Hi Multis

Last week, Kinsale (KNSL) reported its Q4 2025 earnings.

The stock dropped as much as 15% but that loss is now reduced to 7.7%. Still quite a bit for a stock that hasn’t done great overall.

So, why did the stock drop? Gross written premiums grew only 1.8%. That scared people. But I’ll explain why that number is probably one of the strengths of this company.

First, the results.

The Numbers

Revenue: $483.27 million, up 17.3% year-over-year, beating estimates by $15.89 million.

Net Income: $138.6 million ($5.81 per share), up 27% year-over-year from $109.1 million. That’s a beat of $0.50 on the consensus estimate. For the full year, Kinsale posted record net income of $503.6 million, up 21%. You don’t need me to tell you those are phenomenal numbers, but I will tell you anyway.

Operating ROE: 26% for the full year. Best in class, as usual. For context, the average US insurer operates somewhere in the low teens or even single digits. Kinsale continues to impress here.

Book Value Per Share: Grew 33% to $84.66. Awesome result!

Float: Grew 23% to $3.1 billion. This is the money Kinsale holds between collecting premiums and paying claims. Think of it as an interest-free loan from policyholders. If your float is bigger, you can grow investment income faster. Warren Buffett built an empire on this concept at Berkshire, and Kinsale is running the same playbook, albeit at a much smaller scale and more conservatively than Buffett (more bonds and such).

Gross Written Premiums: Up just 1.8%. Ouch. Right? Uhm, right? Let’s zoom in here.

One Division Is Distorting Everything

Kinsale has about 25 underwriting divisions. One of them, Commercial Property, which handles large, catastrophe-exposed commercial property, declined 28.3% in the quarter. For the full year, it was down 17.9%.

If you exclude that division, gross written premiums grew 10.2% in Q4 and 13.3% for the full year. But Commercial Property is the largest division by premium collected.

Commercial Property is the largest division by premium collected.

Why did Commercial Property drop 28.3%? It had an extraordinary run and grew roughly 20x over the prior five years. During that period, many insurers ran from catastrophe-prone risks, and Kinsale stepped into the void, charging crisis-level premiums. Those days are over now. Competitors have noticed the margins and are coming back in. Those extremely high premiums are gone.

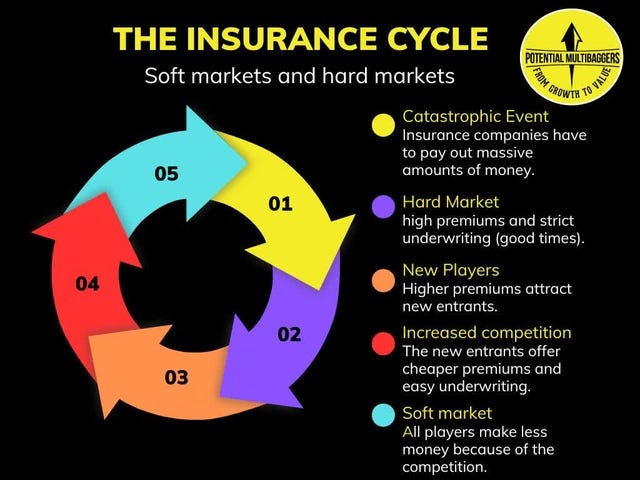

I have shared the insurance cycle before.

Right now, we are in a soft market because of the increased competition. This will last until a major catastrophe happens and then some undercapitalized competitors will either withdraw from that market or go out of business, which will be the reason why there will be a hard market again, which is good for strong companies like Kinsale.

Stuart Winston, the Chief Underwriting Officer, said that in September and October, it looked like Commercial Property was stabilizing. Then, in November and December, a fresh influx of competition brought premiums down further.

Is this a problem? Yes and no. Yes, because it’s Kinsale’s largest division and the premium contraction is pulling down growth. No, because this is exactly how insurance cycles work. And more importantly, Kinsale is not chasing this business at bad prices. CEO Michael Kehoe was clear. Kinsale manages every product line to a low 20s ROE or greater, and it’s not going to compromise to make the growth look better. Its discipline is its moat, and therefore, it’s good to see the company doesn’t suddenly change course.

The companies that now chase revenue growth at all costs in this competitive pricing environment are the ones that will end up with ugly surprises in two or three years.

Kehoe expects the division to stabilize “after the next couple of quarters,” but the competitive environment in large property will continue into 2026. The company’s other property divisions all grew at double digits. Think of divisions like small business property, high-value homeowners, inland marine, personal insurance, agribusiness property, and so on.

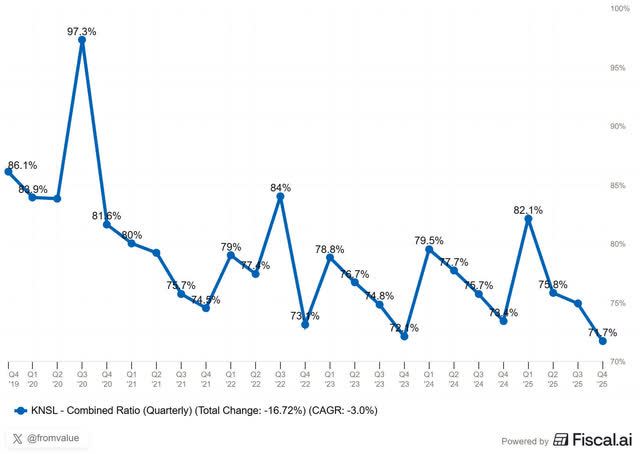

The Real Story: 71.7%

There’s something else that really popped out but on the positive side. The combined ratio of 71.7% is the best Kinsale has ever posted since going public. To quickly recap for newer readers: the combined ratio adds up an insurer’s loss ratio (how much it pays out in claims) and expense ratio (how much it costs to run the business). Below 100% means profit. The lower, the better.

71.7% means that for every $100 in premiums, Kinsale kept about $28.3 as underwriting profit. That’s before a single dollar of investment income. That’s an almost absurd level of profitability for the insurance industry.

I have already shared this earlier, but I want to show you how exceptional this is. This table was shown at the Markel Brunch in Omaha in May 2025. See how much better Kinsale already does here, with 78.7%. Now it was, and I want to repeat this, 71.7%. That’s just mind-blowing.

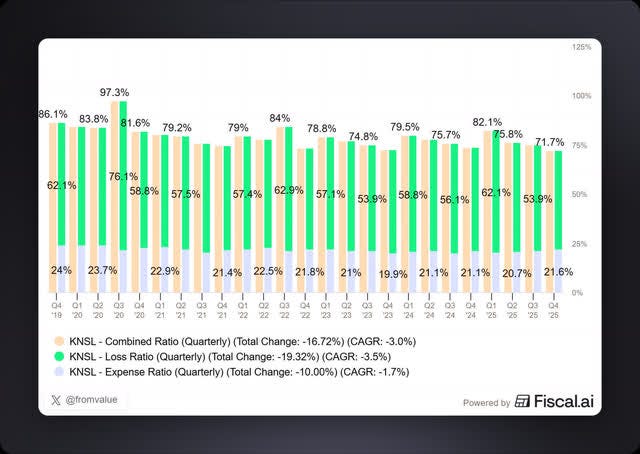

This is how that 71.7% combined ratio looks like.

You can see that there’s a 50.1% loss ratio and a 21.6% expense ratio.

The loss ratio improved by 220 basis points YoY. There were simply fewer catastrophes to pay.

4 basis points come from favorable prior year reserve development, up from 2.6 points last year. Now, what does that mean?

When an insurer sets aside reserves for future claims, it’s making an educated guess. If the actual claims turn out to be lower than the reserves, the difference flows back as profit.

Kinsale has overestimated its claims every single year since its founding. That tells you two things: the company’s genuinely conservative in its reserving, and it’s good at what it does.

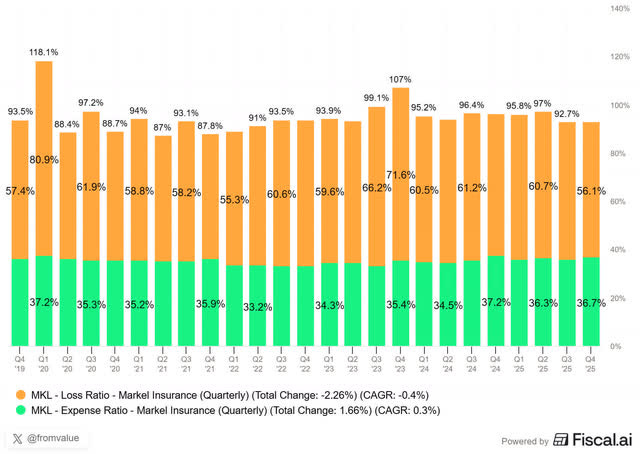

If you look at the expense ratio, you see the company in full strength. At 20.8% for the full year, Kinsale spends about 15 percentage points less than its competitors, who operate in the mid-30s or above 40%. Just look at Markel, for example, a highly-regarded quality company.

Kinsale’s operational efficiency piece of the expense ratio (stripping out commissions) was 10.5% for the year, half a point better than 2024. So, Kinsale even gets more efficient.

Kehoe said something on the call that I think perfectly shows Kinsale’s strength:

Kinsale last year had an expense ratio under 21%, and many of our competitors tend to run in the mid-30s or higher, some even above 40%. Given the customers’ focus on low cost, it’s hard to overstate the significance and the durability of this advantage.

Because the expense ratio is about 10 or 15 full points lower than its competitors, Kinsale keeps stacking advantages. Customers care mostly about price and Kinsale has a natural advantage there because of the low expense ratio. It means Kinsale can offer lower prices than the competition and still make significantly more money. Or it can match the competition’s pricing and make a much bigger profit than the competition.

In a soft market, this advantage becomes even more powerful, because competitors with 35%+ expense ratios start getting squeezed while Kinsale is still comfortably profitable. Even more profitable than ever, as the lowest combined ratio in years proves.

The Float Machine

Net investment income grew 24.9% in Q4 to $52.3 million. New money yields are averaging around 5%, with a 4-year average duration for the fixed-income portfolio. The gross return on the investment portfolio was 4.4% for the year, consistent with 2024.

This is the part of insurance that Buffett has been talking about for decades. Kinsale’s float is now $3.1 billion. The float keeps growing and growing, and that means Kinsale has more and more revenue (and net income) that can be used to invest.

Investment income is therefore increasingly a meaningful contributor. This quarter, $52.3 million in investment income on a base of $120.6 million in underwriting income adds almost 43% to that base. And unlike underwriting income, which fluctuates with catastrophes and pricing cycles, investment income is much more stable and predictable and flows directly to the bottom line.

With premium growth moderating for now, Kinsale gives capital back to shareholders. In December, the board authorized a $250 million share buyback program. In Q4, the company bought back $50 million of stock, using the last money of the previous $100 million authorization. And Kinsale also raised the quarterly dividend by 47% to $0.25 per share. Kehoe also said it’s likely the company will deploy the $250 million authorization over the next year or so.

Kinsale’s AI

For Kinsale, AI is genuinely relevant because its entire competitive advantage is built on technological efficiency.

Over a year ago, Kinsale launched a company-wide AI initiative. Every employee now has an enterprise AI license and they have built dozens of bots and agents used daily in their business processes. Not entirely surprisingly, Kehoe pointed to IT and analytics as the areas where AI is delivering the most today. AI writes and tests code, converts unstructured data into structured data, and improves risk segmentation and pricing.

Kinsale processed about 1 million submissions last year. They quote more than 70% of all new business submissions, much more than most competitors. When you’re handling that volume, even small automation gains compound. And remember, 27% of Kinsale’s employees work in the technology department. It’s Kinsale’s differentiator and the reason I picked the company as a Potential Multibagger. The company owns its own modern custom-built core operating system, with no legacy software. Kinsale’s competitors use systems built 20, 30 or 40 years ago.

Kehoe summarized the AI opportunity in two buckets. One is even more automation, which lowers the expense ratio even further. The other is even better at segmenting and pricing risk, which further improves the loss ratio. So, it’s not a coincidence that the combined ratio dropped. Kehou called the gains “material,” even at this early stage. In other words, Kinsale’s technological advantage only expands.

Submission Trends and Pricing

New business submission growth was up 6% for the quarter (excluding unsolicited submissions). Without Commercial Property, new business submission growth was 9%. About half of Kinsale’s divisions are seeing double-digit submission growth. Renewal retention sits in the low 70% range, steady, with no growth in business moving away from the E&S market.

The combined pricing trend, per the Amwins Index (a large wholesale broker that sees massive volumes of E&S transactions), showed a rate decrease of 2.7% in Q4, compared to just 0.4% in Q3. So the pricing environment softened, again pointing out the soft market.

Within the whole, the several lines vary significantly. Large commercial property is under heavy pressure, but commercial auto, excess casualty, and general casualty still see meaningful rate increases.

Kehoe pointed out something I think many analysts missed:

The 13% growth overall ex-commercial property is pretty strong. If you look at how all the public brokers reported, growth rates tend to be kind of low to mid-single digits.

He’s right. In this competitive environment, 13% growth in the overall premiums with a 71.7% combined ratio shows how strong Kinsale is.

The Call

Unless you get to listen to The Trade Desk’s Jeff Green or Cloudflare’s Matthew Prince, the Q&A section is almost always the best part of the conference call, and this one was no exception.

About 80% of the analyst questions boiled down to: “Isn’t competition going to eat your lunch?” Analysts asked about commercial property declines, casualty pricing trends, submission flows, standard carriers moving into the E&S space, and whether the growth headwinds would persist.

There’s a clear pattern you can see if you have followed so many Kinsale calls as I have. Analysts obsess over pricing cycles and competitive threats, while management keeps calmly pointing to the same things: we have lower costs, we underwrite with discipline, and we reserve conservatively.

The analysts seem to want a more complicated answer, some sort of magic formula no one else sees. But sometimes the business really is that simple and a few fundamental differences make a huge difference in results.

An analyst from Bank of America asked whether social inflation and increased litigation were migrating into the small-account space where Kinsale operates.

Kehoe, in his typically understated tone:

Small accounts definitely aren’t immune from that.

He acknowledged that the U.S. litigation industry is “large and growing” and that plaintiff attorneys are “entrepreneurial as hell.” CFO Petrucelli’s addition, “We’re vigilant for sure,” was another classic Kinsale understatement. This is a management team that doesn’t hype and doesn’t panic. They take on problems the way they run their business: calmly but without hesitation.

A good question came on how Kinsale exercises its expense advantage: does it write at lower ROEs to grab market share, or does it keep printing 26% ROEs?

Kehoe’s answer was clear (and no suprise for me): Kinsale always targets a low 20s ROE or better on each product line, and the assumptions lean conservative. Historically, Kinsale has outperformed its own targets. Kinsale’s not going to sacrifice margin for volume. To me, that’s the only right choice. If you erode on quality, you know where you start, but not where you end.

So, you can say that the slowdown is actually demonstrating Kinsale’s moat. It won’t compromise on quality. I think you and I know that analysts would have been much more excited if premiums had grown much faster, but as a long-term investor, I couldn’t be happier with Kinsale’s decision to prioritize quality over dumb growth. And that comes from a growth investor, haha.

There were also questions about growth areas. Homeowners insurance is a long-term project. Kinsale is already in about 4-5 states for high-value homes and 15 states for manufactured homes. The expansion is slow on purpose. Kinsale looks where the opportunities are. Major insurers like State Farm and Allstate have retreated from catastrophe-prone states and therefore, insurance there is moving from standard to nonstandard (E&S) markets. Kinsale is filling the gap, but very carefully, which is in its nature.

On the question of whether AI could disrupt the broker model, Kehoe quoted Pat Ryan (founder of Aon and Ryan Specialty): “The customer needs an adviser and an advocate. I don’t think that changes with AI.”

But of course, we already saw earlier that Kinsale benefits from AI.

Conclusion

I couldn’t be happier with the earnings. I understand the initial drop, for sure. 1.8% gross premiums growth looks subpar. But insurances are a cyclical business in that respect. It’s only when the times are tougher that the diamonds shine. What I mean is that Kinsale can be above the street fighting competitors, nipping a good glass of quality wine from a distance, as it were. They know the street fighters will eventually harm each other enough to be both out of the game and then Kinsale can come in again, unharmed and still going for that high quality. At that moment, growth will return and all analysts will be fanboys again.

Kehoe has been running this company for 17 years with the same philosophy: build for cycles, not quarters and aim for a low 20s ROE or better. Reserve conservatively and let the expense advantage compound year after year. Simple but not easy under shareholder and analyst pressure. But Kehoe has been there, done that, bought the t-shirt, so to speak.

The competition has intensified but printing a 71.7% combined ratio in the most competitive quarter of the most competitive year in recent memory is the best proof that Kinsale deserves a place in my portfolio.

As Kehoe put it at the end of the call:

I think our investors should expect us to generate very high and attractive returns for the foreseeable future.

After seventeen years of backing that up with results, I see no reason to have any doubt about these words.

If you are not on the paid plan yet, this is your chance. (If you are a premium member already, just scroll past this message). What do you get as a Premium member?

✍️ Multiple high-quality articles per week

📚 Full access to our entire library of deep-insight articles

🔎 Full investment cases

📊 Access to the Private Community

🎥 Regular Webinars

📈 The Best Buys Now every month

✍️ The Overview Of The Week each Sunday

🔎 Deep earnings analysis

Many Multis say that the community alone is already worth the price, but you get so much more.

Go to this page.

Subscribe to the annual plan.