The Trade Desk: Tough Love

This hurts, but there are two kinds of pain. One kills you, the other makes you stronger. Which one is this?

The stock market demands conviction as surely as it victimizes the unconvinced.

Peter Lynch, One Up On Wall Street

Hi Multis

Yesterday evening, I was going to finish David’s article on Global-e and publish it.

And today, I had planned to continue working on my Hims & Hers article, which I have done substantial work on, but it still needs more work.

But then came the earnings of The Trade Desk (TTD) and I dropped everything to write this article. It’s probably the most elaborate earnings analysis I have ever written.

Many Multis (and other TTD investors) wonder if this is the time to sell their long-held shares. I understand that question very well, as The Trade Desk has seen a disastrous stock chart.

That’s why I dropped the two other articles, to prioritize this one.

For sure, this hurts, but there are two kinds of pain. One kills you, the other makes you stronger. Which one is this?

This is a moment that demands nuance, context, and maybe some tough love. I still like this company a lot. But liking a company doesn’t mean you close your eyes to the ugly parts. So let’s look at everything with clear eyes, starting with the numbers.

The Numbers

Revenue came in at $847 million, up 14.3% year over year, beating the consensus by $6.32 million.

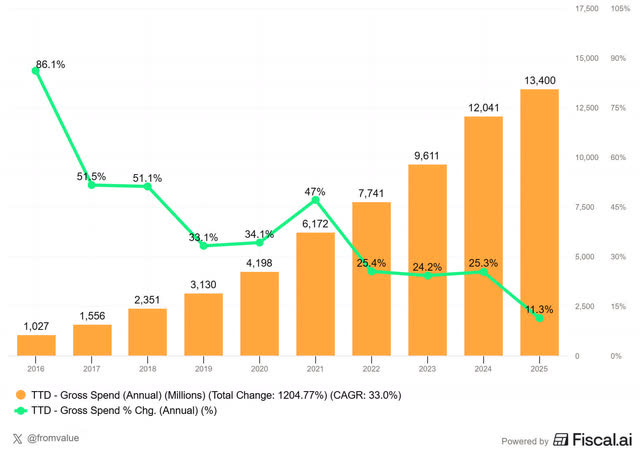

For the full year, The Trade Desk delivered $2.9 billion in revenue, up 18%. Gross spend on the platform was approximately $13.4 billion.

Now, that 14.3% growth rate looks disappointing, and optically, it is. But there’s an important caveat. Remember, Q4 2024 was a massive political spending quarter (U.S. elections). Excluding political, Q4 revenue grew approximately 19% year over year. That’s a much more representative picture. Still, even 19% is a deceleration from the 20%+ growth we were used to. I’ll come back to why.

Non-GAAP EPS was $0.59, beating the consensus by a cent. Net income was $187 million, or $0.39 per diluted share, compared to $182 million and $0.36 a year ago.

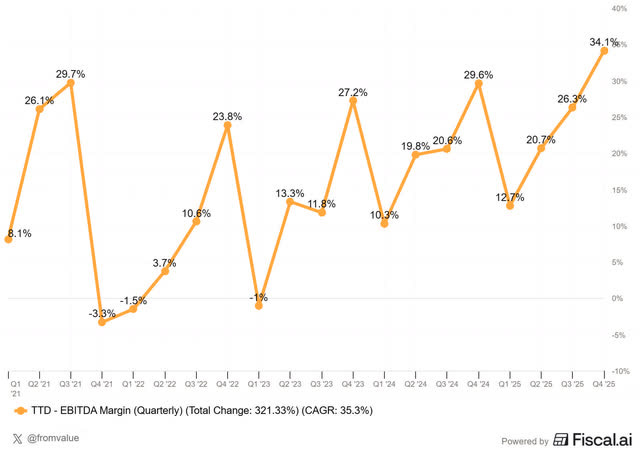

Adjusted EBITDA was $400 million, which translates to a 47% EBITDA margin. For the full year, EBITDA came in at $1.2 billion with a 41% margin. Those are still excellent numbers.

Free cash flow was $282 million for the quarter. And as always, the balance sheet is pristine: $1.3 billion in cash and short-term investments, zero debt. Customer retention stayed above 95%, as it has for over twelve consecutive years.

Up to now: OK or strong. This wouldn’t have caused a 16% after-market drop. So, what did? Guidance.

More specifically, the Q1 2026 guidance and the absence of yearly guidance.

Revenue guidance for Q1 of “at least” $678 million. That implies roughly 10% year-over-year growth. The consensus was $688 million, so that’s a clear miss of about 1.5%.

What’s not something to worry about (even if I read that everywhere) is the lower adjusted EBITDA guidance of approximately $195 million. That implies a margin of just 29%. That may seem very low compared to this quarter’s 47%, but Q1 is seasonally low.

While this is a chart of non-adjusted EBITDA margin, you can still see the pattern.

On top of that, interim CFO Tahnil Davis explained that much of it relates to infrastructure investments, specifically the transition to owned data centers and more investments in AI. She emphasized that full-year EBITDA margins are expected to be approximately the same as in 2025.

But that also points out that other painful detail: no yearly guidance. It means management is not confident for 2026 or has no idea. You know how markets hate uncertainty.

This, along with the 10% revenue growth guidance for Q1, is a number that makes growth investors like us nervous. I understand why the market reacted the way it did. But let’s look at the context behind that tepid Q1 revenue growth guidance.

The CPG and Auto Problem

Jeff Green spent a lot of time on the call explaining something he typically didn’t do until recently: calling out specific verticals. CPG (consumer packaged goods) and automotive together represent roughly a quarter of The Trade Desk’s business. And both had a very tough 2025 and that continues into 2026.

When the world hands them uncertainty, it’s often the thing that gets paused. That they would rather adjust marketing budgets than lay people off.

Jeff Green pointed out that if you exclude the impact of these two verticals, The Trade Desk’s growth rate would have been at least 5 percentage points higher. So, if you exclude political spending and the two macro-affected categories, The Trade Desk’s real revenue growth for this quarter would have been 24%.

That’s a significant difference. But the market only looks at the headlines showing 14% revenue growth in Q4 and 10% guidance for Q1. An overwhelming majority of so-called investors are not interested in the explanation. The stock price reflects what people see at first sight, not what they should see after adjustments. That’s the reality The Trade Desk has to live with right now.

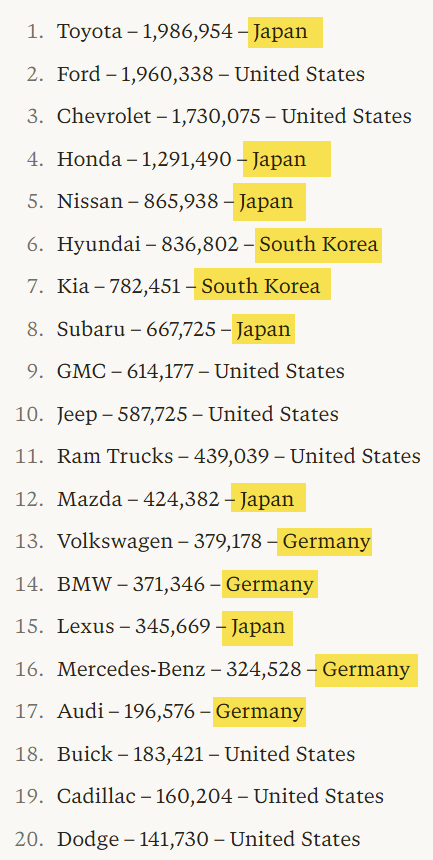

Multi Market Sense may have been rolling his eyes. He wrote in our community:

“GM stock is all time high. Auto spend reduction?”

True, of course, but that comes from the same dynamics. Foreign cars have become much more expensive in the US, so they cut their ad budgets. People see that US cars are relatively cheaper and buy those. Or, to put it differently, you will not cut your ads if you are GM, but you will if you are one of the foreign brands. This is the top 10 of the most sold cars in the US in 2024. 6 of the top 10 are foreign car brands and 12 of the top 20.

The biggest negative was the Q1 guidance. There are two major reasons. First, the CPG and auto weakness that continues in Q1. Just look at the impact.

Food & drink is not all CPG, but this shows that at least a quarter of The Trade Desk’s business is under macro pressure.

Don’t forget that Q1 2025 didn’t have tariffs yet, so the comps are still tougher.

Professor Jeff Has A Tough Semester

As usual, the conference call was a Jeff Green masterclass. But this time, the professor had a harder task: explaining to the unwilling class of analysts why the grades slipped while insisting the curriculum is still working. I’m not 100% sure that comparison works, but you know what I mean.

Let me walk you through the most important insights.

On the supply-demand imbalance

Green said that in 2025, more ad supply was added to the global market than in any year before.

This is a very strong validation of The Trade Desk’s model: when there’s more supply than demand, it’s a buyer’s market. The company that helps buyers make the best decisions (The Trade Desk) wins. Jeff Green backed this up with a great example, not coincidentally about Amazon.

One of the world’s leading appliance manufacturers recently ran a test between The Trade Desk and the Amazon DSP. Focusing on CTV ad performance in one of their most important markets. They found that with The Trade Desk, they were able to reach 70% more unique households because we gave them access to a much wider range of relevant touch points with those consumers.

With The Trade Desk, they were able to reach those consumers at 30% lower total cost, so significantly better reach for meaningfully lower cost. And the kicker is The Trade Desk platform performed 6x better in terms of delivering their campaign goals.

That’s a compelling data point. Not just theory from Professor Jeff but real, measurable results. Not that the market cares. The story is that Amazon crushes The Trade Desk, and if the market wants to believe it, it will, no matter what the facts say. More about Amazon later in this article, of course.

On the walled gardens “cheap reach” problem

This is a theme Green has hammered for years, and it’s becoming increasingly mainstream. He quoted Vinny Rinaldi, a VP at Hershey’s, who described the industry’s obsession with cheap reach as a “fallacy”:

For the past 15 years, marketing success was measured by one dominant pursuit: cheap reach. The advertising industry became enamored with scale over substance, equating impressions with effectiveness.

Green loved the quote so much, he said:

I couldn’t have written a better description of the difference between The Trade Desk and the open internet and walled gardens.

For those who need a bit more context, basically, it’s said that the cheap ads in walled gardens like Facebook, Google, etc. don’t have the same impact and if you measure everything, they are actually a worse investment of advertising dollars.

In his typical way, Jeff Green could point to where the problem is and what Vinny Rinaldi means:

Nobody typed in, 'Buy Mercedes-Benz,' into Google without seeing the commercial or hearing about the company before that. Giving all the credit to the last touch has been a serious mistake.

Green compared it to a football team. Only rewarding the one who scores the goal and not the rest of the team is ridiculous.

And Green quoted a VP of Strategy at a large agency:

"Even though a large commerce walled garden may trump at 1% or no fees, at the end of the day, the effective CPM that we pay is higher than comparable campaigns on The Trade Desk. We're paying more to get less functional reporting, and we are spending a lot more on data than we would have on the comparable Trade Desk campaign."

Green added to this:

Our goal is not, nor has ever been, cheap reach, which ultimately slows growth because it is ineffective.

Quite convincing.

On AI and agentic

Green repeated that AI is not a threat to The Trade Desk but a massive tailwind. I want to add here that the company has been using AI since 2017.

He emphasized that AI is only as good as the data it has access to, and The Trade Desk’s unique combination of objectivity, trust, and massive data assets makes it arguably the best-positioned company in ad tech to benefit.

An AI company in the advertising space must have the data and the objectivity to make any sizable scaled and sustainable progress.

He went further, directly addressing the bearish outlook on SaaS companies that has taken the market like a fever recently.

There is an emerging narrative that AI will compress software value or disintermediate platforms altogether. That might be true for some SaaS businesses, especially those that deal in generic process or low-grade data. However, for platforms that have earned the trust of their clients and partners and have a mass data that is scaled, unique, refined and actionable, they are in the perfect position to leverage advances in AI to add more value.

In short: AI will change how brands reach consumers, but it won’t eliminate the need to reach them.

Innovation: Audience Unlimited, Deal Desk, and Simplification

Green spent significant time on three product innovations that deserve attention.

Audience Unlimited is already applying agentic AI. The underlying thought is simple but powerful: third-party and retail data have been underutilized in programmatic advertising for twenty years, primarily because there has been no price discovery for data. Marketers either overpay or, more commonly, just don’t use it. Audience Unlimited uses a flat cost structure combined with agentic AI to surface the right data segment at the right moment for any given campaign.

Early results are positive, and the rollout continues through 2026. This is an interesting one and I think it may be a card up The Trade Desk’s sleeve.

Retail media continues to grow. Spend influenced by retail data hit record levels in 2025. The Trade Desk’s retail marketplace now covers more than half of global retail sales, according to Green. A Cheerios campaign in the U.K. using retail data saw 88% more conversions and 7x better CPA. Nestlé plans to activate retail data across most of its future campaigns, including audio.

Deal Desk, which I already covered in my Q3 article, continues to gain traction.

Deal Desk tackles a problem that’s surprisingly common in programmatic advertising: the one-to-one deal that sounds great on paper but never actually works.

A one-to-one deal is where a buyer and a publisher agree on a deal upfront, agreeing on how much ad space they will buy at what price. Sounds simple enough, right? But in practice, the overwhelming majority of these deals fail to scale. Most of these deals never work as intended. Green said that historically, 90% of them never reached meaningful spending levels. They were set up poorly, hard to fix if something goes wrong, or the results were very poor.

That’s a big waste of time and money on both sides. Deal Desk uses AI to forecast how a deal is likely to perform before the buyer commits, and flags where things might go wrong. More publishers are signing up every week, including the two largest SSPs in Germany.

Overall, the concept of simplification underlies multiple themes. It is what The Trade Desk aims to achieve for its customers, and I think that’s a great idea.

Green acknowledged something that The Trade Desk’s critics have long pointed out: the platform’s complexity can be a barrier. The company is making big efforts to simplify UX, billing, measurement, and supply chains.

And it’s already starting to pay off:

Our efforts in simplification are already working. IKEA, for example, is using Kokai to get a more intelligent perspective on how their ads perform across all channels. Thanks to Kokai's AI-fueled omnichannel optimization, they saw cost per acquisition decrease by 17%, while also gaining valuable new insights on the effectiveness of different channel activations at different stages of the customer journey.

The Amazon Question (Again)

This comes up every single quarter, and Green addressed it head-on again. His answer hasn’t changed, and it shouldn’t have, because his analysis is correct.

People want to talk about Amazon a lot as it relates to competition. As I said before, I think Google was a far better competitor than Amazon is today, or frankly, will likely ever be.

He pointed out that Amazon’s DSP is essentially a tool for monetizing their own inventory, so their website and Prime Video. Around 95%+ of Amazon’s ad revenue comes from sponsored listings and owned-and-operated content. The actual spend going to the open internet through Amazon’s DSP is minimal.

In 10 years, I don't think Amazon has a DSP as we define it.

That’s a bold prediction. But Green has been making bold predictions for years, about cookies, about CTV, about identity, and his track record is, as I’ve mentioned multiple times before, essentially flawless.

He went even further than in Q3, making clear how Amazon faces a fundamental conflict of interest:

Amazon is mostly playing in selling their owned and operated inventory as well as trying to win on nondecisioned inventory. They can't compete on decision because if they say that they're objectively trying to buy the open Internet and then spend most of the money on their owned and operated where they make all their money, then it imposes some hypocrisy or creates some channel conflict.

He also made a very honest observation about the trade press that is very revealing:

The trade press has not been super friendly to us. When we talk to some of the editors-in-chief at these firms, they'll say things like: 'Your name gets clicks, especially when it's negative or controversial.'

We all know that this is true. I see it myself. If I put out a tweet about The Trade Desk, it does better than my other posts. And I’m pretty sure this article will get better views than average.

The Trade Desk and Amazon are playing in fundamentally different sandboxes, as Green likes to say. Correlation between Amazon’s ad growth and The Trade Desk’s deceleration is not correlation, not causation.

Operational Upgrades: The Growing Pains

This is the area where I think the tough love is most warranted. The Trade Desk has undergone major organizational changes: a new COO, a new CRO (Anders Mortensen, from Google, who joined only weeks before Q3 earnings), and a new CFO (Alex Kayyal, who was already gone by Q4 replaced by interim CFO Tahnil Davis).

That’s a lot of leadership turnover. Green was open about why:

The people that we had at the time we were public, especially as a leadership team, are not the same people that we need to take us from $3 billion to $10 billion.

This is a very well-known problem in business. I call it an inbetweener. A company that scales usually goes through a period of painful transition and, frankly, blunders. Think of the Netflix Qwikster debacle, for example. Or Shopify buying and selling Deliverr within 9 months and a big management turnover as well. Tobi Lütke talked about this problem very insightful in this podcast episode.

I could give more examples, as there are many, but you get the point.

Green said the right things that fit in this context. He talked about accountability, clear roles, and growing from ad-hoc agility to operational execution.

The result starts to show up. Joint Business Plans (’JBPs’) now account for well over half of the business, and the JBP pipeline has more than doubled. That’s encouraging. Of course, I want to see this show up in the numbers before I give full credit for the better pipeline.

The CTV story remains strong. Video (including CTV) accounted for about 50% of the business in Q4 and grew faster than the company overall in 2025. Another rebuttal to the “Amazon is killing The Trade Desk.”

Audio was the fastest-growing channel in Q4 and now accounts for about 6% of revenue. International continues to outpace North America, with EMEA and APAC showing strong momentum. These are all positives.

Conclusion

I just checked the stock price before this conclusion and I was surprised to see that the market seemed to recognize the same things as I. The stock was down 16% yesterday, but now just a bit over 4%.

Of course, if you read the headlines, you see 14% growth, which would have been 19% ex-political spending and more if CPG & automotive hadn’t suffered from the tariffs.

With the weak Q1 guidance, the CFO seat uncertainty, and the stock down 83% from its high, it’s a lot to take for investors.

When I read the headlines, I was leaning on the negative side as well, but I think we should give The Trade Desk leeway. Jeff Green has deserved that during all those years.

The structural story hasn’t really changed. CTV is still growing, retail media is still growing, the walled gardens are still conflicted, AI is still a tailwind, the balance sheet is strong, and Jeff Green is still by far the best CEO in adtech.

What has changed is the macro environment for specific verticals, the execution bar and of course, the market’s patience. If a stock drops so much, every little detail is magnified to explain the drop. And of course, there are some scratches and dents, but I don’t think this car is fundamentally weaker than it was a few years ago.

Green said something that resonated with me:

Despite the fact that I don't think that this is our best earnings report ever, I hope you can hear it that I am as optimistic as ever, and that's largely because we're improving all of these things

I like that he’s so straightforward about this not being the best earnings report, and I believe him. And I share that optimism for the long term. But I also think this is a company that needs to prove to the market that the operational improvements and product innovations translate into reaccelerating growth. The seeds are planted and the JBP pipeline is strong, so there are signs. But trust takes years to get and seconds to lose. In other words, it could be that The Trade Desk is under pressure for longer than just the turnaround.

The latter half of 2026 should be better for The Trade Desk, as the tough comps are leapfrogged then. Tariffs were already in place. Add the World Cup Football/Soccer in the USA, Mexico, and Canada, mid-term elections, and more execution on the new initiatives, and we should see improvement there. If CPG and auto stabilize, that would be an extra boost.

I’m sure by now that I’m keeping my position, which I was not before I started this article. But I’m watching it closely. The next few quarters will tell us whether this is the bottom of a temporary dip or the beginning of a longer problem. I believe it’s the former, but belief doesn’t bring winners. Execution does.

The Selling Rules

To be honest, I had to work hard on these. I wanted to make them to be very strict and realistic and especially relevant.

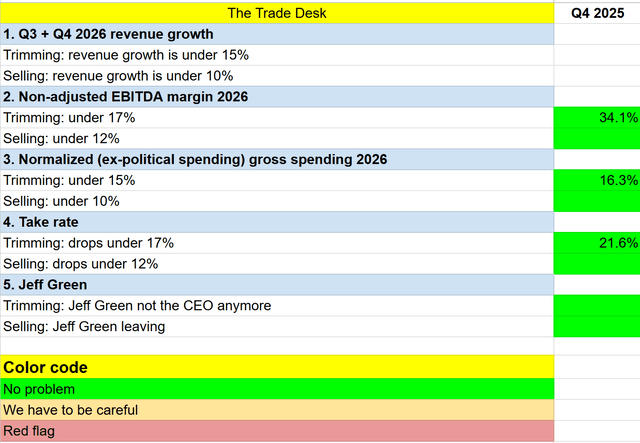

1. Q3 + Q4 2026 revenue growth

It’s simple: if revenue growth doesn’t tick up, the thesis is mostly broken. I understand the reasons for the seemingly lower revenue growth in this quarter. The political revenue should be back in Q3 and partly in Q4. And while I understand there’s an impact from CPG and automotive in Q1, that should get better too, as in Q3 and Q4 it was already the case. If The Trade Desk doesn’t grow its revenue more than 15%, unless there’s a really good reason, let’s say a general down economy, for example, then it’s using macro as an excuse.

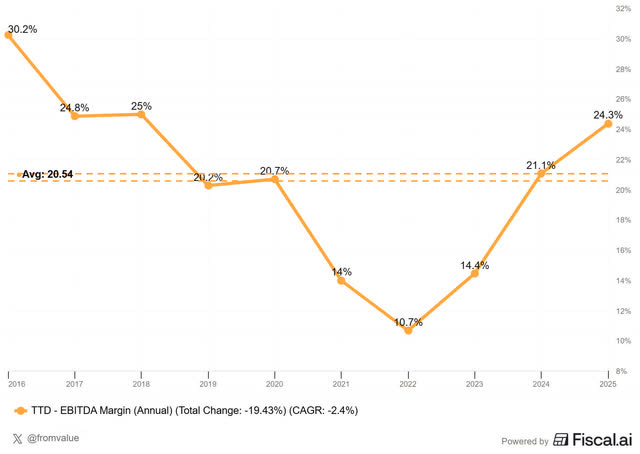

2. Non-adjusted EBITDA margin 2026

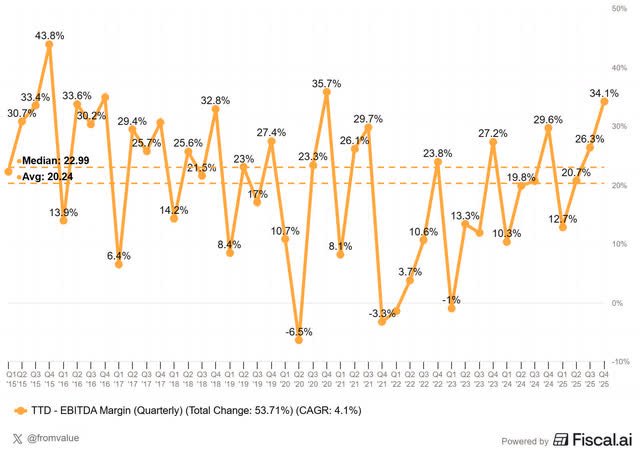

Why EBITDA margin? It shows pricing pressure. Now, as you can see in this chart, it fluctuates heavily quarter by quarter. And there will be an influence from The Trade Desk building and hosting its own data centers, but even then, margins should recover.

If you look at the long-term average and median, you see that both are around 20%.

Of course, there will be some impact from the data center investments, as said. That’s why I take 17%. If the margins are under 12%, unless there’s a general market weakness as in 2022, I will sell.

3. Normalized (ex-political spending) gross spending

Gross spending is the total amount of money that customers spend on the platform. In 2025, that was $13.4 B. That was up just 11.3% up YoY. But adjusted for political spending, we assume that would have been 5% higher.

4. Take rate

The take rate is the gross spend on the platform divided by the revenue. That was a very strong 21.6% in 2025. If this starts to crumble, it’s a sign that The Trade Desk’s pricing power is decreasing and its competitors put it under pressure to lower prices.

Edit: Multi Anthony asked a great question in this context: isn’t take rate crumbling compared to the previous years? I know that’s the story out there, so I loved this question enough to edit this article.

In 2024, the take rate was 20.3%, in 2023, 20.3%, in 2022, 20.4%. So 2025 was actually slightly stronger than the previous years, and the eroding take-rate story does not show up in the numbers.

5. Jeff Green

Jeff Green breathes and bleeds digital advertising. He has been part of the investment thesis from the start. Therefore, if he leaves, it would be a huge red flag to me.

Up to now, The Trade Desk lives up to the Selling Rules, but the gross spending criterion is close.

Let’s move on the PM Quality Score. Is that impacted by the weaker Q1 prospect?

If you are not on the paid plan yet, this is where the article ends for you. Do you want to know if The Trade Desk is a buy right now?

Go to this page.

Subscribe to the annual plan.