How attractive is Mercado Libre Now?

About a proverbial boiling frog and valuation

Hi Multis

In the article I wrote earlier last week, I analyzed Mercado Libre's (MELI) earnings. However, the earnings don't tell us whether the stock is a buy or not; they just tell us whether the investment case is still on track.

One of the dangers in investing is what's sometimes referred to as the "boiling frog" effect.

The metaphor is simple: if a frog is dropped into boiling water, it jumps out immediately. But if the water is heated gradually, the frog doesn’t notice the increasing danger and stays put until it’s too late and he's cooked. Just for people caring about frogs: it's a metaphor. In reality, the frog would leap out.

In investing, this metaphor is used when quality slowly erodes over time. The changes might be subtle per quarter: a slight drop in margins, a slowdown in revenue growth, more stock-based compensation, etc. Separately, these signs might not seem alarming, but together, they can signal a fundamental shift in the company’s trajectory.

That's why I developed the PMQS, the Potential Multibaggers Quality Score, to keep checking constantly if the quality of the businesses we partly own are not slowly deteriorating without us noticing it.

But even if the quality is super high, sometimes it's better not to buy a stock because of the valuation. That's where the QPI, the quality-price score, comes in. This score weighs the quality and the valuation because we all know that higher quality often warrants a higher price and vice versa.

So, without further ado, let's look at the PMQS & the QPI for Mercado Libre.

Personal conviction 10/10

Since January 2024

This is mainly my or your own conviction based on everything I/you know about the company. Your own conviction may be very different here and you can adapt this score to your own liking.

You can download the sheet here to give your own score. You can do this alongside me.

In January this year, I finally caved and gave Mercado Libre a 10/10 personal conviction score. This was not a rash decision because of the market it operates in. Latin America is less stable. But Mercado Libre has proven for 25 years now that it can navigate difficult economic situations. And its 35% revenue growth in US dollars (103% FX-neutral) in Q3 again shows that the company keeps operating in beast mode.

Profitability 10/10

Since January 2024

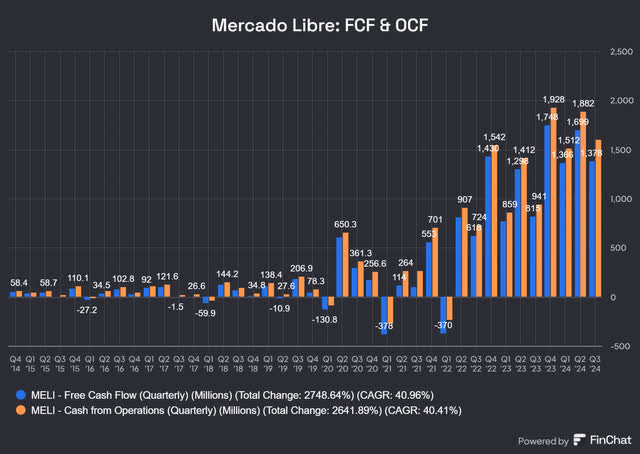

I always look at Free Cash Flow and Operational Cash Flow (=cash from operations) first. Both have trended up, impressively up Mercado Libre. And mind you, Mercado Libre has always invested in fulfillment. That makes it even more impressive.

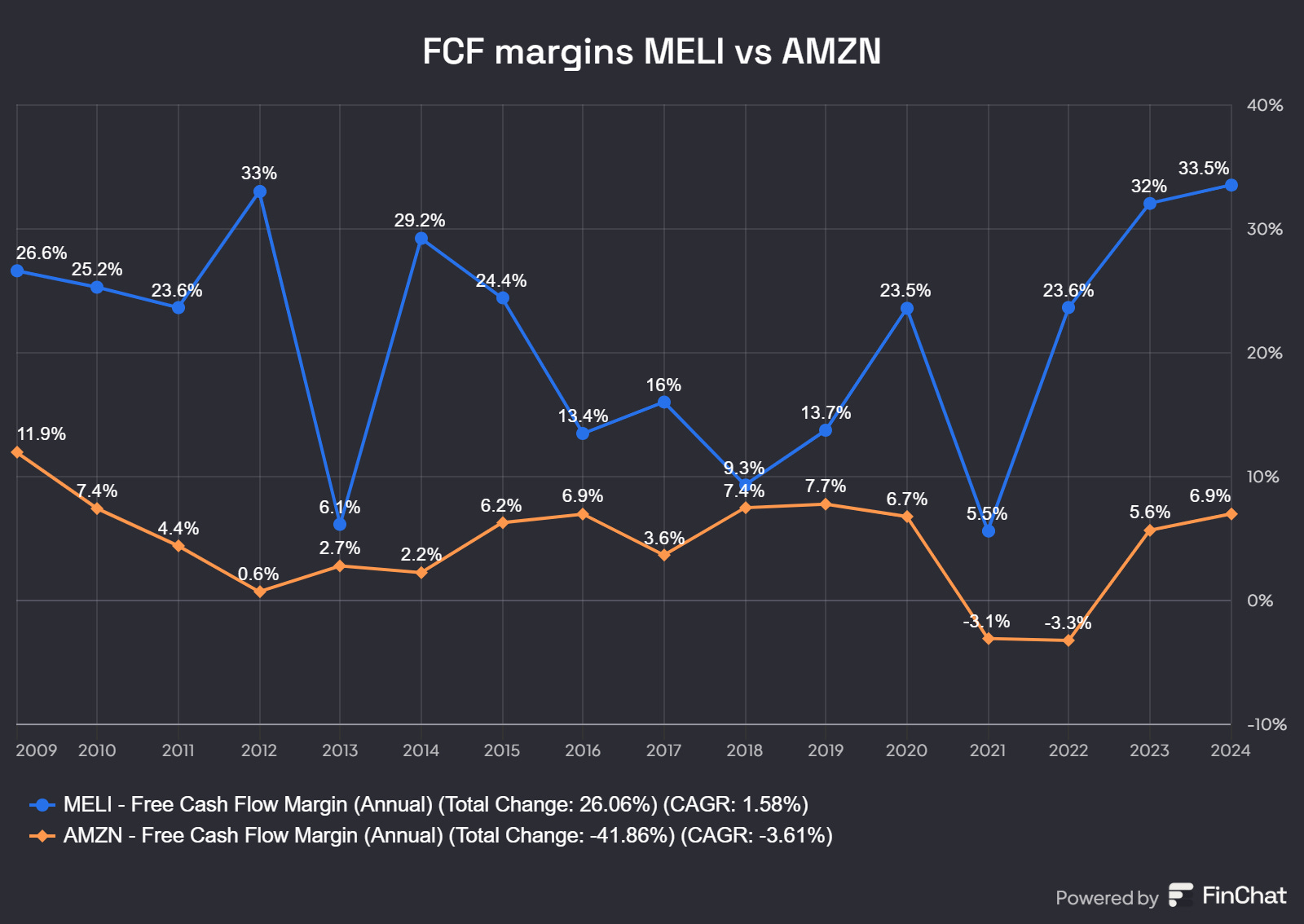

If you want to know how impressive this is, this is Amazon (AMZN) versus Mercado Libre.

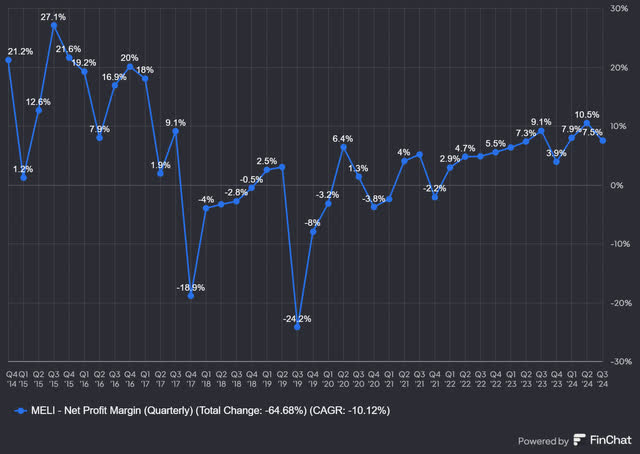

And the company is also substantially profitable on a net income margin.

In Q3 2024, net income on a GAAP basis was 7.5%, which is really strong for a company that grew its revenue by 35% in that quarter. There was a one-time tax hit in the Q4 2023 quarter. The company is back to strong profitability now.

Mercado Libre has been flexing its profitability muscle over the last years. And I reward it with a perfect score. 10/10.

Sales efficiency 10/10

Unchanged since September 2022

The sales efficiency score first looks at the marketing efficiency by looking at what percentage of revenue goes to SG&A (selling, general and administrative) and how much revenue growth that brings in the trailing twelve months and what is expected next year. I divide the average of those two by the SG&A number as a % of revenue and that is marketing efficiency. I then multiply that by the gross margin to look at sales efficiency. I then divide that number by 10 to get the Sales Efficiency Score.

This is the score for Mercado Libre with the Q3 2024 results.

Of course, this formula is far from perfect, but it gives you some idea of how well the company sells its product. There are plenty of nuances to add here, but the numbers are what they are.

Mercado Libre has had a 10/10 score since the beginning I started using the Quality Score. This quarter, it had a score of 127.2, clearly above the threshold for a perfect score, again.

Innovation 5/5

Since January 2024

This is part subjective, part measurable. Subjective as in: how many new important products does the company issue versus its competitors? You can partly measure that, too, if you want, but the magnitude of the innovations is much more important than the sheer number of innovations.

As for measuring, you can look at the percentage of revenue that goes to R&D. However, I also want some efficiency there, so I look at R&D efficiency by dividing revenue growth by the R&D expenses in the previous year.

Mercado Libre spent 10.85% of its revenue on R&D in 2023.

With revenue growth of 35% in Q2 2024, the R&D efficiency is 3.38, which definitely puts Mercado Libre firmly in the top quartile, based on the 2015-2018 numbers.

Throughout the years, MELI has proven that it can launch and nurture very valuable new products. Think of its payment arm Mercado Pago, for example, or its ads business and, more recently, Meli Mas, the company's subscription service similar to Amazon Prime.

Because innovation is not just throwing out new products and see what sticks, but also and maybe primarily a matter of execution, I maintain Mercado Libre's score of 5/5. Oh, boy, isn't this getting too freaky, with all these maximum scores? Am I a fanboy of MELI? Well, I am, but I just look at the numbers to give my scores. The only total exception is the personal conviction score, which is totally personal, as the name suggests. But even that is based on my years-long coverage of the company.

Must-have? 5/5

Since December 2024

I introduced it because of what Matthew Prince, the founder and CEO of Cloudflare (NET), said, as I reported in the Overview Of The Week #125:

I think that the world is about to get sorted into must-haves and nice to haves.

Is Mercado Libre a must-have? That's a hard one and the answer will be 'it depends'. People often prefer online shopping to physical shopping when they are more money-constrained, as they know that prices are often lower and they are less tempted to buy other stuff they don't need.

Mercado Libre might benefit from this. However, discretionary spending would go down, a force that could pull down Mercado Libre. In 2021 and 2022, spending remained very high on Mercado Libre, though. If you look at the period 2014-2016, which is called "The Great Brazilian Recession," you will see this.

A CAGR of 33% during the worst recession in decades in the company's biggest market? Most companies would give an arm and a leg to have that during the best times. I have always given Mercado Libre 4/5, but the fact that it's gaining market share versus Amazon in advertising shows me that this company is something special. I raised it to 4.5 in the previous quarter because of this.

But then I saw this graph today about e-commerce in Brazil.

Mind you, the last one is an estimate, the rest is reality. So, Mercado Libre's market share went up from 26% in the first quarter of 2021 to 45% in the third quarter. That's despite the so-called threat from Amazon. For me, as a Sea shareholder, I'm also happy with the Shopee growth. But that's not the subject here.

I'm raising the score for Mercado Libre again, to 5/5.

Revenue growth 5/5

Unchanged from the start

This is very simple: how high was the revenue growth over the last twelve months?

For Mercado Libre, that is 35%, with strong currency headwinds, so that deserves a clear 5/5, no discussion.

Revenue growth durability 10/10

Unchanged from the start

Even more important than revenue growth is the durability of revenue growth.

Management Quality Score 10/10

Since June 2022

Excellent management teams are often one of the most important keys to long-term success. I look at the track record, execution, and vision here.

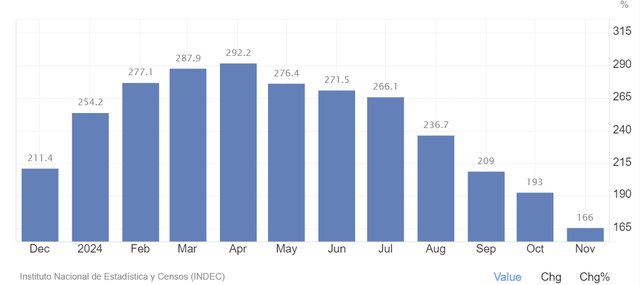

I see a fantastic track record for Mercado Libre in a region that's harder than the US. Argentina, Mercado Libre's home turf and second-biggest market (after Brazil) for a very long time, has seen extremely high inflation for years. It is currently at 166%, down from 292.2% in April.

But things have gotten much better since Milei became President. When he started the month-over-month inflation was 25%. It was at 2.4% in November, compared to October.

Despite these huge inflationary headwinds, Mercado Libre has achieved 35% revenue growth in US dollars! That's an Olympic golden medal in pricing power. Revenue was even up 16% in dollars in Argentina in this quarter, can you imagine?

MELI is very adaptable and changes quickly if necessary. Marcos Galperin has instilled a company culture like few others have done before him. But his co-founder, Stelleo Tolda, is often not appreciated enough. He successfully launched Mercado Libre in its biggest market, Brazil. He was the leader there too for the first 10 years, before becoming COO of the group and Executive VP for Latin America (which is all of the company's market).

I will examine this question more in the future: How deep is management quality? This is inspired by Phil Fisher's 15 questions. I refer to question number 9 here.

I had an interview with Fede Sandler earlier this year, which is being edited and will be released next week. Fede is the former IRO (Investor Relations Officer) of Mercado Libre. He touches on this subject and shows that Pedro Arnt, Mercado Libre's CFO for years but now the CEO of DLocal (DLO), was perfectly replaced from within the company.

He also talked about this in the interview we had last year. You can watch that interview here.

It's not always easy to measure the depth of management quality. But in the case of Mercado Libre, I'm pretty confident that several capable people are on the bench, ready to take over if necessary. Pedro Arnt was an outstanding CFO, but when he left to become the CEO of dLocal, he was replaced by another very solid CFO, the current one, Martin de los Santos.

Insiders' Ownership 5/5

Unchanged since January 2024

Does management have skin in the game? This is out of 5, and not 10, as it is not always a make-or-break but often it's a valuable indication.

For Mercado Libre, the only insider with a stake bigger than 1% is Marcos Galperin, although it's through a trust.

At the current price of $1,802, this means about $6.9 billion, which is fantastic and deserves 5/5. I used to knock off a point because the rest of management didn't have a 1% stake, but at this price, that means about $700 million, so you can't expect that from everyone in management.

Multibagger potential 5/5

Since January 2024

To look at multibaggers, the law of large numbers plays a role, which means it's harder to grow your revenue as much in percentages when your revenue is larger. But you shouldn't forget that Latin America is the fastest-growing e-commerce market in the world and that won't change anytime soon.

Combined with new projects just starting out like advertising and Meli+, Mercado Libre's subscription business similar to Amazon Prime, and great opportunities left for Mercado Pago, I think the chance that Mercado Libre becomes a real juggernaut is realistic. Could it be the first $1T Latin-American company? I think it could become possible.

The fact that I even consider such a market cap means that I think Mercado Libre's multibagger potential is big, and hence, I give it a score of 5/5.

TAM & SAM 4.5/5

Changed August 2024

In this short article, I introduced this new score, replacing the multibagger potential for the original recommendation.

TAM stands for total addressable market and SAM for serviceable addressable market, the market you serve because of your specific product and geographical limitations.

In this case, there is a limit to the SAM, as Mercado Libre is focused on Latin America. This is a huge market, and it's growing at fast speed, but still I used to knock off a point for this limitation. But the economy in general will probably grow so much in Latin America over the next decades that I raised this score to 4.5/5.

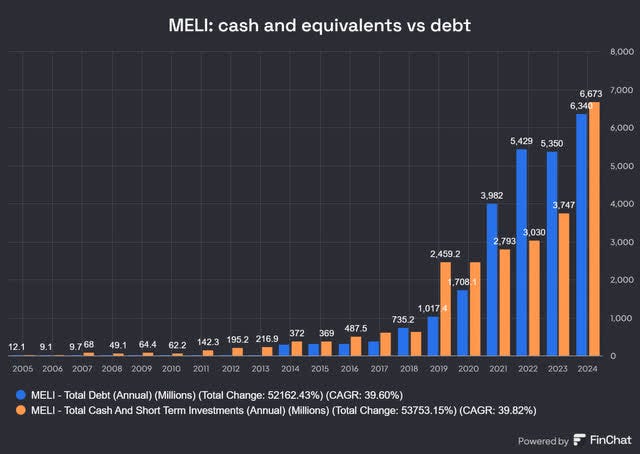

Financial Strength 8.5/10

Since June 2024

Let's make this simple with a Finchat chart.

There is more cash than debt, that's great. Don't forget that with more credit, there will also come more debt. That's OK, though. Mercado Libre is financially in a strong position.

Negative Scores

I also have negative scores, which means I am subtracting points from the score so far. The scores are marked out of 5 because a lot is implicitly captured in the other numbers already.

Risk 1.5/5

Since August 2024

A lot is already baked in financial strength, but this is an overall risk score that shows more than just financial risk.

For Mercado Libre, I used to give 2/5. The company is in a region of the world that is a bit less stable, but it has found a way to navigate the problems for 25 years now. That deserves knocking off half a point.

Competition 2/5

Since the start

How strong is the competition? Again, you can't objectively measure that but there are indications.

Mercado Libre is the big gorilla in the room in Latin American e-commerce. It's the only player all over Latin America, and there is a reason Morningstar puts it in the "wide moat" category. At the same time, I don't want to put the score too low, as competing with Amazon (AMZN) on its core competency and with many local players is intensive.

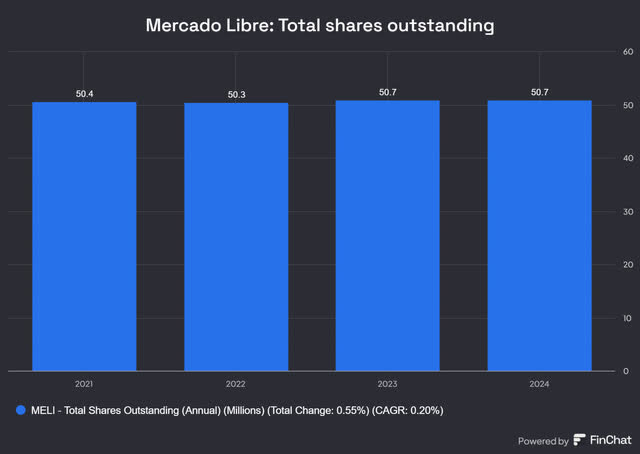

Dilution 0.5/5

Since August 2024

I used to call this SBC (stock-based compensation), but dilution is a better term, as it is broader. Dilution is negative over the long run, but that doesn't mean that companies should not issue stock when they are still growing fast. Look at Apple's shares outstanding before 2012, when it started buying back shares:

At the same time, I don't want to ignore dilution completely, so I give a negative score.

We look at this over a 3-year period to exclude missing something.

This is Mercado Libre's evolution of outstanding shares over the past three years.

As you can see, there's a total dilution of 0.55%, or a CAGR of 0.20%. That's low, but I don't want to fully ignore it. That's why I give a score of 0.5/5.

Scale advantages shared (-5/+5): 4/5

Since July 2022

When I looked back at some of the best investments, they did not only have substantial scale advantages but also shared them with their customers in some way. For Amazon or Walmart (at the time), I think this criterion is obvious. Because they are bigger, they can give their customers better prices.

Google has always had a scale advantage: the more people use their products, the more they can give away for free. While Google leveraged people's data to generate profits, this mechanism also enabled Google to offer so much for free (Gmail, Fotos, Drive storage up to a certain limit, etc.).

I have not come up with this concept myself. This is one that I borrowed from Nick Sleep from Nomad Capital. He uses this concept to guide all of his investments. That's why he started investing in Amazon in 2003 already. He has mostly held on to that position to now. He did the same thing with Costco, another company that shares the advantages of its scale with its customers, by only charging 15% on the purchase price, no matter what. This makes these companies almost impossible to compete with unless you start doing exactly the same thing.

The most prominent advocate of this? Jeff Bezos, who made this napkin sketch about it.

So, this competitive advantage can be significant. I'm going to withdraw or add points with this criterion. For some companies, extra scale only adds extra complexity. Those will get a negative score. I think of Uber (UBER) here. The normal scaling is the second level, which will be given some points. This means that if you grow, your scale gives you cost advantages. The third level is where all users also benefit from the scale. Here, you will see higher scores, 4/5, maybe 5/5.

For me, Mercado Libre is a clear third-level cost-advantage-shared. I rate it 4/5. It follows Amazon's steps closely.

Conclusion

The PM Quality Score went up again, from 87 to 88. Mercado Libre remains a top-quality company and that shines through in all the numbers.

It has the second-highest Overall Quality Score, only after Adyen but before The Trade Desk and Crowdstrike, for example.

The QPI update

For the Quality-Price Score, we first need the Valuation Score.

This is for paid subscribers only. But if you are a free subscriber, I hope you valued this information.