Hi Multis

Kinsale (KNSL) reported its Q1 2026 results quite some weeks ago, but I had not covered them yet. Since the earnings, the stock is down about 13%.

If you zoom out a bit more, you see that Kinsale has the worst drop since it became a public company in July 2016. The stock is down almost 45%.

Last quarter, when premium growth slowed to 1.8%, I made the case that the slowdown was intentional and good. Kinsale was leaving underpriced business, to the competition.

So which is it this time? Is this a disciplined company riding out a soft market, or has the growth story simply ended? That’s an important question, as it means more or less the same as: Is the investment thesis still intact?

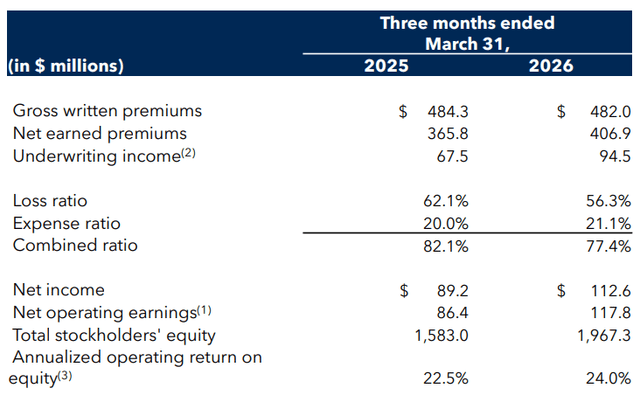

The Numbers

Gross Written Premiums: $482.0 million, down 0.5%. Yes, down. As far as I know, it’s the first decline. This is probably the main reason Kinsale’s stock dropped. Let’s part it for now, but obviously, we’ll get back to this.

Net Written Premiums: up 5.6%. Gross down, net up. We get back to that later as well, of course.

Net Earned Premiums: $406.9 million, up 11.2%. Earned premium is the part of written premium that gets “used up” as a policy runs off, and it is the part that shows up as revenue. It lags written premium.

Underwriting Income: $94.5 million, up 40%.

Combined Ratio: 77.4%, down from 82.1% a year ago. The combined ratio is the loss ratio (claims paid out) plus the expense ratio (the cost of running the business). Under 100% is an underwriting profit. So 77.4% means Kinsale kept about $22.60 of every $100 in premium as pure underwriting profit. That’s before a single cent of investment income. This remains very impressive.

Net Income: $112.6 million, or $4.88 per share, up 26.1%.

Net Operating Earnings: $117.8 million, or $5.11 per share, up 37.7%. Operating earnings leaves out the ups and downs of the stock portfolio, so it shows the insurance business more cleanly.

Operating Return on Equity: 24%. The average US insurer sits somewhere in the low teens, so this is still outstanding.

Book Value Per Share: $85.31, up 25.6% in a year. Great result.

Net Investment Income: $55.4 million, up 26.5%.

Float: now $3.3 billion.

Here’s an overview from the earnings slide deck.

So: EPS up almost 38%, a 24% ROE, book value growing at 25%, a combined ratio under 78%. Read these numbers and you wonder why the stock is anywhere near its lows. The top line growth and the quality of the earnings are the reason.

Below, for paid subs: why the biggest division is shrinking on purpose, the new competitors that worry me more than the giants, and what I'm doing with my position on Monday.

4000 words you can’t read as a free sub.