Hi Multis

Pfew... Yesterday was a deep red day. After such a day, I appreciate the weekend even more than in other weeks.

And of course, weekend also means a new Overview Of The Week.

Articles In The Past Weeks

We are keeping up the pace. This is again the fourth article this week. Let’s look back at the three previous articles.

In the first article this week, I presented you the second part of the deep dive on the newest Potential Multibaggers pick. It’s already up 30%, but if you want to hold for the long term, reading this can help you decide if you still want the stock.

In the second article of the week, we dissected Celsius Holding’s earnings.

Yesterday, I published the third article of the week, another earnings deep dive. This time, the outstanding Datadog earnings reflected the fundamental change the company has undergone over the last few quarters. We looked at what changed.

Memes Of The Week

It’s funny how people react to this section. Some people love it and others hate it. Now, if you hate it, you can scroll past this section, but if you love it, you would have to miss the memes otherwise, so I’ll keep them in.

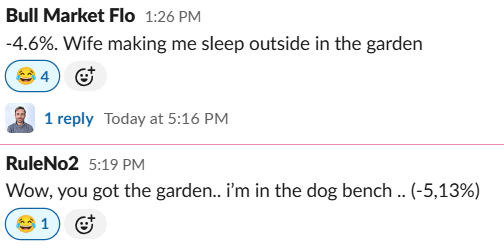

This is not really a meme but from the Potential Multibaggers community. The Friday bloodbath left some traces, haha.

Bryan Johnson, the millionaire health freak who became even more famous because of the Netflix documentary Don’t Die: The Man Who Wants To Live Forever, also posted a stock market meme about Friday’s market action.

I also laughed hard with this one because it’s so true for so many investors.

This one went viral on X because of the funny cross-reference between the comics and movies and the chip company.

The high token costs also created a few memes, like this one.

Earlier this week, the market was much better than Friday and this inspired Multi bep for this funny thought.

Interesting Podcasts Or Books

This week, I listened to an episode of David Gardner’s podcast Rule Breaker Investing. David Gardner is one of the best investors of the last decades. He has picked multiple 100+ baggers like Amazon, Tesla, Nvidia, and several others. And yes, he kept them.

He recently turned 60, and in that context, he made an episode titled “60 Thoughts As I Turn 60.“ He puts them in three categories: investing, business and investing. Recommended!

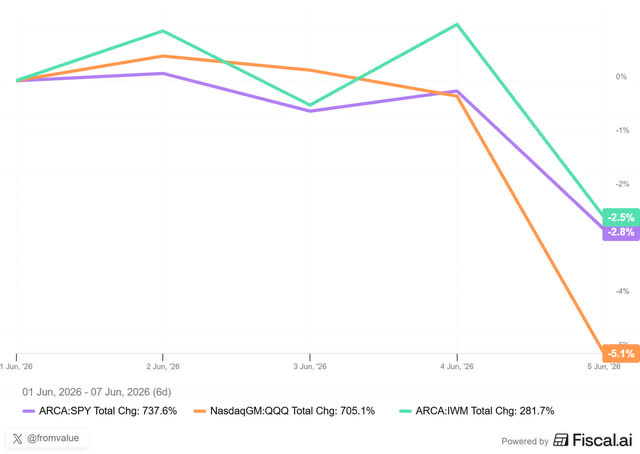

The markets in the past week

The markets were down substantially, by 2.5% for the Russell 2000, 2.8% for the Nasdaq a whopping 5.1%.

Last week, I wrote:

In exactly two months (March 31 to now), the Nasdaq is up a whopping 29.71%. That’s crazy. And unsustainable.

I hate the word correction, because it implies that the market has done something wrong. But right now, I think a correction would be welcome.

Now, sometimes, you have to be careful what you wish for. But what feels bad for the short term can be very healthy for the long term.

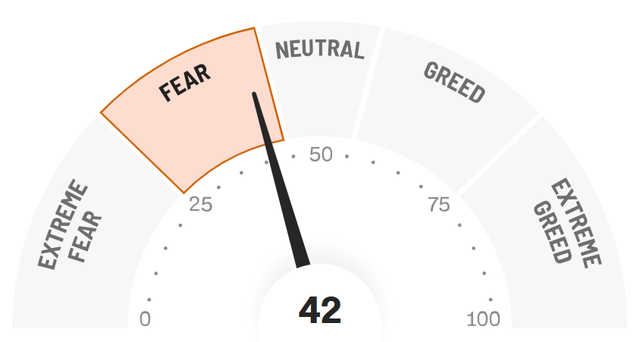

The Greed & Fear Index dropped from Greed to Fear.

Quick Facts

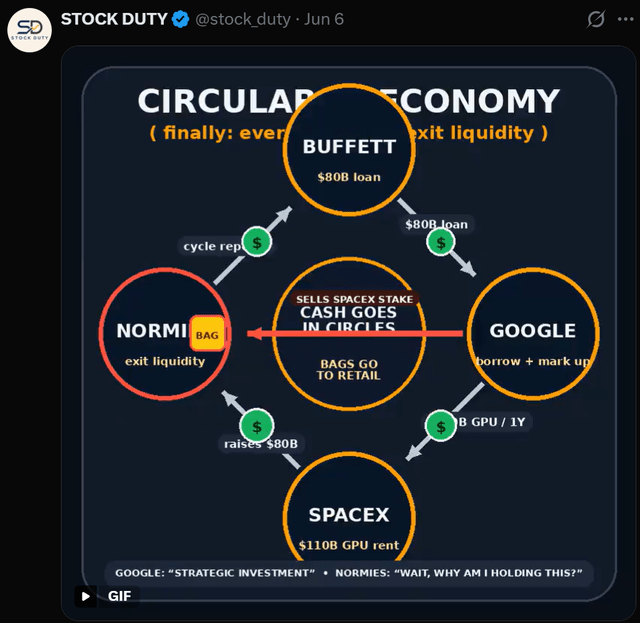

1. Don’t Buy SpaceX’s IPO

What a coincidence (not). Just a week before SpaceX’s IPO (scheduled on Friday), the company announced that Google will rent computing power from SpaceX for $920 million per month for 32 months. That means an additional $ 29.44 B in revenue.

But mind the details. It’s $920 million per month. Not a $29.44B contract. The difference is in this sentence:

After December 31, 2026, the agreement may be terminated by either party upon 90 days’ notice.

Google owns 6% of SpaceX. At the expected IPO value of $1.75T (yes, a T), that means that it has an investment of $105B in SpaceX at that valuation. So, it’s not that it doesn’t want to help SpaceX.

It even inspired someone to make this GIF. It’s a bit cynical, but you can’t say it’s total nonsense.

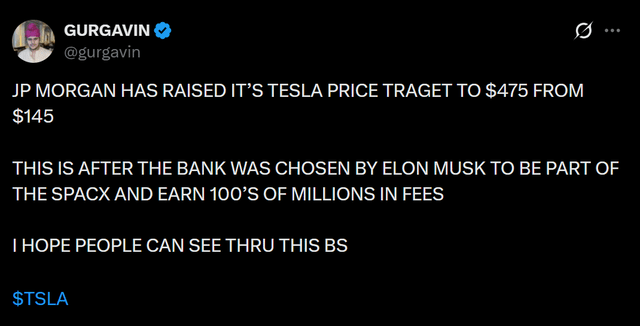

And some other suspicious things are going on. This for example.

If you still believe price targets, please let this convince you to stop attaching any credibility to them.

But back to SpaceX and why you shouldn’t buy the IPO. It’s quite simple. You are the exit liquidity. That’s a fancy name for being the sucker to pay insiders, VCs and early investors at peak hype valuations.

Before the Google deal, SpaceX traded at 94 times the 2025 revenue. That’s not a typo. 94x forward revenue, not profit. That’s bonkers.

Suppose that SpaceX grows its revenue by 50% without the Google deal. That’s very strong growth. That would mean $28B in revenue. Add one year of Google revenue and you have $39B. Very strong, but that still means SpaceX’s valuation is 45 times revenue.

If someone wants to buy Potential Multibaggers for 45 times the forward revenue, please contact me.

Still not convinced not to buy the SpaceX IPO? Look at this.

Ok, if you want to buy, I know what you are going to say: SpaceX is an exceptional company. Well, here are some other exceptional companies like Cloudflare, CrowdStrike, Facebook, Shopify, Palantir, and multiple others.

Focus on the last column. The stocks of these outstanding companies that went public that year dropped by 55% on average within a year.

I may buy SpaceX at some point, but not at the IPO.

2. Bullish For Nvidia

I don’t know if people think about what happened in the context of Nvidia. This is pretty important.

SpaceX doubles the price of operation to rent out its GPUs to Google. This means two things:

1. There are still not enough GPUs to quench the chip thirst. Nvidia ramps up its production continuously, but it can’t follow the demand. Google decided, therefore, to rent the GPUs from SpaceX.

2. This also shows that Nvidia’s GPUs are probably better to run Gemini on than Google’s own TPUs. Why would Google pay double the market price for GPUs if its own TPUs are cheaper than that market price to start from. It would simply make no sense.

Jensen Huang has said on several occasions that Nvidia’s Blackwell costs twice as much as an ASIC chip, of which Google’s TPU and Amazon’s Trainium are examples. So that means Google pays four times as much for GPUs as it would if it simply deployed its own TPUs.

There is something interesting that Jensen Huang adds to the price. He says that even if Blackwell is twice as expensive, the compute power, efficiency, energy efficiency, etc., means that Nvidia’s GPUs are twice to eight times as effective. Google seems to admit that with this rent.

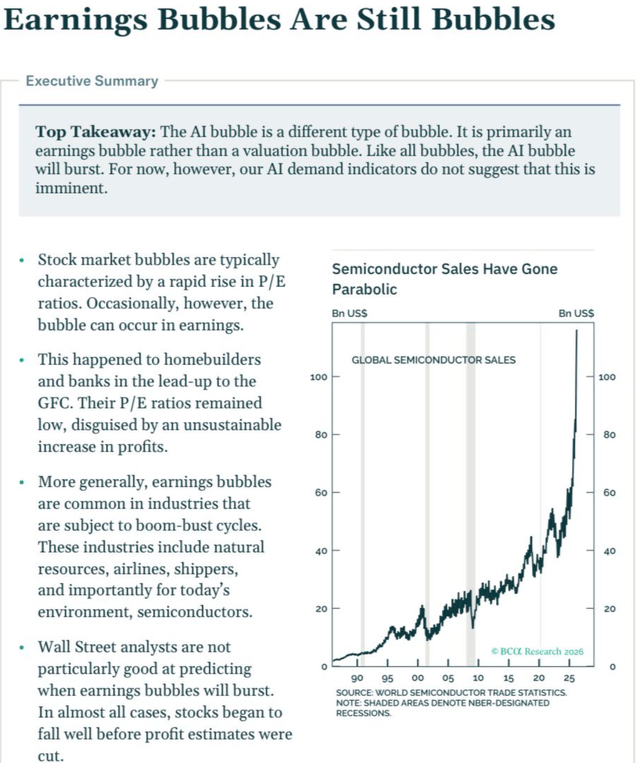

3. An Earnings Bubble?

This week, I read this interesting post.

The argument is simple and correct. While many compare this to the dotcom bubble, probably because AI a revolutionary tech innovation, this looks more like the build-up for the Great Financial Crisis.

These charts are shared to convince people that this is different than the dotcom bubble.

Do you know why that’s convincing? Because it is different than the dotcom bubble.

In the buildup to the Great Financial Crisis, banks and home builders also posted big earnings gains. But they poked them up with very risky behavior.

Now, don’t get me wrong. What happened then was much riskier than what happens now. Now, the financial system will probably not in danger.

What I mostly mean is that people want to predict the next bubble by making it fit into the mold of a previous one.

Right now, I have the same opinion as the takeaway of what I showed you earlier. Yes, this is a bubble. Yes, it will pop. But probably not now yet.

4. When Good News Is Bad News

Over the short term, the market doesn’t trade on the economy but on interest rates.

We saw a big drop in the indexes this week. Most of that was from Friday. The Nasdas lost dropped 4.18% in a single day. The reason? The job report came in, and it blew all expectations out of the water. The US economy added 172,000 jobs in May, double the expected figure.

The market had been counting on rate cuts, but with higher interest rates and this strong jobs report, the odds of a rate hike are higher than of a cut.

But there’s a caveat. The job report looks like a blow-out economy, but if you look closer, there’s something else going on.

Just to be clear, the trend is cooling. Higher-wage cyclical jobs are still shrinking, and those are usually a better indicator of the trend, not people temporarily hired for the World Cup.

The takeaway for Multis? Nothing about the fundamentals changed this week. The price is a fickle market trying to price a company’s next decade and more. That’s an impossible exercise and that’s why emotion over the short term matters a lot. In the long term, a company’s return is determined by fundamentals, though.

When you join Potential Multibaggers now, you get my entire investment system:

✅ Best Buys Now: every month, the 5 best stocks to buy

✅ My Proprietary Quality Score: rating companies on 17 quality metrics nobody else uses

✅ Deep Earnings Analysis: thorough breakdowns that reveal what really matters

✅ Valuations & Buy/Hold/Sell scales: cut through the noise and know exactly when to act

✅ 15,000+ Word Deep Dives: each pick gets 4-5 extensive articles so you understand exactly what you own.

✅ Private Community: direct access to me and 800+ serious long-term investors.