Hi Multis

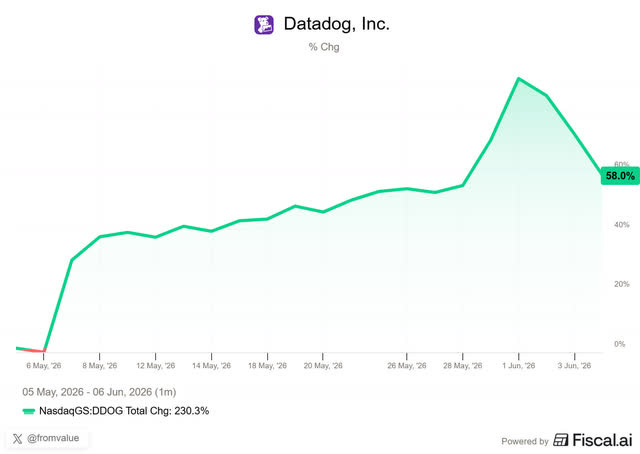

Datadog (DDOG) reported its Q1 2026 results on my mother’s birthday (May 7), and I had not reviewed the earnings yet. Now that I have, I can say it was potentially the best quarter this company has ever delivered. And the market agreed. The stock is still up 58%, even after the drop in the last few days. It was up 90% just a few days ago. Crazy.

If you want the best stock screener, the best charts, the best analyst estimates, the best earnings calls, Morningstart research, and sooooo much more, join Fiscal and get 15% off.

I keep repeating this, but it’s good to see this live for long-time Multis. Stocks can do nothing for years and then suddenly shoot up like a rocket over a small period of time. As long as the company keeps performing and the fundamentals stay intact, this often happens. But it can take years of patience. Years of nothing and then suddenly everything. That’s the stock market for you.

Datadog’s outstanding quarter also crushed one of the most superficial bear cases I heard about Datadog: that AI is going to eat it. At the end of the article, you’ll understand why this is ridiculous.

The Numbers

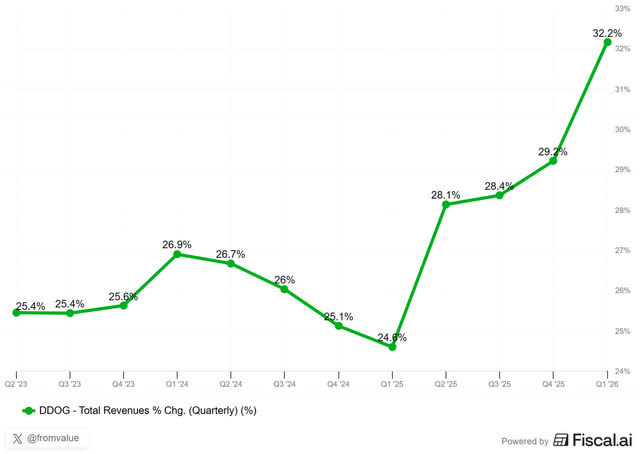

Datadog’s Q1 revenue came in at $1.006 billion, up 32% year-over-year. The consensus was $960 million, so this was a $46 million beat, or 4.8%. It was the first time Datadog crossed a billion dollars in a single quarter. A nice milestone.

This was the fourth consecutive quarter of accelerating revenue growth, and not by a bit. Just look at this beautiful climbing line.

It’s impressive that Datadog can do this at this scale.

CFO David Obstler said on the call that ARR (annual recurring revenue) growth accelerated in each month of Q1, and management said the trend continued in April. I think that’s one of the reasons why the market reacted the way it did to these earnings.

Non-GAAP EPS was $0.60, beating the consensus of $0.51 by $0.09. Non-GAAP operating income was $223 million, good for a 22% operating margin. Free cash flow was $289 million with a 29% margin.

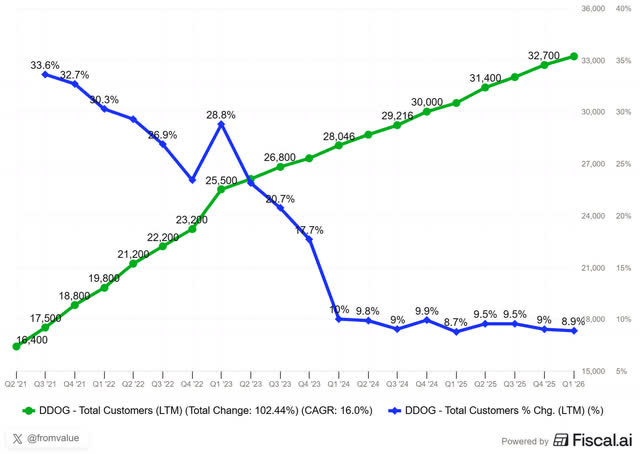

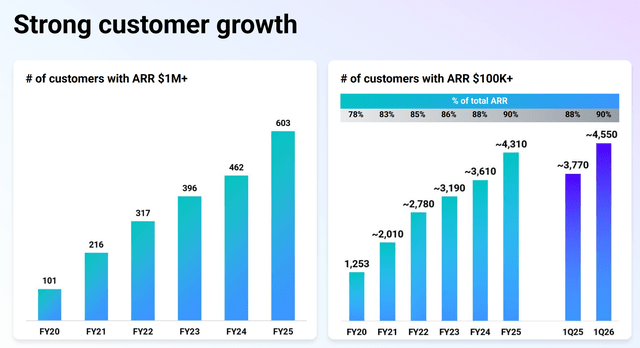

Datadog ended Q1 with about 33,200 total customers, up from about 30,500 a year ago.

When you plot this on a chart, which Fiscal can do, of course (get 15% off here), you see something interesting.

Customer growth is not responsible for the revenue acceleration we saw. So, what is? This.

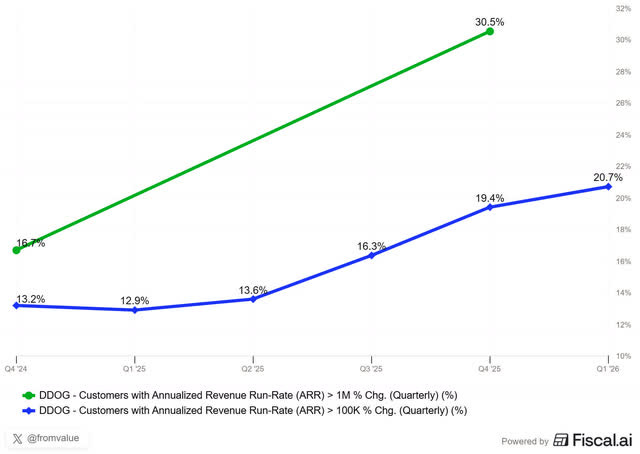

If you wonder why the green lin, with customers with ARR of more than $1M stops a quarter earlier, it’s because Datadog only provides once a year. But you see the trend. It’s big customers that power the growth. There were about 4,550 customers with an ARR of $100,000 or more, up 20.7% from 3,770 a year ago. For the biggest customers, it’s probably even more. Don’t forget that Datadog has usage-based billing and with more AI, that means more usage, as I have always said, long before the market agreed.

Net retention has not moved in a long time. It’s always 120% or a bit higher.

The Core Business Keeps Accelerating

For most of 2025 and until a month ago in 2026, software stocks were beaten to a pulp on the fear that AI was going to disrupt or replace SaaS. The narrative was that LLMs and coding agents would make a lot of cloud software obsolete. Anything that wasn’t directly an AI play looked vulnerable.

And then Datadog reported. It was the turnaround for software, it seems. CEO Olivier Pomel on the call:

Non-AI customer revenue growth accelerated again this quarter to mid-20s percent year-over-year, up from 23% last quarter and 19% in the year ago quarter.

So, the non-AI part of Datadog’s business, the part that the market wrote off, just posted its third consecutive quarter of accelerating growth. From 19% to 23% to mid-20s. Or put differently, traditional SaaS customers accelerated their Datadog spend. SaaS dead? Hahaha.

This is the Anti-Non-AI Bubble I have talked about for months now. The SaaS market is much bigger than everyone seems to factor in now. Founder and CEO Olivier Pomel confirmed how much growth Datadog can still have just by taking market share alone already. From the J.P. Morgan conference two weeks after the earnings:

We’re the leader in observability, we’re #1 there, but we still have only 13.6% of the market according to Gartner. So this tells you how early it is in the market for us, how much opportunity there is ahead of us, even factoring out all of the new developments with AI.

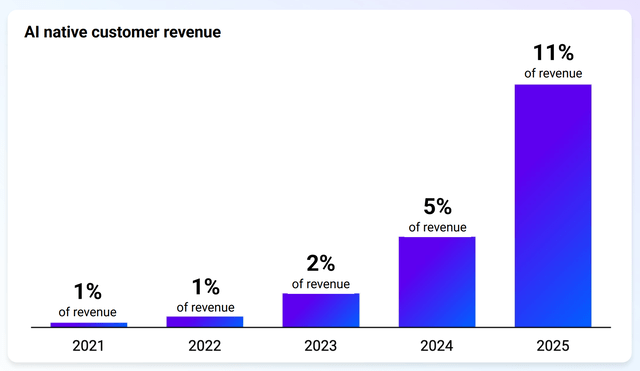

The AI-native cohort, of course, is also growing rapidly. Datadog now has 22 customers spending more than $1 million annually on AI-related work, and 5 spending more than $10 million. And Pomel disclosed at the recent Investor Day in February that AI-native customers represent about 11% of Datadog’s total revenue today, up from 5% in 2024, and just 2% in 2023.

But many seem to forget that the other 89% is everything else, and that part is accelerating faster than it has in years. Datadog is in a premium position. it gets the AI tailwind on 11% of its revenue (and growing fast), and the SaaS tailwind on 89%. What a great double engine!

The Training Reversal

There was something else that caught my ear on the earnings call that I really liked. CEO Olivier Pomel on the call:

Interestingly, last year, when we reported earnings, we said we’re mostly interested in inference workloads and training is not really a market for us yet. Now we actually see training becoming a market.

That’s an important reversal. So, what changed? Pomel explained the mechanism in more detail at the J.P. Morgan conference:

Models went from being mostly pre-trained to being largely post-trained. The post-training was becoming increasingly specialized to different types of verticals. The stacks that are used for post-training also are becoming richer and richer. And we saw instead of having 5 to 10 companies doing that, now there were 50 to 100.

Twelve months ago, training wasn’t a market for Datadog but now it is. How can this change so fast? Olivier Pomel explained at the J.P. Morgan Conference that the kind of training had changed.

Pre-training is the huge, expensive first step in which a model learns from scratch on incredible amounts of internet data. Only 5 to 10 companies worldwide could afford that. Post-training is what comes after: based on the pre-training, you can teach the model to be good at something specific, like coding, or medical questions, or customer support. It’s cheaper and easier, and now 50 to 100 companies are doing it, but that could soon be 500 or 1,000. This is a very interesting development and another reason Datadog looks well-positioned to profit from AI.

In Q1, Datadog brought in two new deals with the AI research divisions of two of the world’s largest tech companies. One was a 7-figure deal, the other even an 8-figure deal. These are hyperscalers with top-notch engineering talent and a strong culture of building everything in-house, but they still came to Datadog. That says a lot.

Olivier Pomel on the earnings call:

Hyperscalers typically have a culture of building everything themselves, and they certainly have the balance sheet and the human capital to support some of that build-out. Like if there was ever a set of companies for whom it makes sense to do it themselves, that would be those companies. And yet, we see that they have the same issues.

Don’t forget that Anthropic also signed a bit contract. We discussed this last quarter.

Below: the rest of the AI story, why every huge AI company uses Datadog, and what I'm doing with the stock right now.

When you join Potential Multibaggers now, you get my entire investment system:

✅ Best Buys Now: every month, the 5 best stocks to buy

✅ My Proprietary Quality Score: rating companies on 17 quality metrics nobody else uses

✅ Deep Earnings Analysis: thorough breakdowns that reveal what really matters

✅ Valuations & Buy/Hold/Sell scales: cut through the noise and know exactly when to act

✅ 15,000+ Word Deep Dives: each pick gets 4-5 extensive articles so you understand exactly what you own.

✅ Private Community: direct access to me and 800+ serious long-term investors.