The truth is that you don’t know what is going to happen tomorrow. The market will fluctuate.

Peter Lynch, One Up On Wall Street

Hi Multis

Last quarter I wrote an article called “Tough Love.“ I gave The Trade Desk (TTD) the benefit of the doubt, kept my position, and told you the next few quarters would tell us whether this is a temporary dip or a longer problem.

Well, we have one of those next quarters. And on the things that matter most to the market right now, it’s probably worse than that of Q4 2025.

The stock initially dropped about 14% in after-hours and closed Thursday’s session down roughly 8% at $23.49. We are down around 85% from the all-time high. That’s tough. For you, for me and for everyone who is not a psychopath.

Last quarter, I said “trust takes years to get and seconds to lose.” That sentence is still key. I have not lost my trust completely, but it’s wearing thin. I’m writing this article with a sharper pencil than usual and that’s because these results warrant that. But I might also have found the reason why The Trade underperforms and cannot really communicate it straightforwardly. Let’s dive in.

The Numbers

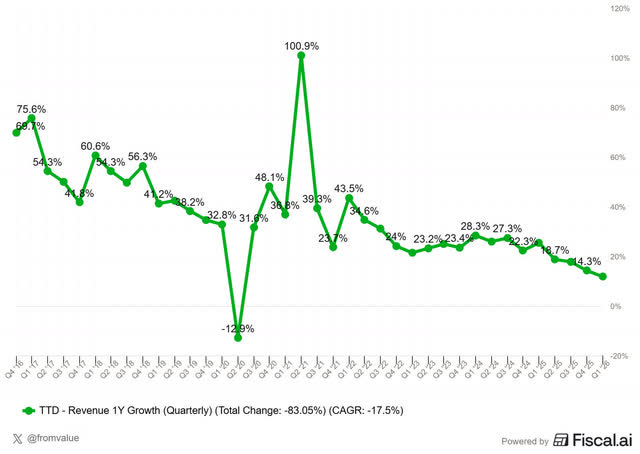

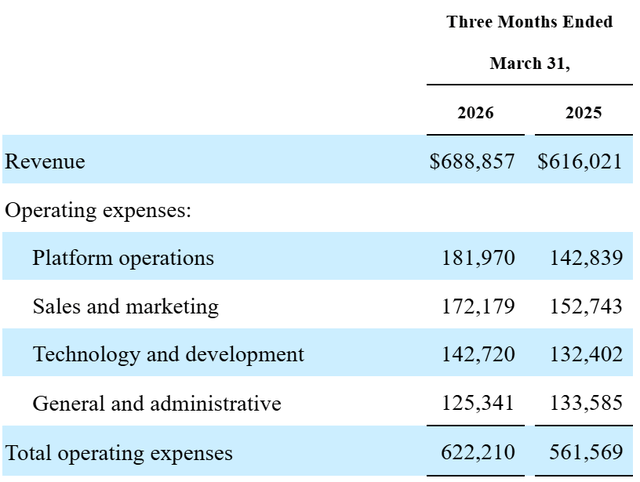

Revenue came in at $689 million, up 11.7% year over year, beating the consensus of $678.7 million by about 1.5%. A beat is a beat but the growth rate is the slowest since the IPO, with the exception of the first full quarter of the COVID pandemic.

Did you know that Fiscal now has a 25% off promotion? Use it now!

Non-GAAP EPS was $0.28, missing the consensus of $0.32 by about $0.04. GAAP net income was $40 million, or $0.08 per diluted share, down about 20% year over year. Adjusted net income was $134 million.

Adjusted EBITDA was $206 million, a 30% margin, down from the mid-30s a year ago. Q1 is always the seasonally lowest margin quarter (always remember that), so part of this is just the calendar.

Within the costs, operating expenses were up 10.8%.

Source: The Trade Desk’s Q1 2026 10-Q

I saw some pointing out that the costs for platform operations were up “unsustainably.” And yes, they grew 27% YoY (from $143M to $182M). But that’s a long-term investment in self-owned data centers and AI infrastructure. That’s also the main driver of the EBITDA margin compression we see in this quarter. All in all, I think it’s good that the company invests in its own data centers and AI infrastructure, so I don’t have a problem with the margin compression as long as it’s not outrageous, which this was not.

The real question is whether the investment will pay off in reaccelerating revenue. So far, it hasn’t, but often, these things need time.

Free cash flow was excellent: $276 million on $392 million of operating cash flow. The free cash flow margin came in at 40.1%, up 2.4 percentage points YoY. This is the best part of the report. It shows that the underlying earnings power of the business is still very much there.

The balance sheet also remains top-notch: about $1.4 billion in cash and short-term investments, no debt. The Trade Desk repurchased $164 million of its own shares in the quarter and still has $327 million remaining under its buyback authorization.

Customer retention stayed above 95% for the 12th consecutive year. I have already pointed out that it doesn’t mean all that much in that sense; it’s not DBNRR or a dollar-based net retention rate. Years ago, when asked, Jeff Green argued convincingly that DBNRR doesn’t mean that much because it is very campaign-driven. I understand this, but it doesn’t say if the average customer has spent more or not over the last year or years.

SBC remained elevated at roughly 16% of revenue, which means the buybacks are mostly offsetting dilution rather than meaningfully shrinking the share count, although the basic shares were still down about 4% YoY.

So you have a revenue beat, an EPS miss, margin compression, very strong cash generation, and continued buybacks. That’s what I would call a mixed report on the headline metrics. That alone wouldn’t have crushed the stock so much, I would argue. But guidance did.

The Trade Desk guided Q2 revenue of “at least” $750 million, against a consensus of about $770 million. That’s a 2.6% miss on the guide. More importantly, it implies year-over-year growth of just 8.1%.

Single-digit growth. From a company that grew 26% the year before. There is no nice way to put it: this is awfully weak.

The Deceleration: Five Quarters Now

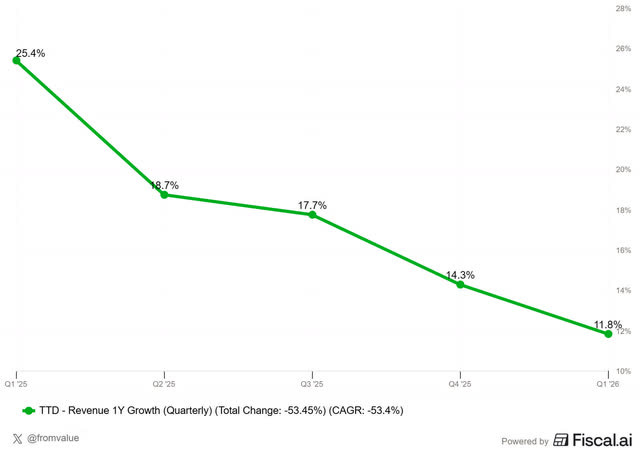

I already showed this before, but let’s zoom in a bit here.

Q1 2025: 25.4% growth, Q2 2025: 18.7% growth, Q3 2025: 17.7% growth, Q4 2025: 14.3% headline (about 19% ex-political, to be fair), Q1 2026: 11.7%, Q2 2026 guidance: 8.1%.

Some decelerating growth is normal from a certain size, but this is much too fast and worse, the deceleration has accelerated. This is no longer just “tough comps” or “political spending normalization” or “CPG and auto headwinds.” Those things are real, mind you, but they are not enough for me anymore to fully explain a company going from the mid-20s growth to 8% guidance in five quarters. This is also the longest deceleration streak in The Trade Desk’s public life, not a record you want to hear about.

The Q2 guide of about 8% growth is roughly in line with global digital ad growth forecasts (Dentsu projects 6.7% for 2026), but it is well below the growth rates expected in the channels where The Trade Desk most heavily plays. The IAB projects US CTV growth of 13.8% and commerce media of 12.1% in 2026.

The Trade Desk has long pitched itself as concentrated in the fastest-growing parts of digital advertising, so the right comparison is not the broad industry average but those specific channels and against those, the gap is meaningful.

When asked about this, Green’s answer was:

We are uniquely one of the few large companies that are focused on being a buying platform for large companies. So most of our revenue comes from Fortune 500 companies and their brands. And of course, they respond differently to macro factors than smaller companies or local businesses, especially when the headwinds are macro and global in nature.

There’s truth in that. Big-brand spend is more macro-sensitive than small business or DTC spend. But it’s also, partly, an excuse. Last quarter, I wrote that excuses are never good. They might be true but they are still excuses. The very best companies prevent having to make excuses. And for a very, very long time, The Trade Desk used to be such a company.

When an analyst said that industry digital and video growth expectations are above 8% this year and asked why The Trade Desk is guiding below the industry, Green didn’t really answer directly. That too is not what I’m used to from Jeff Green. He always had a teflon layer, but he was refreshingly open to give context to criticism. Here, he pivoted to easier comps in the back half, but that doesn’t really answer the question. The question deserved a better answer than it got, and the deflection itself may be a signal that he does not have a clear explanation for why a company that has historically outperformed the market is now guiding to underperformance versus that market. This definitely worries me.

Something else that jumped out to me, but in a positive way this time, were margins. The full-year adjusted EBITDA margin guide is “at least 40%, approximately in line with 2025.” Sounds fine and unremarkable at first. And to be honest, I missed it the first time as well. That’s why if things are rocky and a company goes through a tough phase, I always listen to the conference call first and then the next day (preferably) also read the transcript. It was when I read that this jumped out to me.

Q1 came in at a 30% adjusted EBITDA margin. The Q2 guidance is $260M EBITDA on $750M revenue, so that’s about 34.7%. So, the average for H1 is 32.4%. That means H2 has to deliver an adjusted EBITDA margin above 47% to hit the full-year 40% guidance. That can mean two things: either management put the bar too high or the investments should pay off in H2. If it’s the first one, it’s another red flag and that’s why I add it to the Selling Rules. Yes, we are dealing with an interim-CEO, but I don’t care. She should do her job as well as anyone, as it impacts the company.

I want to stress that, when it comes to the Selling Rules, none are a thesis-breaker on their own; together, they paint a clearer picture of how the company executes. Sometimes, breaking one Selling Rule will be enough to sell, but there’s always context and if that context makes sense, applying the Selling Rules mechanically doesn’t make sense.

The Worrying Departure Pattern

Last quarter, I described the management churn as an “inbetweener” problem, common to companies scaling from $3 billion to $10 billion. I quoted Jeff Green on the need for different leaders at different stages in a company’s life and that definitely makes sense. I gave it the benefit of the doubt.

But the worrying thing is that this pattern continues. This quarter, Adweek broke the news, on the morning of earnings, that Samantha Jacobson, The Trade Desk’s Chief Strategy Officer, is leaving for OpenAI. Here I saw a glimpse of the Jeff Green I know, in his classy answer when a question came:

On a personal level, working with Samantha has been one of the highlights of my career. (...) She’s smart and humble, and she’s just generally amazing.

It’s also a good sign that Jacobson stays on the Board of Directors. That softens the blow. Green’s track record on hiring has historically been strong. But does he still have it?

In the last year or so, The Trade Desk has appointed a new COO, a new CRO (Anders Mortensen, from Google), a new CFO (Alex Kayyal, who left within months and was replaced by interim CFO Tahnil Davis), and now lost its Chief Strategy Officer to OpenAI. And don’t forget that in September 2023, co-founder and former CTO Dave Pickles also left the company. That is a lot of senior-level turnover, and people generally don’t leave a strong and winning company at this rate. The interim CFO label is also still on the books, which is itself a signal that the seat hasn’t been filled with conviction.

It might be deliberate upgrading, as Green phrases it, but it might also be instability. The honest answer is we don’t know yet. But I do know I want this pattern to stop soon, so the full attention can be given to the customers and serving them in the best possible way, instead of internal operations.

Is This The Explanation For The Slowdown?

Another thing that has been a drag for too long is the public dispute with one of the world’s biggest ad agency companies, Publicis. That has been going on for over a quarter now. Green’s response was deliberately short:

Since 2018, we’ve done billions of dollars of business with Publicis through the agreement that we have. And we continue to have a great dialogue with Publicis about the next chapter of our partnership. Our negotiations are ongoing. It’s probably not prudent for me to say more about it in this forum.

That’s corporate-speak for “we don’t have this resolved yet and I’m not going to give you any info.”

Of course, a dispute with one of your biggest customers is never a good situation, but I noticed something in this context worth pointing out. It could explain the situation The Trade Desk is in and it would also explain why Jeff Green is not as open as usual.

But before I explain what might be going on here, let me tell you a bit more about the dispute with Publicis. The company said it did an audit on The Trade Desk’s practices and found issues with fees, opt-ins and other things. It recommended that clients not work with The Trade Desk anymore. Omnicom, another big ad agency, also launched an audit on The Trade Desk. The ironic thing is that ad agencies are notorious for not being transparent, while The Trade Desk is generally seen as the best player in the business when it comes to transparency.

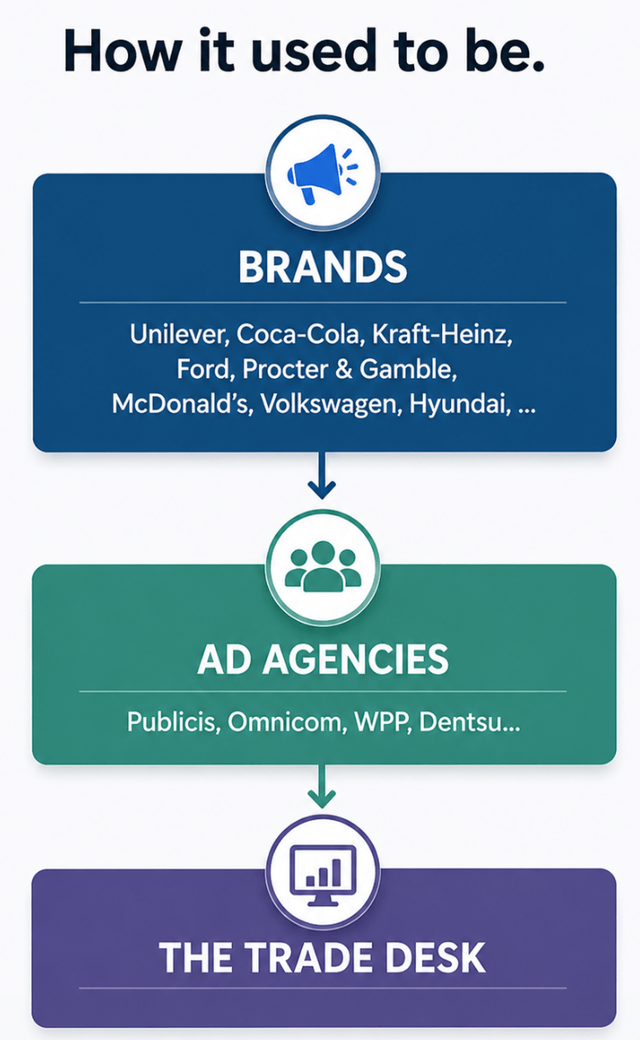

And it’s not just Publicis and Omnicom. Companies like kWPP and Dentsu have pulled back from several The Trade Desk programs, such as OpenPath. What you have to know is that this is how this business used to run.

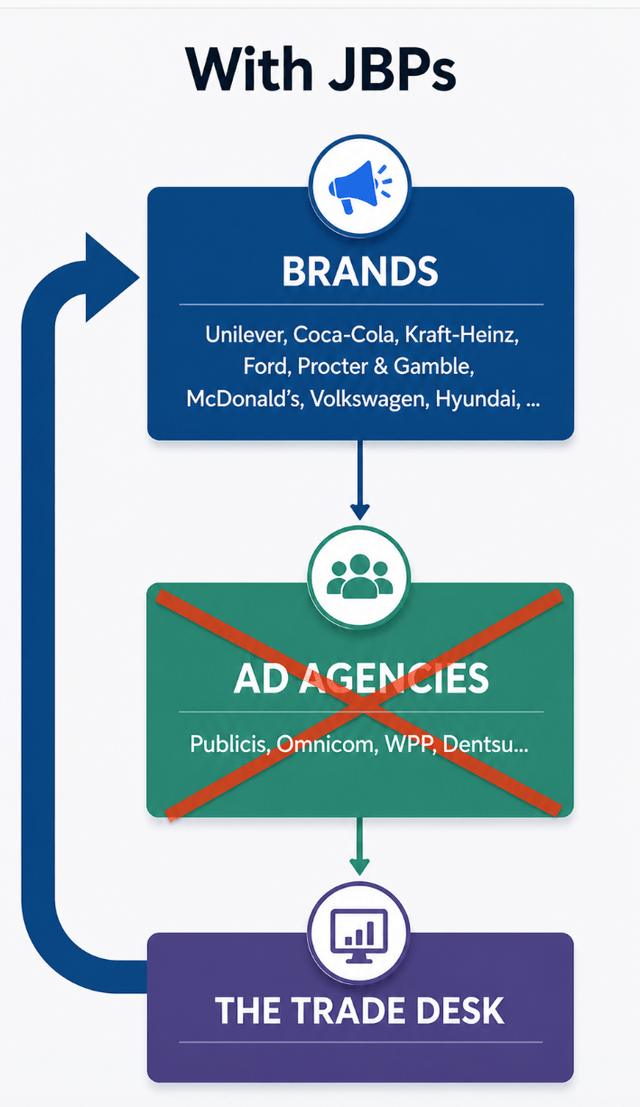

So, you can imagine how important these ad agencies are for The Trade Desk’s revenue, right?

What blew me away in the results The Trade Desk just published is that the JBPs grew 55% YoY.

Green on the earnings call:

March was our biggest month on record for JBP signings. We signed 45 JBPs in March alone. For Q1, our total JBP count grew 55% year-over-year. And excluding renewals, new JBP deal spend grew 40% year-over-year during the quarter.

That’s incredible growth. JBP stands for Joint Business Plan. It’s a strategic partnership between The Trade Desk and mostly brands (some are with ad agencies as well). These deals include committed ad spend, shared growth targets, priority access to beta features and data, and co-marketing support. But, very important, it’s a direct relation with the brands, not through the agencies.

Cutting out the middleman and going directly to brands is, of course, very positive for The Trade Desk. But the problem is that by circumventing ad agencies, it bypasses its biggest customers. This is how it looks with JBPs.

Both images were made with ChatGPT based on schemes I had drawn on a piece of paper

I can imagine that Publicis and other ad agencies are angry about the JBPs, which largely put them out of the picture. That can make them cut spending on The Trade Desk’s platform and, using their influence with brands, discourage them from using The Trade Desk. They are being circumvented and feel their power slipping through their fingers.

That would be a positive for The Trade Desk’s direct relationship with the world's biggest brands, but it would also explain the weakness in the company’s earnings. The JBP’s 55% YoY growth should fire revenue growth on all cylinders, but if ad agencies cut their spending, that will offset the JBP growth. In the long term, though, this could prove very favorable for The Trade Desk. It could cut out the middleman and have higher margins. Is that also a part of the reason for the high EBITDA guidance for the year? I believe so.

It would also explain many of the other things I see that are not typical of The Trade Desk. I have followed this company since its IPO in 2016 and I have been an investor since May 2019, 7 years ago. If what I think is happening is true, it’s a huge, difficult and probably dangerous positioning shift for The Trade Desk.

It would explain why Jeff Green, who has never been afraid of some bold statements, is so careful right now and can’t say much. After all, if he tells the truth of what’s going on, he confirms the ad agencies’ biggest fear. It’s a process that has been going on for years, probably starting with OpenPath, which SSPs (supply-side platforms) saw as intruding on their business. Green can’t comment too much on what’s going on.

He always downplayed the insinuations of The Trade Desk going into the SSP industry with OpenPath and of course, he should do the same with ad agencies. As the ad agencies seem to choose an open war, fearing for their long-term existence, Jeff Green can’t be as open as he usually is because these are his biggest customers.

It would also at least partly explain the management turnover at The Trade Desk, maybe even starting as early as Dave Pickles in September 2023. If Jeff Green had had this as his secret master plan all the time, it would have felt extremely dangerous from the start. It’s hard to disintermediate your biggest customers by cutting them out and going to their customers directly. That’s what’s happening right now. It’s a very dangerous and risky game, but if Jeff Green can pull it off, it will be a revolution in the business.

If this has been the plan from the start, it also explains why someone like Jeff Green, who has been an incredibly visionary CEO for so long, now suddenly looks like having lost his touch. In reality, he would be pulling off the biggest disruption in the advertising business. A very risky one, I stress that again, but a potentially extremely lucrative one if this succeeds. I can imagine that many of the leaders disagree with this disruption to the business model that has worked for so long. They, too, probably think that Jeff Green lost it all of a sudden.

If this is true, there could be multiple quarters or maybe even years of underperformance during the transition, but in the end, The Trade Desk should come out much stronger, as it has eliminated a powerful middleman.

It would also explain why Jeff Green is still so incredibly insightful to listen to when it comes to the ad industry. If you want a master class on where the industry is going, Jeff Green has always been by far the best source.

The most striking moment for me was a quote he attributed to a partner at an AI-first company:

You cannot overtake 15 cars in sunny weather, but you can when it's raining.

That’s an F1 line, and it’s a great one. The argument is that the brands and platforms that get disciplined and data-driven during macro pressure are the ones that emerge with bigger market share when the weather clears.

It’s been raining for a while already, and right now, it looks like The Trade Desk is the car losing positions, not gaining them. Put differently, there’s a gap between the storytelling and the scoreboard. But if what I said above is true, that’s normal.

Reacceleration isn't really about reinventing ourselves. It's about executing against a larger and expanding opportunity.

In the context of the JBPs and what’s going on, this is interesting.

Amazon competition

Jeff Green has not changed his story on Amazon. He acknowledges it’s a strong competitor and partner but that’s not the reason for the slowdown. Of course, you can only trust his words here, as you can not see the numbers. With what I mentioned above about the JBPs, it’s totally believable that what Green says is true. He tried to convince analysts with an example.

Our pharma team recently went head-to-head against Amazon for one of the largest pharmaceutical advertisers in the world. Lured by seemingly low rates, this brand shifted some investment to PG on Amazon last year. Over the past 9 months, our team delivered consistent partnership and focused on driving real business outcomes for the client. In Q1, our team won back the business and signed a JBP for 2026 that will increase their spend on our platform by 114% year-over-year.

A 114% spend increase from a brand that briefly defected to Amazon and came back. This is a real datapoint against the “Amazon is eating The Trade Desk’s lunch” narrative. The biggest brands are voting with their dollars when given a fair test. Of course, it’s always possible that this is an outlier, but I genuinely don’t believe so. I think the “Amazon eats The Trade Desk” story is just that, a story. The company has competed successfully against Facebook, Google and Amazon, so why would that suddenly have switched so fast? Again, the JBP story explains what could be going on in reality.

So far I've shown you what's happening. The harder question is what to do about it. Below the line, I go through every Selling Rule I have made for The Trade Desk, update my Quality Score, my valuation and I conclude with a Buy - Hold -Sell rating. Want to unlock these? Subscribe here.