Celsius: Something Unexpected Just Happened For The First Time

Celsius is buying its own stock. Should you?

Hi Multis

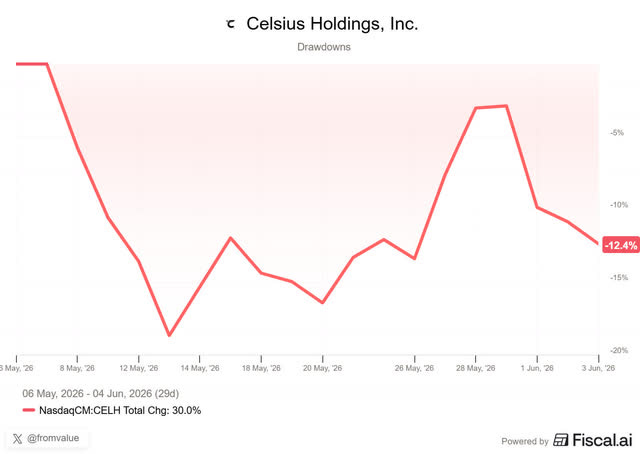

Celsius Holdings (CELH) reported its Q1 2026 results on May 7, and the stock kept dropping. It’s now 12.4% lower than before the earnings.

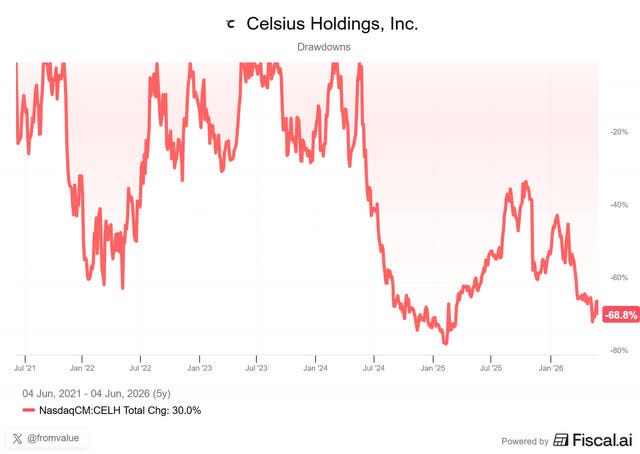

Year-to-date, the stock is down 34% and from its 2024 all-time high, it’s down almost 70%.

The real question is, of course, whether the market is wrong and gives us an opportunity to buy, or if the weak stock price is a sign that there’s more.

Let’s look at the numbers first.

The Numbers

Revenue: $782.6M, up 138% YoY, beating the consensus by $22M or 2.9%.

Adjusted EPS: $0.41, up 128% YoY, beating the consensus by $0.12 or a whopping 41.4%.

GAAP EPS: $0.33, up 120% YoY.

North America revenue: $747.3M, up 144% YoY.

International revenue: $35.3M, up 55% YoY.

Brand split: Celsius $348M (+6% YoY), Alani Nu $368M (+60% pro forma YoY), Rockstar $67M.

Gross margin: 48.3%, down from 52.3% last year in Q1, but better than the 47.4% in Q4 2025.

GAAP net income: $110.1M, up 148% YoY.

Adjusted EBITDA: $195.5M, up 181% YoY. EBITDA margin of 25.0%, up from 21.2% last year.

Buybacks: 700K shares for $24.1M at an average price of $35.39. $236.1M still left of the $300M buyback program.

So on the surface, the results look really strong. Celsius posted substantial beats of the consensus, with better margins. And yet, the market didn’t seem to care. Let’s look into more detail.

The Celsius Brand Problem

I start here because I think the 6% growth for the Celsius brand is why the market doubts the company’s growth story. For the first time, Alani Nu was bigger than Celsius. Revenue for Alani was $368M, compared with $348M for Celsius.

A part of that is seasonality. Celsius is the fitness brand of the portfolio, and apparently, people drink fitness drinks more in spring and summer than in January and February. Alani Nu is more seen as an everyday brand. For full-year 2025, Celsius did $1.46 billion and Alani Nu (acquired in April 2025) did roughly $1 billion. So, on an annual basis, Celsius was still bigger last year. But Alani Nu posted 60% revenue growth versus 6% for the Celsius brand. Is it in trouble? Monster grew more than 20%. That 6% growth for the flagship brand looks very weak.

At the Deutsche Bank conference on June 2, John Fieldly explained what’s going on. Before PepsiCo, Celsius was distributed by more than 300 independents. This is important to know.

To get shelf space at certain retailers, Celsius often did custom flavors. Fieldly gave an example. A convenience chain of 300 stores didn’t believe Celsius would sell, so the company created a Cherry Cola exclusively for them. It worked, and therefore, they could also sell Celsius on the shelves. That flavor only existed for those 300 stores. And there were many flavors like that.

In the PepsiCo system, that approach doesn’t work. If you have national distribution, you need national consistency. So Celsius is removing all regional flavors and focusing on the national flavors. Fieldly:

We want to have a consistent portfolio around the country. As we say internally, we want to keep the fast cars on the track.

Each flavor removal immediately results in lost revenue. That’s a big part of why the Celsius brand grew only 6% this quarter.

The core Celsius 12-oz cans grew 11% in convenience stores. So, that proves Fieldly’s story. The assortment is shrinking, but what remains of the legacy brand is doing well.

Fieldly also said something at the conference you don’t often hear from a CEO:

Especially on Celsius, we should have had more innovation. That would have added more complexity with the integration of Alani and Rockstar, but we should have had more innovation, and we’re cycling over 6 innovations versus last year.”

So Celsius underinvested in flavor innovation on the flagship brand. The reason was the integration of Alani Nu and Rockstar. Understandable. Last year, there were 6 innovations, so that makes the comps tougher. Management will continue to focus on the integration now but go full-in on innovation in 2027.

Alani Nu: Firing On All Cylinders

If the Celsius brand looks weak but is better than it looks at first sight, Alani Nu is firing on all cylinders. I think we can already say now that this was a killer acquisition for Celsius. That it would overtake Celsius in sales so fast was really unexpected.

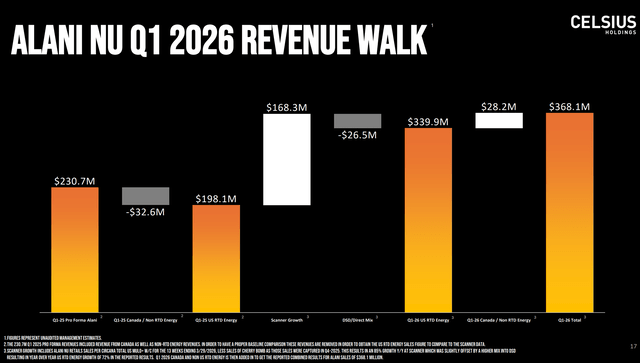

Revenue was $368M, up about 60% pro forma. Pro forma means this is against Alani Nu’s sales last year, before Celsius bought it. Scanner data, which measures what consumers bought, even showed the brand up 100% YoY.

So consumer demand grew faster than the reported revenue number suggests. That’s important, and it’s worth explaining why the two numbers are quite a bit apart.

The company gave us a breakdown:

Alani Nu sold $230.7M in Q1 2025, the quarter before Celsius bought the company. But not all of that was from the US energy drink market. Take out $32.6M from Canada and from non-energy products like protein bars, and you get $198.1M of U.S. energy drink sales. That’s the right number to compare this quarter with.

From there, scanner data shows U.S. energy drink sales grew 85% YoY, not the 100% I mentioned earlier. The difference is Cherry Bomb, a limited-time flavor that Celsius shipped to stores in Q4 2025. Consumers bought most of those cans in Q1 2026, but the company already booked revenue when the cans shipped, so the revenue was in the Q4 results. Without that distortion, growth would have been 85%.

Apply 85% growth to that $198.1M, and you get about $168M of additional revenue. That’s the white bar.

Then there’s a $ 26.5 M deduction. When Alani Nu was sold directly to retailers like Walmart, Celsius booked the full wholesale price. Now that Alani Nu is being sold through PepsiCo’s DSD (Direct Store Delivery) system (which means Pepsi trucks deliver cans straight to store shelves instead of to a retailer’s warehouse), Celsius sells the cans to Pepsi first, and Pepsi takes a cut before reselling them to retailers. So even if the same number of cans are sold to consumers, the revenue Celsius reports per can is lower.

So the takeaway is: consumer demand for Alani Nu grew by 85%. That’s phenomenal growth. Of course, even if Pepsi takes a part of that, volume is much bigger and on top of that, Celsius also had to pay its previous distributors, but in another way.

At the Deutsche Bank conference, Celsius shared that Alani Nu’s availability in convenience stores went from 65% in January to 91% in May. That’s a sea change.

Normally, when a brand expands distribution that fast, sales per store go down. The new stores are usually lower quality and it takes time for shoppers to find the product. With Alani Nu, sales per store actually went up over those five months.

The bear case on Alani Nu is that it’s a flavor brand, riding LTOs (Limited Time Offers), like Cherry Bomb and Lime Slush, that are fashionable for a few months and then disappear.

The fear is that once the LTO cycle slows, the brand fades. But the data shows the opposite. The brand is reaching more stores and the consumer is buying more per store, not less. That’s a really strong indicator that the brand has staying power.

There’s a related concern: that Alani Nu is just stealing sales from Celsius. Fieldly was asked this directly at the conference. His answer was that there’s some overlap, but Alani Nu is also reaching consumers that Celsius wasn’t. I think he’s right, and the proof is in the share number. If Alani Nu were just stealing Celsius’s sales, then the core Celsius brand wouldn’t have grown by double digits on a normalized basis (see above for that).

The market got the two big numbers wrong. The question is whether it’s also wrong about the rest, the margins, the Costco threat, and the current stock price. Below are my answers.

When you join Potential Multibaggers now, you get my entire investment system:

✅ Best Buys Now: every month, the 5 best stocks to buy

✅ My Proprietary Quality Score: rating companies on 17 quality metrics nobody else uses

✅ Deep Earnings Analysis: thorough breakdowns that reveal what really matters

✅ Valuations & Buy/Hold/Sell scales: cut through the noise and know exactly when to act

✅ 15,000+ Word Deep Dives: each pick gets 4-5 extensive articles so you understand exactly what you own.

✅ Private Community: direct access to me and 800+ serious long-term investors.