My ServiceNow Thesis

Why I started building a position recently

Hi Multis

I’ve had a refreshing holiday in Egypt, and one of the things I wanted to do every now and then is go a bit broader than purely Potential Multibaggers to some stocks that are also in my portfolio. You will not get the same level of detail on these as on the Potential Multibaggers, but it will be what many others call a deep dive, haha. But these articles will be shorter and definitely not regular. Don’t think you will get a quarterly article on ServiceNow from now on.

If you don’t want to miss high-quality articles like this, subscribe now!

Potential Multibaggers will still have absolute priority. I’m also working on part two of the new Potential Multibaggers pick and I hope to have that out later this week, but I need a bit of a broader scope and I think many of you will appreciate this as well. If you don’t, I’m sorry, but this is what I will do from time to time. I’ll also focus more on doing the Potential Multibaggers articles (from the picks, I mean) and the earnings articles will become a bit shorter, unless there’s a good reason to make them long (for example, a deep search if the thesis still holds).

But enough introduction, let’s go to the subject of this article: ServiceNow (NOW).

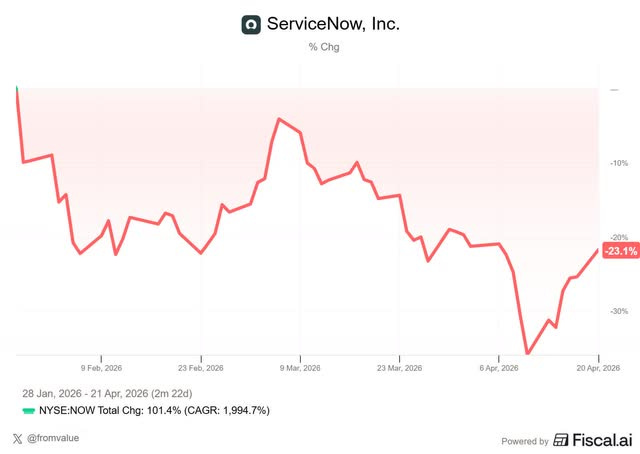

ServiceNow reports tomorrow after close, and the stock is trading at around $100. I’ve followed this one for a long time, and I’ve recently started a position for the first time in quite a while, as you may know.

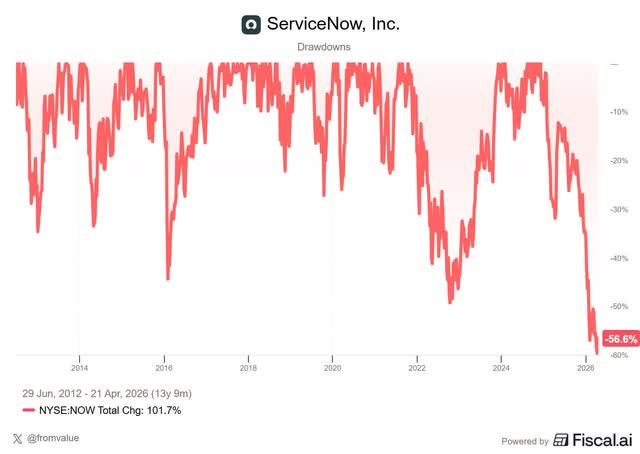

The drawdown context

As is often the case in the market, the drop isn’t really about the results.

Q4 2025 was actually a strong quarter on most fronts. Subscription revenue was up 21% year-over-year to $3.47 billion, and total revenue grew 20.5%, which is strong for a company at this scale. Current RPO was up 25%. CRPO is the money the company already has under contract for the next 12 months but still has to recognize as revenue because it still has to deliver the services. So, if you look ahead, ServiceNow also seems to be in excellent shape.

On top of that, ServiceNow closed 244 AI deals worth more than $1 million in net new ACV (annual contract value), which is substantial already. For 2026, management guided subscription revenue to a range of $15.53 to $15.57 billion, good for 19.5-20% growth. Knowing guidance is usually conservative, that’s strong. The board also authorized an additional $5 billion share repurchase program.

A lot to like there, right?

And yet the stock dropped about 15% the day after the earnings, and while it has recovered a little, it’s still 23% below where it was before earnings.

So, if the reason was not in the results, it must be in something else. As so often in investing (this is consistently underestimated), it was in the story that has been circulating for months now.

It goes something like this: AI will disrupt everything, and since ServiceNow sells software to enterprises, ServiceNow must be a loser. I have called this the “anti-bubble” for months already. As the biggest companies that use AI are private (OpenAI, Anthropic, X), you see that there’s the opposite of what happened in the dotcom bubble. Instead of bubbles in big companies, supposed losers are shorted and sold, purely based on sentiment. Probably a lot of that money is being invested in the next round of Anthropic and/or OpenAI.

Now, I’m not saying the story about AI disrupting SaaS is completely wrong, but it’s extremely exaggerated. That means the child is often being thrown out with the bathwater. I would be very surprised to see ServiceNow end up at the losing side of this shift. And that mismatch, between a strong business and a weak narrative, is exactly why I started building a position.

The Platform Thesis

The first thing to clarify is that ServiceNow isn’t a point solution. It’s a platform, and that distinction matters much more than most people seem to realize.

A point solution solves one specific problem, so if AI can solve that problem better or cheaper, the point solution dies. That’s a real risk in SaaS right now, and for plenty of companies, it’s a genuine threat. For me, it’s an absolute filter for which stocks to buy or not. A platform is the layer everything else runs on, so it doesn’t die when a new technology arrives. The new technology runs on the platform, not the other way around.

ServiceNow knows this and it doubles down on this. It’s positioning itself as a sort of AI control tower, a central dashboard where enterprises can monitor and manage all their different AI agents from one place. So, that’s a product enterprises need because of AI, and I think that will become very valuable over the next few years.

ServiceNow isn’t only helping other companies manage AI, but it’s also monetizing AI itself, through its NowAssist, which was on track to generate over $500 million in annual contract value coming out of Q4.

The partnership strategy has been smart, too. Rather than trying to compete with OpenAI or Anthropic on foundation models, which would be a losing game, ServiceNow has integrated with both. The company is building the workflow layer that sits on top of whichever model wins, which is exactly where I want a platform to be positioned.

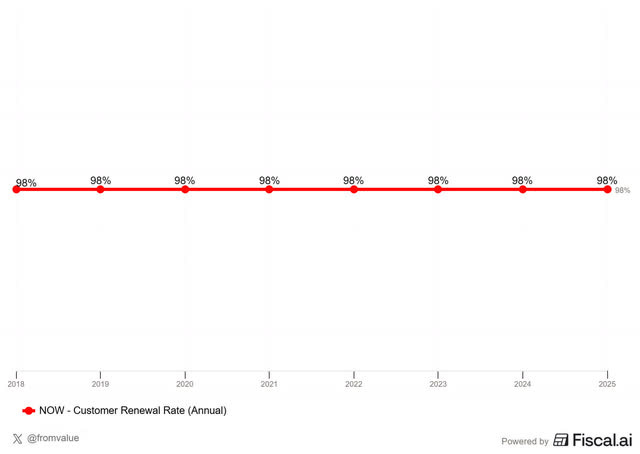

Then there’s the retention number, and this is where I think people underestimate the business the most. This is a chart since 2018. Do you see the AI impact? I don’t.

Retention at ServiceNow is so high because ripping it out of your system once it’s embedded is incredibly difficult. It’s often a multi-year project involving dozens of teams and workflows across the enterprise, and nobody takes that on just to save some money. You only rip out a system like that when something is badly broken, and right now, nothing is broken. Sometimes, you don’t have to overcomplicate things.

Which brings me to the other thing the market is worried about: pricing. The story is that AI agents will replace human seats, so seat-based revenue collapses, and the whole business model cracks under the weight of its own legacy. But a company with ServiceNow’s position isn’t going to just sit there and watch its revenue model die. I don’t get why people think that everything will change with AI, except for the companies adapting to it. We’ve seen that story with Google last year. The sentiment has totally shifted and I think ServiceNow could see the same thing. That’s not a prediction for tomorrow, but for the longer term.

If AI agents take off the way the bulls claim they will, that’s actually great news for ServiceNow, because usage will explode. More AI agents means more workflow transactions, which means more revenue per customer. The companies at risk of disruption are those that can’t switch to a usage-based pricing model because there’s not enough activity on their platform or, even worse, in their solution.

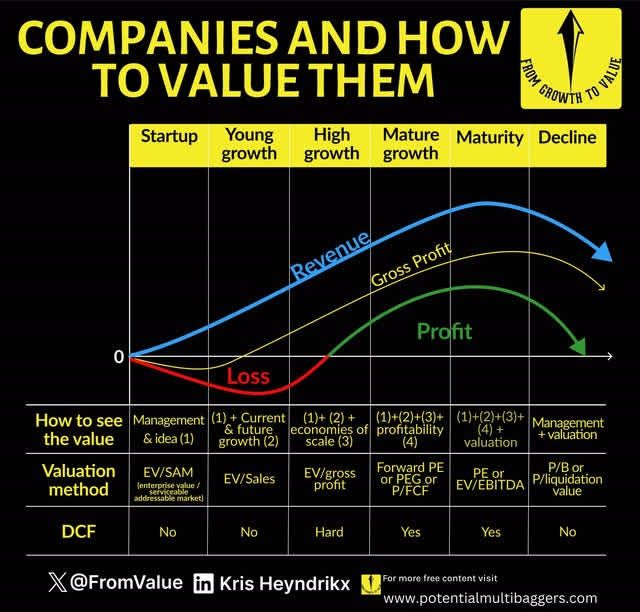

Quality And Valuation

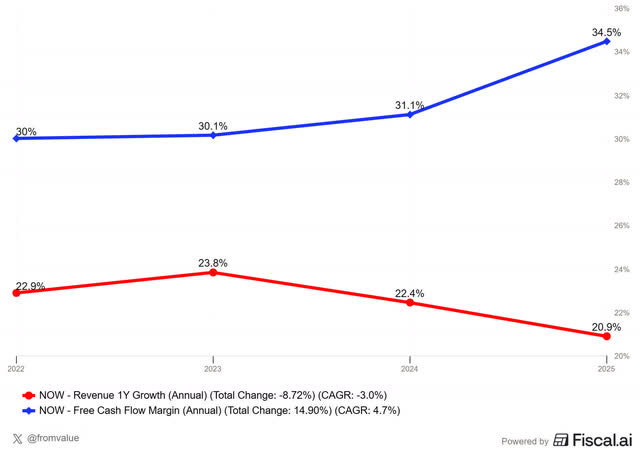

The simplest way to test whether a software company is doing great is the Rule of 40, where you add revenue growth to free cash flow margin, and anything above 40 suggests you’re looking at a high-quality business.

Now, look at this.

34.5% + 20.9% = 55.4%, which is simply outstanding!

The important thing is that it has been there consistently, not just in one good quarter. Yes, revenue growth has slightly declined (but not much) but the FCF margin has increased.

These aren’t the numbers of a company with a pricing problem or a demand problem.

For a quick valuation, I use my own framework, summarized in this graph.

As ServiceNow continues to grow by around 20%, which you might argue is still high growth, let’s first look at an EV/Gross Profit basis.

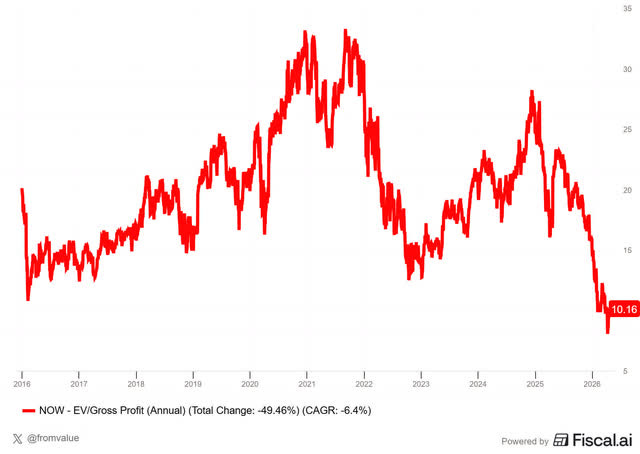

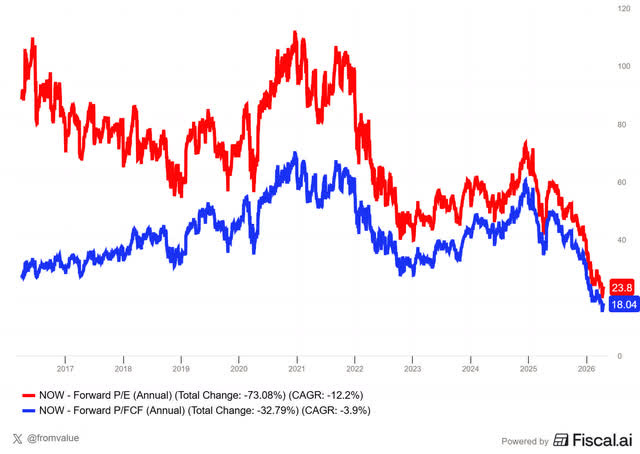

As you can see, on an EV/Gross Profit basis, ServiceNow is the cheapest it has ever been since its IPO almost 14 years ago. But maybe the market thinks this company is no longer in high growth and has switched to mature growth? Fair, let’s check that as well. Again, you see the same pattern: the stock has never been this cheap.

If you don’t want to miss all the great Fiscal AI charts and other tools, get 15% off here.

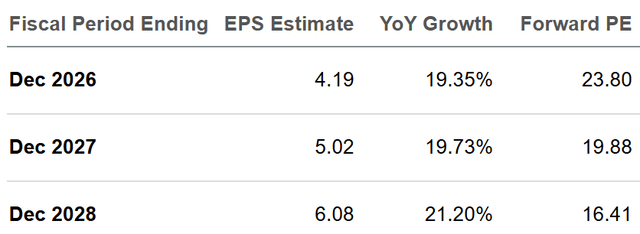

Now, let’s also check the forward PEG (Price/Earnings/Growth).

If we divide the expected PE by the expected growth, the 2026 PEG is 1.23, which is on the cheap side of fair. The 2027 PEG is almost exactly 1, the exact border between cheap and fair. The 2028 PEG is just 0.77, plainly cheap.

So what you’re paying for is a company compounding revenue at roughly 20%, with 98% retention, and an AI monetization story already in place, at a multiple that sits far below its historical averages and bordering on cheap. That’s why I find it interesting right now.

Three things I’m watching tomorrow

With the earnings tomorrow, I’ll watch a few things in particular.

If you don’t want to miss high-quality articles like this, subscribe now!

The first is net new ACV from AI deals. The Q4 number was 244 deals worth more than $1 million, and I want to see what Q1 looks like, particularly for the AI-specific cohort.

The second is cRPO growth, which, for me, is probably the most important forward-looking number in the entire report. It tells you what revenue is already under contract for the next 12 months, it’s much less noisy than headline revenue, and it gives you real visibility into the pipeline. Q4 grew 25%, which is very strong, and if Q1 holds anywhere near that level, the top-line guide for 2026 will probably be revised a few times upwards in the coming quarters.

The third thing I’ll be listening for is any commentary from management on the evolution of the pricing model. They’ve hinted at a move toward usage-based pricing, and I want to hear if there’s any news on that front.

I try to be honest about what would change my mind, because a thesis without a break point is just a story you tell yourself.

If cRPO growth decelerates meaningfully below 20%, that would worry me, and if NowAssist ACV goes flat or down quarter-over-quarter, that’s a real red flag. If the renewal rate were to suddenly drop by a few percentage points, that would be worrying.

No single one of these kills the case in isolation, but all of them together would, and I’d rather be clear about that up front than pretend otherwise.

The bottom line

The market is lumping all SaaS companies into one pile right now, and I think that’s both a mistake and an opportunity for long-term investors.

Some SaaS businesses genuinely will lose to AI. Point solutions doing narrow tasks, tools that wrap thin features around a user interface, anything where the core job can be done better or cheaper by a model... Don’t get me wrong, there will be SaaS companies in trouble and I stay away from many now.

But I believe ServiceNow won’t be one of them. It’s the workflow platform that enterprises have used for over a decade, with a real AI product already generating revenue, a credible platform thesis for the agent era, and a pricing model that it can adapt as usage patterns shift.

That’s why I recently started a position. Tomorrow’s earnings will provide valuable data to see if my thesis is on track.

In the meantime, keep growing!

Great article, thanks Kris!

Any update feedback after the earnings will be very welcomed 😊