Hi Multis

Mercado Libre (MELI) reported its Q4 2025 earnings at the ned of February. The company announced more investments and that made the stock drop like a bomb. It is now down more than 35% from its top.

So, let’s look at the numbers first.

The Numbers

Revenue: $8.76B (+44.6% YoY), beating estimates by $300M

EPS: $11.03, missing estimates by $0.41

Operating margin: 10.1% (down from 13.5% a year ago)

Full year revenue growth: 39%

Full year income from operations growth: 22%

Marketplace:

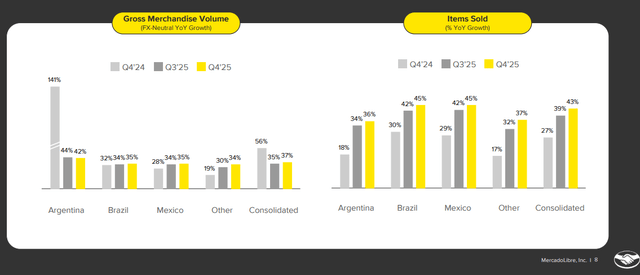

GMV: $20B (+37% YoY FX-neutral in Brazil, +35% in Mexico)

Items sold growth: 45% YoY in Brazil (accelerating from 42% in Q3 and 26% in Q2)

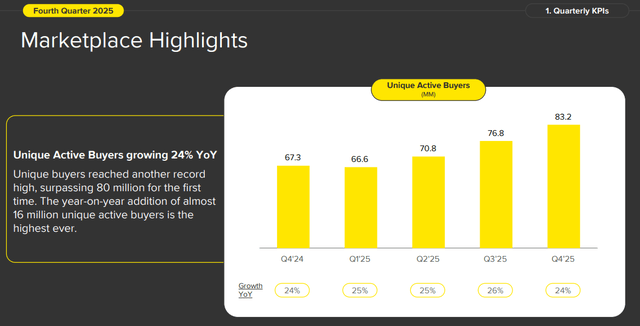

Unique active buyers: 83.2M (+24% YoY)

Mercado Pago:

Monthly active users: 77.9M (~28% YoY)

Credit portfolio: $12.5B (+90% YoY)

Assets under management: $19B (+78% YoY)

Nearly 3 million new credit cards were issued in Q4 alone

Regional Breakdown:

Brazil: 54% of revenue

Mexico: 22% of revenue

Argentina: 18% of revenue

Other: 4% of revenue

Advertising:

Revenue grew 67% YoY (FX-neutral)

And here’s an overview from Mercado Libre’s earnings call slides:

Investing For Dominance

Let me repeat something I’ve said in my previous MELI articles. Every single time Mercado Libre has deliberately compressed margins to invest in the long-term opportunity, it has paid off. Every. Single. Time.

And each time, analysts doubted the company. Same story, over and over again. Sometimes, the markets are funny in their own way. Management was very transparent about the investments, which I always like.

In the shareholder letter, management quantified the margin impact of the investments (note: CBT = cross-border trade, 1P= 1st-party selling, where MELI is the merchant)

We estimate the combined impact of our strategic investments, which include the lower free shipping threshold in Brazil, CBT, 1P and the credit card, was equivalent to 5-6 percentage points of operating margin in Q4’25.

So, without the deliberate investments MELI made, the operating margin would have been around 15-16%. That’s strong, and it would have probably meant a beat on earnings, too.

CFO Martin de Los Santos added on the conference call that the company won’t hesitate to keep investing:

Our main focus is on capturing the large opportunities in front of us in commerce, fintech and advertising. And we will not hesitate to invest in order to capture those opportunities as we have done in the past, even if that puts some short-term margin pressure. We’re not trying to optimize short-term margin.

Now, if you’re a trader, you hate hearing this but as a long-term investor, this is music to my ears. And importantly, these aren’t vague promises. The results are already visible. Even with all these investments, full-year income from operations still grew 22%. The company makes the right choice to grow faster at the expense of higher short-term margins.

So, yes, analyst calls like this one are correct but myopic, only looking at the year ahead.

Source: Seeking Alpha

That was the reason Mercado Libre dropped more after earnings. Thank you to all traders and short-term focused analysts.

Commerce: Brazil Is On Fire

The free shipping initiative in Brazil that we discussed extensively last quarter continues to deliver beyond expectations. As a reminder, Mercado Libre lowered the free shipping threshold (from R$79 to R$19), and the results are remarkable.

Items sold in Brazil accelerated from 26% year-over-year in Q2, to 42% in Q3, to 45% in Q4. Overall, it was 43.2% (the number disappears for one reason or another when I download the chart).

Do you want such premium insights? Fiscal has you covered! Grab a 15% discount with this link.

The unique active buyers grew by 24% YoY, the highest number of new buyers ever.

New CEO Ariel Szarfsztejn was proud:

New buyers that have come to MercadoLibre since June when we launched the new value prop are buying more items across a larger number of categories with higher retention rates compared to cohorts of new buyers prior to that change.

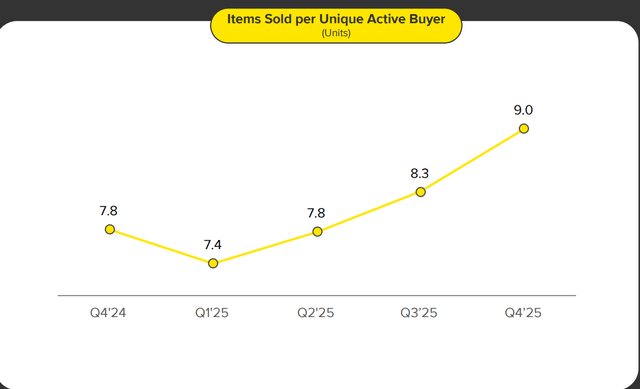

You can see this here.

It’s very impressive to see this. Usually, when an e-commerce business grows quickly, the average number of items sold per user drops. That MELI can make both grow so strong is another testament to the strength of this company.

I think this is a point many miss. So, anyone saying that the margin compression is important is not looking at Mercado Libre as an investment but as a trade. As an investor, you think like a business owner, and as a business owner, I’d be delighted with these results.

The logistics network is absorbing all of this beautifully. Unit shipping costs in Brazil declined 11% during the quarter. More volume is a leverage, as fixed costs go down as a percentage of delivery costs.

Mercado Libre introduced a slow-ship network to fill idle capacity, which I like a lot. When you have trucks and warehouses not in use at any given time, you can ship lower-value items during periods of lower traffic at almost no incremental cost. It’s a brilliant solution and it’s one of the things that competitors without such a big delivery system simply cannot copy, unless they invest heavily for years. Mercado Libre has already done those investments.

Mexico is performing well too, with 35% GMV growth. Cross-border trade saw a 74% increase in FX-neutral GMV. Mercado Libre now operates fulfillment centers in both the U.S. and China to serve its Latin American customers. This is a direct copy of what Amazon does worldwide. Here’s the regional breakdown.

An update on first-party (’1P’) that flew a bit under the radar. 1P is when Mercado Libre is the seller. Amazon started mostly with 1P and then expanded to 3P. Mercado Libre did it the other way around.

CFO Martin de Los Santos confirmed that 1P is now profitable before allocating central and indirect costs. That means it’s still not fuly profitable, but it’s early and this is a meaningful milestone. Scale will do the rest.

Remember, 1P exists as a sort of customer service to fill gaps in selection and pricing where third-party sellers underperform. It grew by about 80% FX-neutral in 2025 and is clearly gaining traction, especially in categories such as supermarkets. It’s an addition to the core 3P model, definitely not a replacement and it’s a good thing to see that there is a path to profitability.

Mercado Libre also changed its shipping fee structure for merchants in Brazil in January, moving to a model that charges based on actual dimensions and weight rather than flat rates. It’s still too early to tell what the financial impact will be, but it shows the company continues to fine-tune its business consistently.

This is just about a third of this article. Do you want to know whether I see MELI as a great opportunity now or not?

Do you want the whole article and know what I bought with my own money earlier this week?

Go to this page.

Subscribe to the annual plan.