Hi Multis

Did you check your calendar when you saw the Overview Of The Week come in?

It’s Saturday, not Sunday, but you already got the Overview Of The Week today.

The reason could already be deduced from the title. I’m going to Egypt with my family for a week. As a child of the 80s, I have to think of the great Bangles hit “Walk Like An Egyptian” every time I hear the country’s name. I know it’s maybe a bit immature and culturally not fair for a country with such a rich history, but it’s true.

As a sidenote, the songwriter, Liam Sternberg, was a bit tipsy when he crossed the English Channel. The sea was choppy, and passengers and waitresses had to do moves to keep their balance. It reminded him of the postures of figures in Ancient Egyptian tomb paintings. But back to today.

The consequence of this very-last-minute holiday is that you get the Overview Of The Week on Saturday already, that you will hear me less often in the upcoming week and that there will be no Overview Of The Week next Sunday (no, not next Saturday either).

I have worked on part two of the new pick. I already have about 6,000 words, but I could cut or add words depending on my editing process. So, that’s one you might get in the upcoming week. Or, if not in the upcoming week, definitely in the week that follows. It depends on how much time I will dedicate to working there (don’t pity me, I still love what I do!) and how many hours the article still needs, which I never know exactly and chronically underestimate.

Articles In The Past Weeks

This is just the second article this week. The first one was, of course, on the new pick. You can read the full 7,600 words here.

Memes Of The Week

Three memes this week. This is the first one.

And the second one.

I always love it when people can break out of the current paradigm to mock it, like this one, for example.

Interesting Podcasts Or Books

One of the biggest influences on my investing was David Gardner. As long as he still talked about stocks himself, until 2021, I never missed an episode of his podcast. Now, I listen every now and then and this week, I did that. In this episode, David Gardner talks about little tricks that can help you in life.

The markets in the past week

For a while now, the market and tech stocks have been disconnected (more on that later), so if you are overweight tech (like I am), it’s now harder to assess the broader market by looking at your portfolio alone.

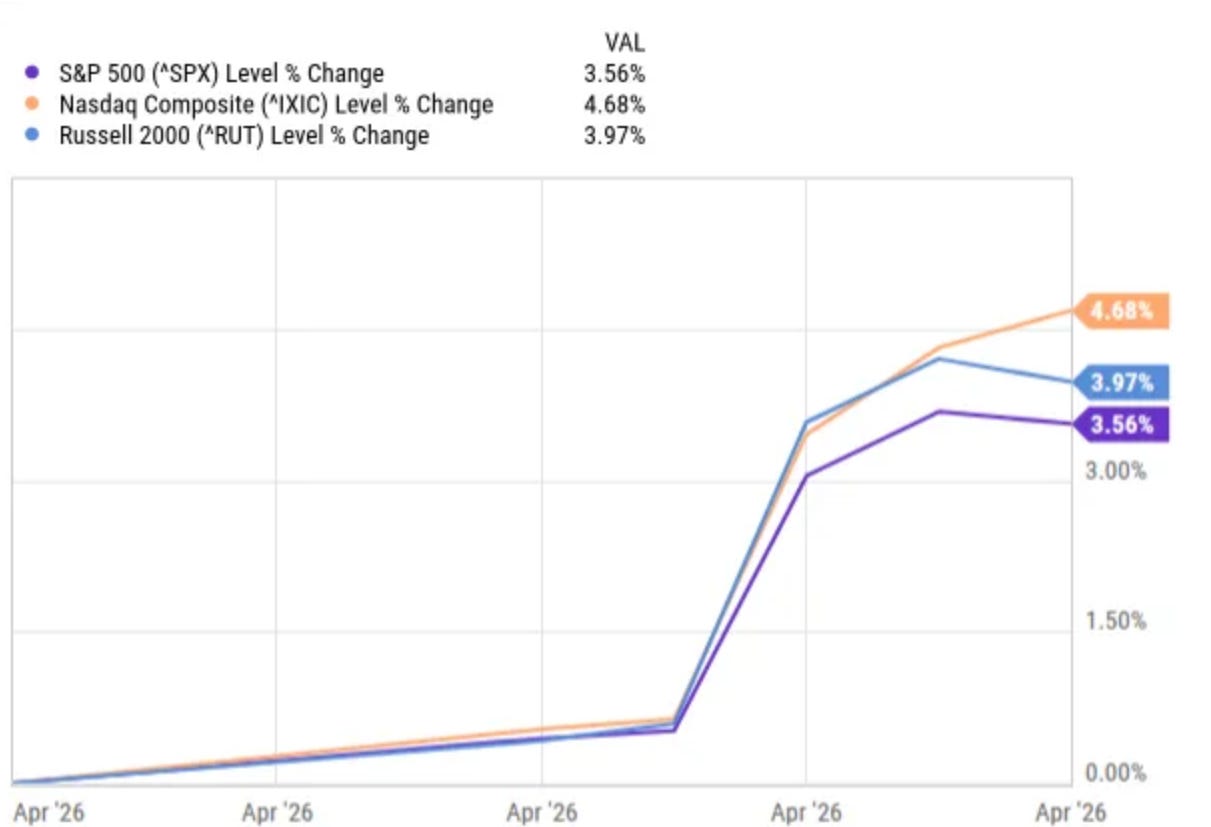

Let’s look at what the indexes have done this week.

As you can see, the markets were up substantially again, just like last week. The Nasdaq won 4.68%, the Russell 2000 3.97% the S&P 500 3.56%.

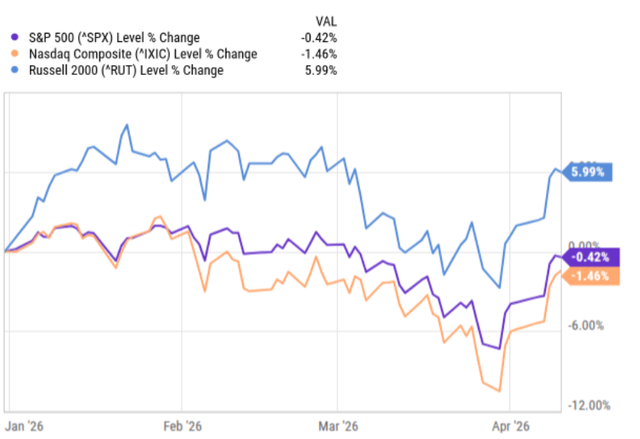

So, where does that leave us year-to-date?

So, after this week:

The S&P 500 is down just 0.42% YTD,

The Nasdaq is -1.46% YTD

The Russell 2000 is up 5.99% YTD.

Remarkable. Because it doesn’t feel like that. But those are the numbers.

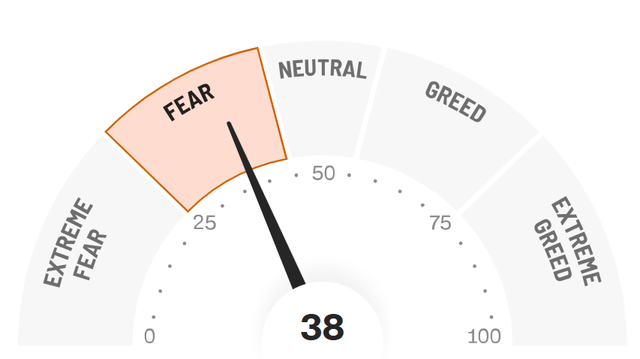

At the beginning of last week, the Greed & Fear Index dropped to 9 but it ended the week at 19. This week, it continued to zoom up, to 38.

That’s still in Fear territory, but the sentiment seems to be improving fast.

Quick Facts

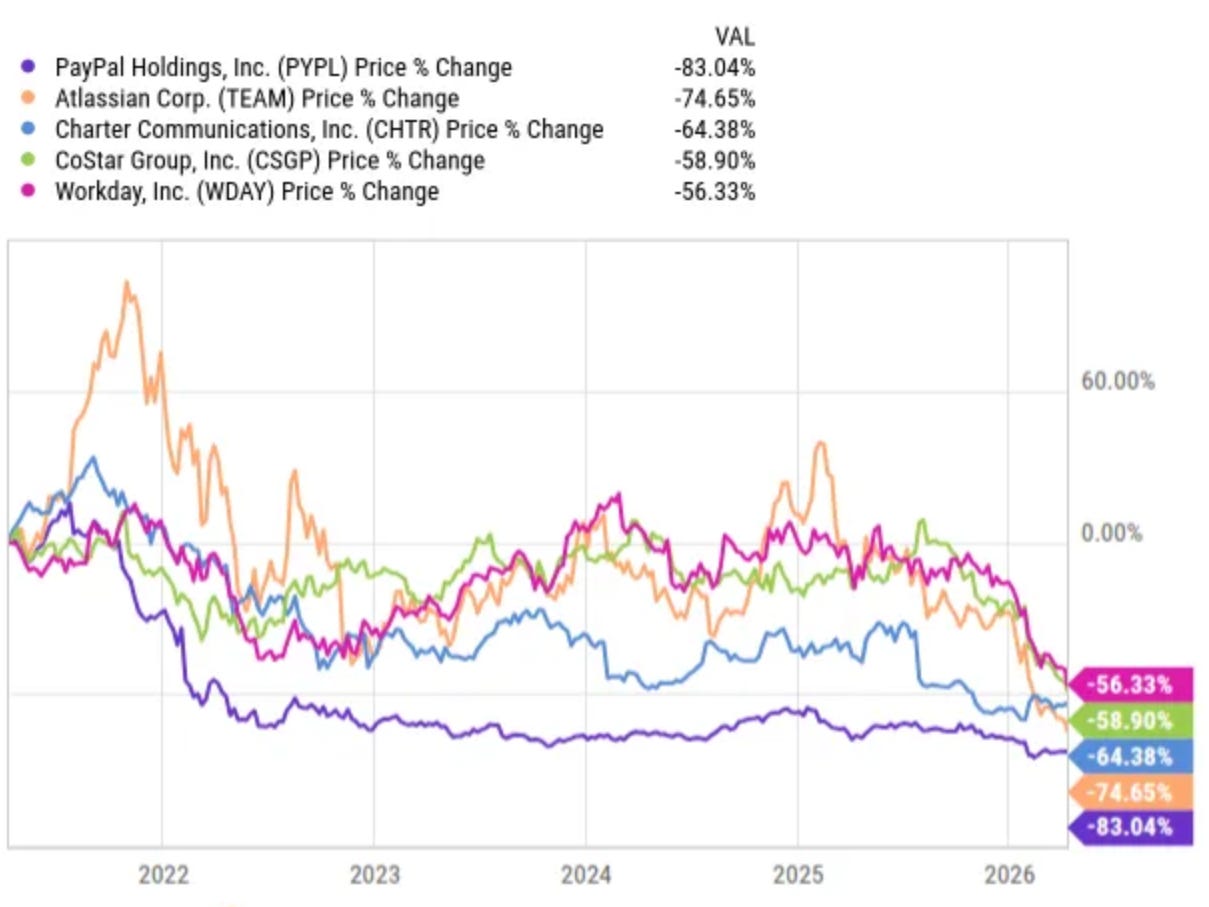

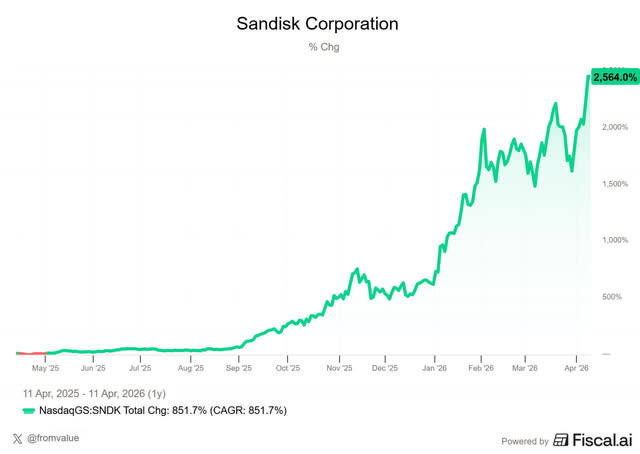

1. Nasdaq 100 Replaces Atlassian by Sandisk

This week, the Nasdaq 100 has booted Atlassian (TEAM) from the Nasdaq 100. It is replaced by Sandisk (SNDK). There was not a single reason why Atlassian was replaced, but the fact that the stock is down the second-most over the last five years won’t have helped. Only “PainPal” did worse over the last five years.

But being removed from the index is not always as negative as it sounds. Sometimes those stocks have already had a big drop and the removal sometimes marks the bottom. On the contrary, the stocks that come in have often had a big recent jump, and that goes for Sandisk too. It’s up more than 25x over the last year.

But, as said, that doesn’t always mean it’s a good thing to “sell your losers” and “keep your winners.” In general, if the investment thesis holds, it’s often a good thing to hold the stocks that are out of favor.

Charlie Bilello gave an example of this with an index replacement. In August 2020, Exxon Mobil was removed from the Dow Jones Industrial Average, and Salesforce replaced it. Exxon returned almost 4x since then, while Salesforce is down almost 40%.

2. Private Equity In Trouble? Or Opportunity?

For about a year or so, I have said every now and then that I saw a bubble in private equity. I couldn’t put my finger on it exactly, but I saw initiatives by people with questionable integrity that wanted to ‘democratize’ private equity. If that’s the case, you know something is fishy.

Private credit was the first problem for private equity. This story is still evolving, but it’s clear some private equity funds will get hurt. The second and simultaneous problem for private equity is the massive exposure to software. Only in the last few months of this year have software deals come down a bit, but they still account for 49% of all deals.

Private market managers poured hundreds of billions of dollars into software firms over this period, betting that software-as-a-service (SaaS) business models would produce strong growth and consistent cash generation. The private equity industry has never been this exposed to a single sector. But now valuations crash and don’t forget that private credit was also mostly given, probably much more than 49%, to software companies.

I’m very sure that some of the software names out there are babies being thrown out with the bathwater, but there will be AI disruption of software companies that only have a nice interface, but no proprietary data, insights, high switching costs or network effects. That means that this is a double whammy for private equity.

Now, the market has sold off many private equity companies and there too, some opportunities could spring up soon. I’m thinking of companies like Brookfield (not that far off its high) and KKR, both part of a cream-of-the-crop group in private equity.

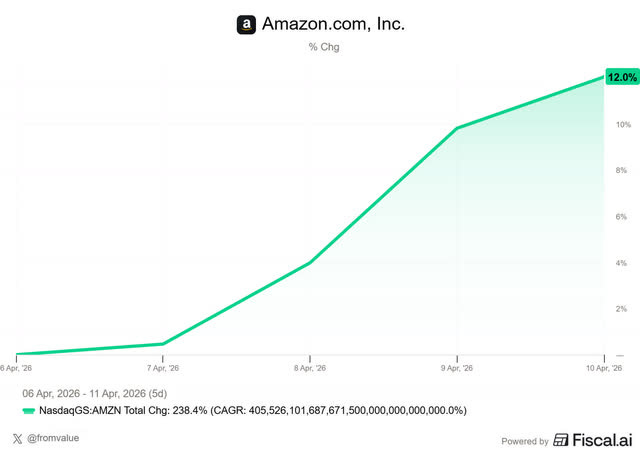

3. Amazon’s Hidden Chip Giant

Amazon’s stock was up about 12% this week after its CEO Andy Jassy published his annual shareholder letter and gave a few interviews.

If you don’t want to miss all the great Fiscal AI tools, get 15% off here.

Jassy shared that Amazon’s AWS AI revenue was already at a $15 billion annual run rate in Q1 2026. Evercore’s Mark Mahaney, a legend in tech investing, had forecasted somewhere between $5 and $10 billion. Three years into the AI wave, AWS’s AI run rate is nearly 260 times bigger than AWS was at the same point in its history. Not a typo. 260x.

The crazy thing is that AI revenue wasn’t even the best news. The chip business inside Amazon seems to have been underestimated for a very long time.

Amazon’s custom silicon division, which includes Graviton (’CPU’), Trainium (AI accelerator), and Nitro (networking), is now at a $20 billion annual run rate.

That doubled from $10 billion at last quarter’s earnings. On top of that, Jassy said if Amazon’s chip division were a standalone business selling to third parties like any other chipmaker, the annual run rate would be around $50 billion. That would make it comparable to Broadcom’s AI chip business.

The market assigns zero value to Amazon’s chip business because it’s buried within AWS. And yet it’s potentially a $50 billion standalone operation. That’s bigger than 82% of the Fortune 500.

Two large AWS customers asked if they could buy all of Amazon’s Graviton capacity for 2026. Amazon had to say no because, well, other customers exist.

On the Trainium side, Trainium 2 is completely sold out. Trainium 3, which just started shipping a few weeks ago, is nearly fully subscribed already. And a significant chunk of Trainium 4, which is still about 18 months away from broad availability, has already been reserved.

AWS CEO Matt Garman confirmed at re:Invent that all currently available Anthropic models were trained on Trainium. There are now 1.4 million Trainium chips deployed across all three generations, and Anthropic’s Claude runs on over a million Trainium 2 chips. Anthropic helped AWS co-design the chip from the ground up, working at the kernel level with Amazon’s Annapurna Labs team.

This all tells you something about the chip demand. For Amazon’s chips, but also chips in general. As I wrote last week, it may be time to buy Nvidia again.

Free cash flow dropped from $38 billion to $11 billion because Amazon is spending almost $200 billion in capex in 2026, mostly on AI infrastructure. That scares people. But Jassy said Amazon already has customer commitments for a substantial portion of this capex, with most of it expected to be monetized in 2027 and 2028. That includes the $100 billion-plus OpenAI commitment, on top of the Anthropic partnership.

In January, I made 5 bold predictions for 2026. I’m still confident that these two will prove to be true.

4. Anthropic: The Stock Destroyer (part 372)

At this point, Anthropic might be the single most effective stock destroyer on the planet. Every time it puts out a press release, dozens of stocks drop like a rock. The market sells first and reads the press release in full later.

It happened again this week. Anthropic announced Claude Mythos Preview, a new AI model it considered too dangerous for public release, and launched Project Glasswing, a cybersecurity initiative around it.

Mythos found thousands of vulnerabilities across every major operating system and browser, including a 27-year-old bug in OpenBSD, a system that’s famous for being unhackable and a bug that had been hiding in FFmpeg for 16 years and survived five million automated scans.

Sounds impressive, right? It is. But look at what happened before anyone even digested the details.

When Fortune first leaked the existence of Mythos back in March, cybersecurity stocks cratered. CrowdStrike dropped around 10%, Palo Alto 8%, Cloudflare 14%. The narrative instantly flipped from “cybersecurity spending is non-discretionary” to “AI will make all security software obsolete.” Billions in market cap gone in hours, all because of a leaked draft blog post.

Then, this week, the actual announcement came out. And guess what? CrowdStrike and Palo Alto were named as launch partners.

This is the pattern now. Anthropic says something, the market panics, software and cybersecurity names get slaughtered, and then people actually read the announcement and realize it’s more nuanced than “everything is dead.” But they have sold their stocks and then invent a rationally-sounding explanation like “more uncertainty.”

This fits into the anti-bubble I’ve been writing about. In the dotcom bubble, the biggest bubbles were in public companies. Think Yahoo!, Pets(.)com, Webvan and many others.

In contrast, this time, the biggest bubbles are in private markets: Anthropic, OpenAI, SpaceX, Stripe, ...

I’m not saying these aren’t phenomenal businesses; they clearly are. But the valuations are crazy. And the result is that money is being pulled out of public markets to chase these private names (see above in this Overview Of The Week for the percentage of software in private equity).

This puts more selling pressure on the public companies that are supposedly disrupted. Look at this chart that Michael Batnick shared:

This is about Wednesday and Thursday. The S&P 500 was never up this much with software down this much. This already shows you again that the movements are extreme.

Public shareholders get hit twice: once by the panic selling after every press release, and again by the capital outflows into private markets chasing the next hot AI round.

At the same time, forward earnings expectations for software stocks continue to go up.

I’m not saying Anthropic is doing this on purpose, but it’s a hypemachine. An AI model too dangerous for public release? I don’t know about you, but damn, I want to try that out! I’m still frustrated a lot with the current models, for many use cases.

The model is clearly very powerful. It found four vulnerabilities that escaped for so long. Anthropic said these capabilities weren’t even trained intentionally. They just emerged.

But the market keeps pattern-matching “new AI capability = existing companies are dead” without doing the work. The companies inside Project Glasswing, Amazon, Apple, Microsoft, Google, Nvidia, CrowdStrike, Palo Alto, Broadcom, and about 40 others, are getting $100 million in usage credits and early access. They’ll be stronger from this, not weaker. Being at Anthropic’s table is probably better than being on its menu.

If you are a paid subscriber already, you can just scroll past this. If you are not, please read this.

When you join Potential Multibaggers now, you get my entire investment system:

✅ Best Buys Now: every month, the 5 best stocks to buy

✅ My Proprietary Quality Score: Rating companies on 17 quality metrics nobody else uses

✅ Live Portfolio Access: Every stock I own, every transaction I make, in real-time

✅ Deep Earnings Analysis: Thorough breakdowns that reveal what really matters

✅ Valuations & Buy/Hold/Sell scales: Cut through the noise and know exactly when to act

✅ 15,000+ Word Deep Dives: Each pick gets 4-5 extensive articles so you understand exactly what you own. The first article alone (part 1!) is already 7,600 words. What others call a ‘deep dive’ is just the starting point of a part of an article for me. This is the work professionals literally pay thousands of dollars per report for!

✅ Private Community: Direct access to me and 800+ serious long-term investors.

Normally, this costs $1,200 per year.

But now, you can get this for just $399!

I’ve added a $800 credit to your account.

That means you can get all of this for just $399 instead of $1200!

This pick is a company I’m personally loading up on, just like many other Multis are.

Claim your $800 discount NOW!

I’ve limited this to 25 spots at $399 instead of $1,200.

This is not a fake number! There are 25, not more.

In a bull market, they’d be gone in hours. But there are spots left now.