Hi Multis

Yesterday, TransMedics (TMDX) reported its Q2 2025 earnings, as the second Potential Multibagger after Kinsale. You can read my report on Kinsale's earnings here, if you haven't already.

The Numbers

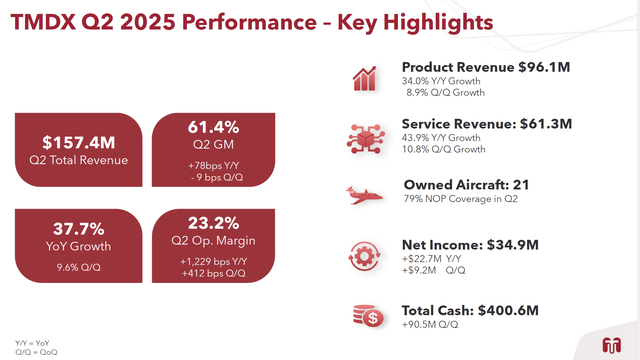

Revenue: +38% YoY to $157.4M, a beat by $9.7M or 6.6%.

EPS: $0.92, +238% YoY, a beat by a whopping $0.47 or 104%

Product Revenue: $96M, +34% YoY, +9% QoQ

Service Revenue: $61M, +44% YoY, +11% QoQ

Gross Margin: 61% (flat YoY)

Operating Income: $37M, +192% YoY, +33% QoQ.

Operating margin: 23%

Guidance: FY 2025 revenue raised to $585-605M, +35% YoY vs. the midpoint

op margin expansion +650bps in 2025, targeting ~30% by 2028

You also get an overview on this Q2 earnings slide:

(Source)

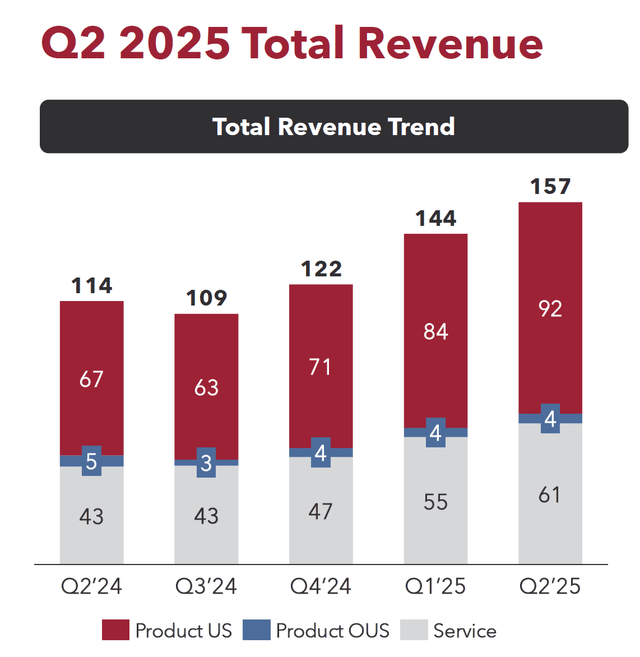

TransMedics had a great quarter. Revenue was up 38% to $157 million, beating the estimates by $10 million. The gains came from liver, heart, and lung OCS segments.

As you can see, Product was the biggest contributor, with $92 million versus $61 million.

That means service is up 41.8%, product 37.7%. That's a good balance. If service were up much more than product, it would be a red flag. And that's why I made that one of the Selling Rules for TransMedics.

My strength and weakness at the same time is optimism. To protect myself from the negative side of my optimism, I used to make selling rules, but in the last year or so, I haven't done too much with them. From now on, I will focus on them more again. These are very specific for every company. And I made them for TransMedics. More about the rest of the Selling Rules later in this article.

The company raised its 2025 guidance to $585-605 million, which means 35% growth at the midpoint. Management also said they are targeting 30% operating margins by 2028.

👉 This is just the surface. In the full write-up (for paying subscribers):

How TransMedics is quietly turning regulatory heat into a massive competitive edge

The international expansion clue buried in the CEO’s comments

How the CEO reacts to a thorny question about a competitor.

Why I gave it a 70/100 on the Potential Multibaggers Quality Score

My updated valuation, specific Selling Rules, and what could trigger a sell

If you’re not a member yet, this is the kind of deep research you’re missing.