Hi Multis

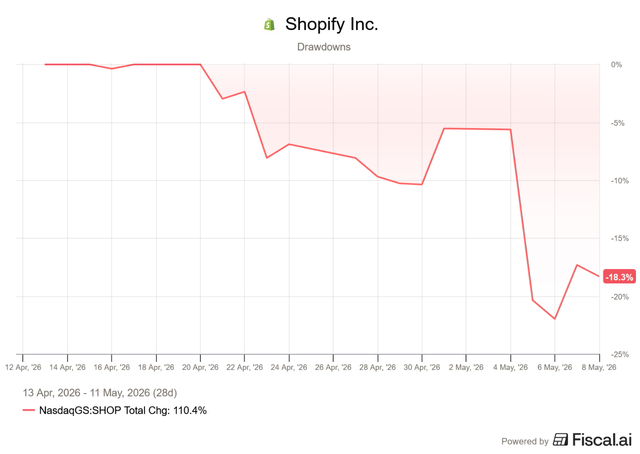

Shopify (SHOP) reported its earnings last week, just like so many Potential Multibaggers. And just like many Potential Multibaggers, the stock is down a lot.

Ok, compared to that 85% drop in 2022, that 46.7% drop doesn’t look too dramatic. But it’s still a big drop.

It’s also a lesson, as this is one of my best investments ever. It’s an 11-bagger since I first picked it in May 2017, but it was a 20-bagger already twice. That volatility is just what you have to be able to endure if you want long-term winners.

So, the question you and I have is: “Is this a buying opportunity or not?” Let’s find out together. Zack was happy to do the first part, the earnings analysis. I see you back for the Selling Rules, the Quality Score and the Valuation.

Hi Multis!

Zack here, excited to kick off my Q1 2026 earnings season with Shopify.

Selling off software continues to be in vogue this quarter, with Shopify taking a significant ~20% drop after earnings, followed by a slight recovery since.

What happened? Is Shopify continuing to execute despite the prevailing AI narrative? Read on to find out.

The Numbers

Total Revenue for Q1 came in at $3.17B, growing 34% year-over-year, beating estimates by 2.7%. This is a strong follow-up after their first-ever $3B+ quarter in Q4 2025. Don’t forget that usually, Q4 is by far the best quarter for an e-commerce company and Q1 is seasonally weaker. An e-commerce business that does more in Q1 than Q4 is showing outstanding growth.

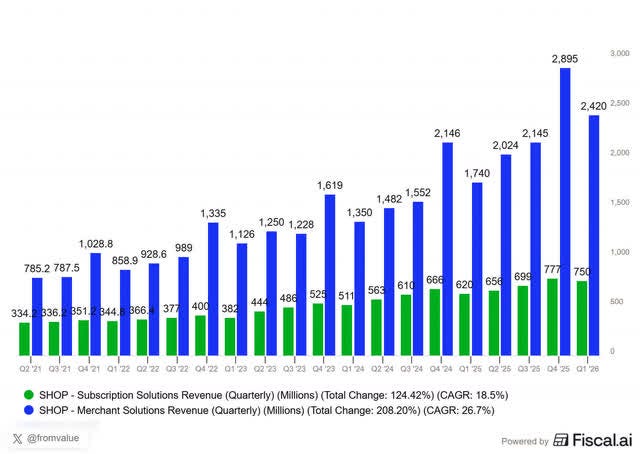

Revenue Breakdown

Merchant Solutions Revenue continues to drive the majority of revenue, growing 39% year-over-year to $2.42B. This was largely driven by a 41% increase in Gross Merchandise Volume (GMV) processed through Shopify Payments.

Subscription Solutions Revenue: Grew 21% year-over-year to $750M. This was fueled by more merchants joining the platform and a higher mix of merchants opting for the high-value Shopify Plus plans.

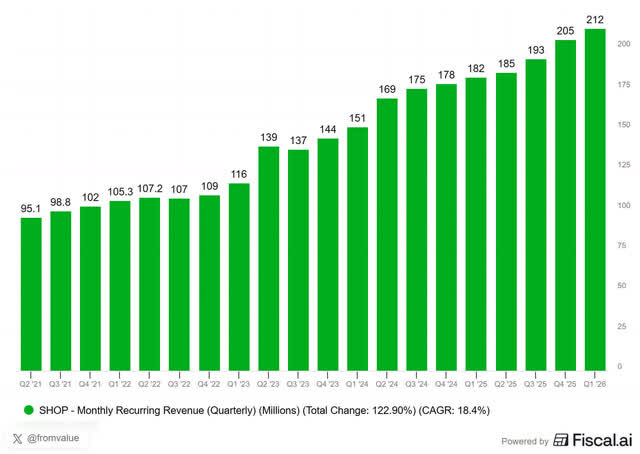

Monthly Recurring Revenue (MRR): Reached $212M, a 16% YoY increase. While the growth rate is a step down from the 20%+ growth seen last year due to pricing hikes, the absolute dollar growth remains a solid directional indicator for future subscription health, and it actually had a slightly higher growth rate than last quarter.

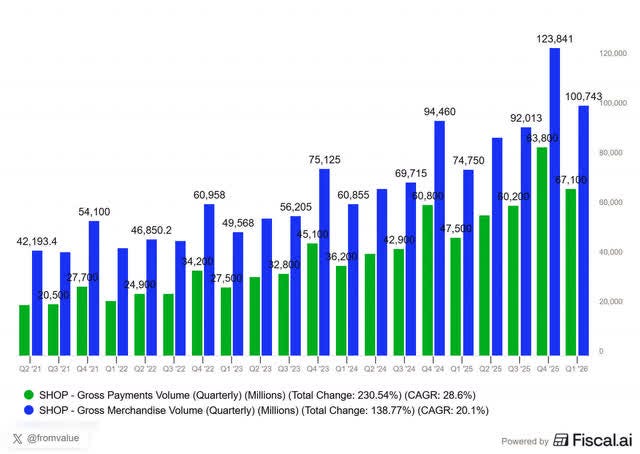

Volume Metrics

Gross Merchandise Volume (GMV): For the first time ever, Shopify cleared $100B in the first quarter, hitting $100.7B (up 35% YoY).

Gross Payments Volume (GPV): Payments through Shopify’s own rails reached $67B, representing a 67% penetration rate of total GMV. Adoption remains high, even as the platform scales into more diverse geographies and larger enterprise brands.

Attach Rate (aka Take Rate) is another helpful indicator that tells us how much revenue Shopify is extracting from the growth in GMV. Kris has used it for a long time in the Selling Rules. It came in at 3.15%, almost matching the highest level set a few quarters back.

with a total change of 2.27% and a compound annual growth rate (CAGR) of 0.8% over a specified period. AI-generated content may be incorrect.")

As merchants sell more, Shopify is benefiting more as that piece of the pie increases.

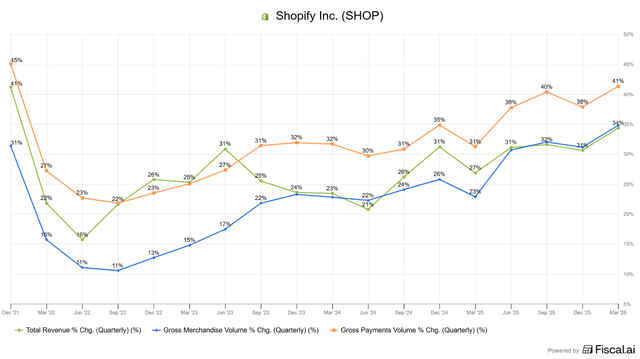

Let’s step back for a second here and look at the topline metrics’ growth over the past few years:

After a growth slowdown a few years ago with the COVID backlash, Shopify is clearly showing reacceleration across the board. Selling more products (GMV), processing more payments (GMV), all while growing revenue at an impressive rate. Very strong!

But are they just buying their growth or are they doing it profitably? Let’s take a look.

Gross Profit: Increased 32% YoY to $1.55B.

Gross Margin: Held steady at 48.8%.

Some may be fooled by the growth of payment solutions, which carry a lower gross profit margin (~40%) compared with subscription solutions (~80%), and assume the margin is being held down by a less efficient part of the business. However, payments are asset-light and scale effortlessly due to lower operational costs once the initial “cost of goods” is covered. We can see the efficiency reflected in the next point.

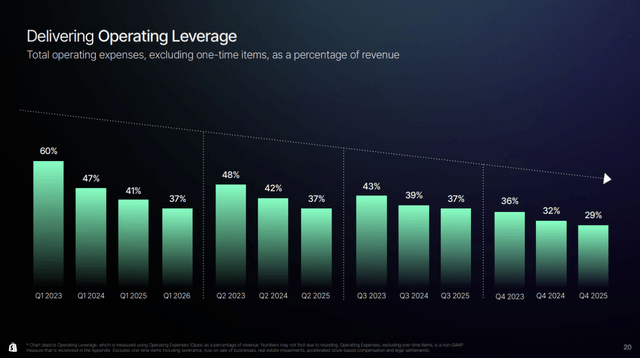

Operating Income: came in at $382M, a 88% increase over Q1 2025 and operating leverage continues to improve every quarter as we can see by this illustration below:

Source: Shopify

Net Loss was -$581M for the quarter.

Earnings per Share was -$0.45 compared with -$0.53 last year.

Both bottom-line numbers are not relevant due to equity investments and miscellaneous other items, which make them pretty meaningless in gauging business performance. To remind you, Shopify has investments in Affirm, Global-e and Klaviyo. The Affirm investment went down from $1.5B to $930, the Global-e investment from $868M to $682M. Shopify has not sold these, so the losses are unrealized but under accounting rules, this is a loss. In total, there was a “loss” of more than $1B in investments. Net income excluding equity investments came in at $360M, up 59% YoY.

Free Cash Flow: Came in at $476M, representing 31% year-over-year growth with a 15% margin. This matches last year’s margin but represents significantly higher absolute cash generation.

President Harley Finkelstein summarized Shopify’s strong streak:

That means we’ve now put up four straight quarters of 30% or more revenue and GMV growth alongside mid to high teens free cash flow margins every single quarter. There are very few publicly traded companies today that are able to make that claim at anything like this scale. It is a very small club, and that is something we are very proud of.

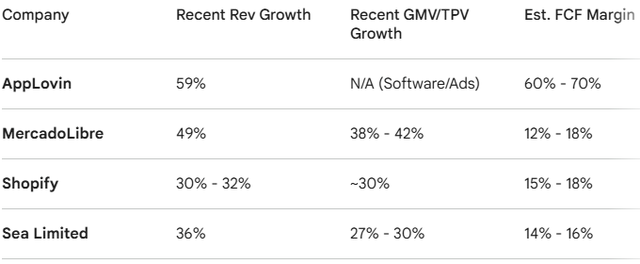

Out of curiosity, I went ahead and input that exact parameter into an LLM and received this response:

Source: Google Gemini

As a disclaimer, I did not fact-check, but I found it interesting that 3 of the 4 are Potential Multibaggers (I personally own all 4).

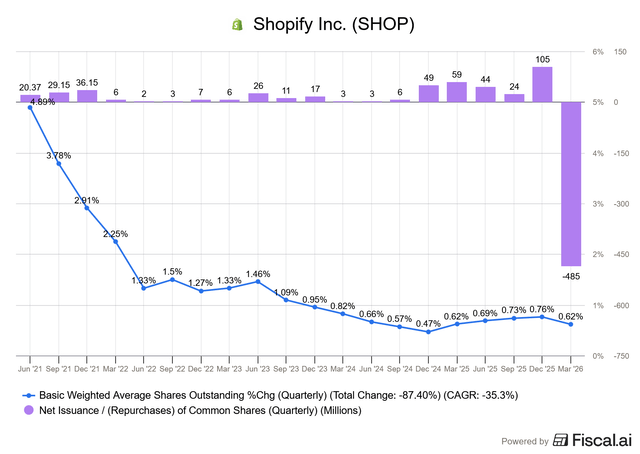

During Q1, Shopify also repurchased $514M of its own shares, with $1.5B still remaining in the authorized program. This is the first quarter of significant buybacks:

With a fortress balance sheet of over $5.7B in cash and marketable securities and no debt, Shopify is returning capital to shareholders while maintaining aggressive growth.

Q2 2026 guidance

Management expects Revenue growth in the “high-twenties” on a year-over-year basis, a noticeable step down from the 35% revenue growth in this quarter. Jeff Hoffmeister states some of this deceleration has to do with the reduction in favorable FX tailwinds next quarter.

Business Highlights

Do I even need to say it? Of course, the conversation was dominated by AI. As Harley Finkelstein noted:

In 2026, AI is now Shopify’s native language. We bet early on AI and forced its adoption. It’s embedded in everything we do, the products we build, the channels we power, the way every single person on the team operates.

I mentioned in the Q4 2025 earnings article that Shopify is the e-commerce platform best positioned for the AI wave, and the metrics are confirming exactly that which Finkelstein highlighted:

In the first quarter, AI-driven traffic to Shopify stores has grown 8x year-over-year, while orders from AI-powered searches have increased nearly 13x. Within this, new buyer orders are occurring at nearly twice the rate of other channels.

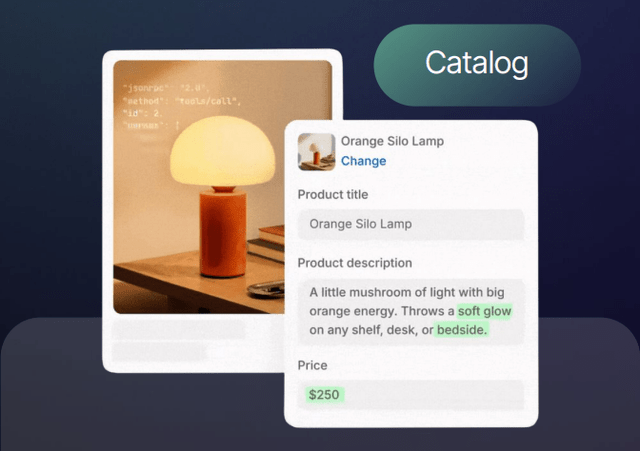

Some of that success can be attributed to Shopify Catalog, which structures and standardizes merchants’ products, making them more readable and understandable by AI Models in real time.

This structured data has provided a noticeable performance edge with traffic originating from Catalog-powered AI searches converting 2x better than traffic from general AI searches, and orders from AI search have grown 15x since early 2025 (keeping in mind this is growing from a small base).

Source: Shopify

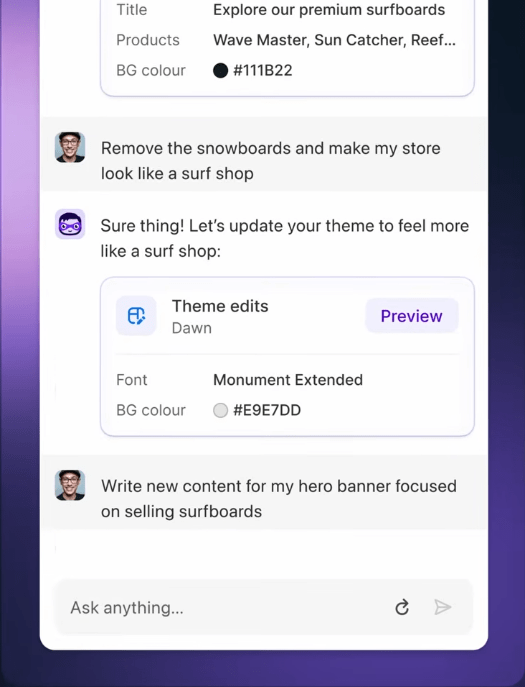

AI is also leveraged to help merchants. Sidekick is Shopify’s AI-powered “co-founder” designed to assist with a wide range of operational tasks via a conversation interface. During the call, management reported monthly active usage of 4x year-over-year. Nearly half of the Shopify Flows (automated workflows) in Q1 were built through Sidekick and theme edits through the tool grew by 1,000% during the same period.

Source: YouTube

Beyond conversion, Shopify is developing tools for demand generation, specifically to help small businesses that lack the resources to manage massive multi-platform campaigns.

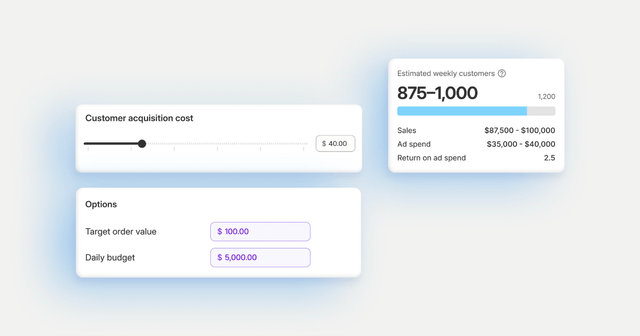

Shop Campaigns provides merchants with a more turnkey solution to acquire new customers. With Campaigns, merchants only have to enter a few parameters, and the tool will do the rest, enabling merchants to advertise their products across multiple surfaces: Shop App, Shop Product Network, and other popular ad platforms (Facebook, Google, Instagram, etc.).)

Source: Shopify

In Q1, the number of merchants with a live campaign was up 3x year-over-year and for some of the merchants, Shop Campaigns is contributing as much as a quarter of their total GMV.

Shop App GMV rose 70% year-over-year, showcasing its growth as a destination for online commerce. The engagement metrics further highlight this momentum, with monthly active users growing more than 40%, and unique buyers increasing over 50% compared with the same period last year. These results show an increasing number of shoppers are now discovering and buying from brands directly within the Shop ecosystem rather than just navigating to sites from external sources.

The continual rate of product innovation and improvement demonstrates that Shopify continues to do everything possible to help its clients win, because when they win, Shopify wins.

Here’s where the free part ends. If you want to know if Shopify is a BUY now, and you want the Best Buys Now stocks of tomorrow and sooo much more, consider upgrading your subscription to paid.