Hi Multis

David wrote an article about Global-e (GLBE), but I added quite a bit, so you can see this article as a joint effort, although let me be clear about that, David did by far the most work.

Of course, as always, after the earnings analysis, I will look at Global-e’s Selling Rules, the PM Quality Score and the valuation to decide if Global-e is a buy now.

Hi Multis

David here.

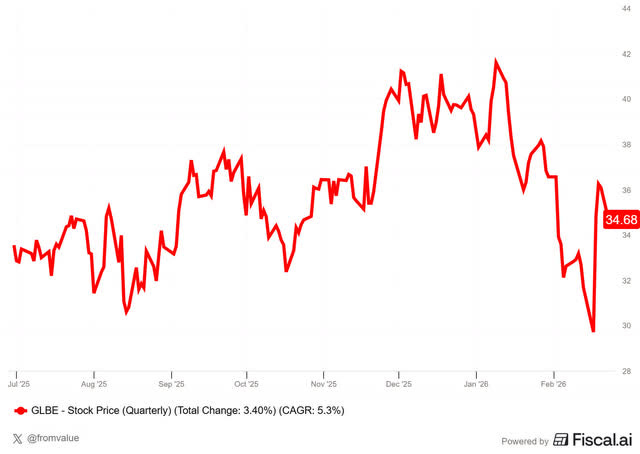

Global-e’s stock recently experienced some weakness, in line with broader market trends, but moved about 15% to $36 following the earnings release. It’s down a little bit to $34.68 at the moment of writing.

So, let’s jump in.

The Numbers

Revenue

Revenue in Q4 was $336.7 million, an increase of 28% year-over-year. The two revenue streams, service fees and fulfillment services, contributed $160.9 million and $175.7 million, respectively. Service fees increased 37% year over year, while fulfillment services grew 20.6% year over year.

One nuance here: the fulfillment take rate came in slightly below expectations this quarter. That’s not a sign of weakness, but because average order values were higher than expected. That means more GMV per transaction, which was good for GMV. So the “miss” on fulfillment take rate is a good miss.

For the full year, revenue mix remained stable with 47% ($451.2 million) from service fees and 53% ($510.9 million) from fulfillment fees. Both segments delivered approximately 27-28% annual growth.

Global-e guided for its first $1 billion+ revenue year in 2026. For any company, that’s a significant threshold.

Gross Profit

Gross profit totaled $154.8 million, compared with $118.7 million in the same quarter last year and up from $99.6 million in Q3 2025. That’s a 46% profit margin.

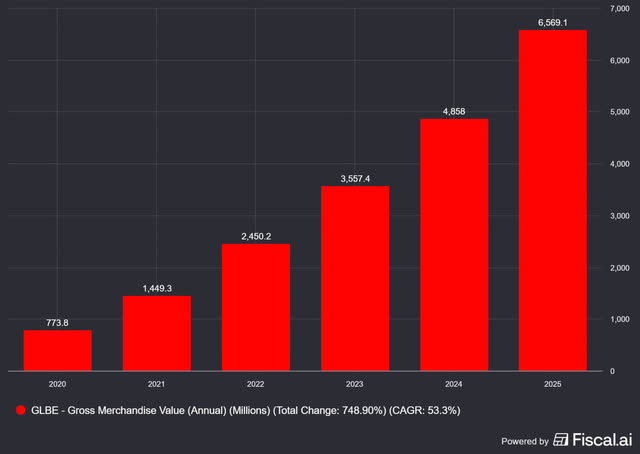

Gross Merchandise Volume (the total dollar amount of everything sold on the platform) increased 37.8% year-over-year to $2.361 billion, bringing the total GMV for 2025 to $6.569 billion, representing 35% annual growth.

A number that puts the GMV in perspective: Global-e’s total annual GMV for 2020 was $774 million. The company did $1 billion in GMV in November alone.

Global-e delivered strong operating results across key metrics, supporting a solid financial foundation for continued expansion.

The result exceeded company guidance across key metrics, and investor sentiment appears particularly positive regarding the company’s forward guidance.

Current Results and Future Guidance

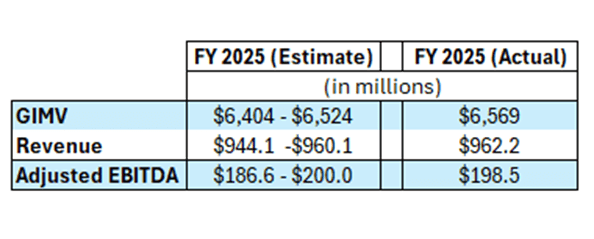

Global-e updated its full-year outlook last quarter to the following:

The improved outlook for GMV, revenue, and adjusted EBITDA was discussed in the previous analysis. Management provided several drivers supporting the higher guidance, which was useful for evaluating how these expectations translated into actual results.

The table below compares company guidance with actual reported results.

This was the first full year of GAAP profitability, with a GAAP EPS of $0.39. The amortization of the Shopify warrant, a recurring drag on GAAP results for years, is now essentially gone. That removes a structural GAAP headwind and makes the reported numbers cleaner going forward.

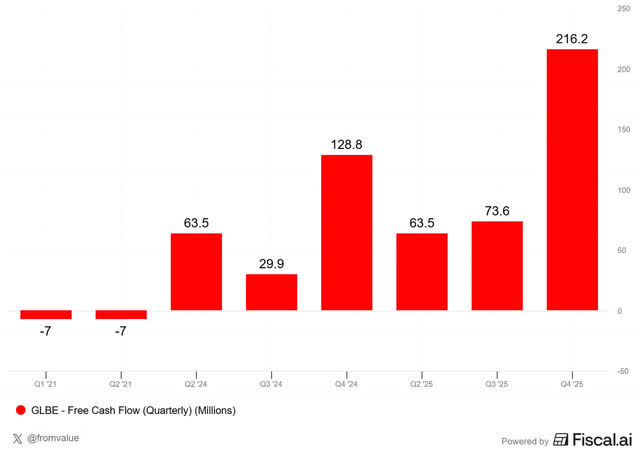

Cash generation remains strong, with $216.2 million in free cash flow generated in Q4.

A portion of this cash is expected to be returned to shareholders. As highlighted previously, Global-e authorized a $200 million share repurchase program.

As of the end of Q4 2025, approximately $72 million in shares had been repurchased, representing about 1.8 million shares. The company indicated that repurchases are expected to continue under the existing authorization.

Management confirmed on the call that the company has continued buying in Q1 2026, with $128 million of capacity still remaining on the program.

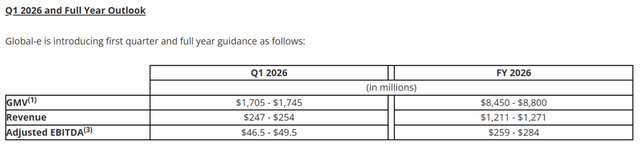

Alongside year-end results, Global-e also released its 2026 outlook:

The company expects GMV growth of 28.6% to 34%, revenue growth of 25.8% to 32%, and adjusted EBITDA growth of 30% to 43%.

The adjusted EBITDA guidance, $259M to $284M, at a 22% margin at the midpoint, would give Global-e a Rule of 50 for the full year. That means revenue growth plus EBITDA margin exceeds 50. Usually, The Rule of 40 is seen as a benchmark for great companies..

Also important: Q1 2026 guidance calls for GMV growth of 38.8% at the midpoint. That’s an acceleration.

The outlook indicates that management expects the growth momentum achieved in 2025 to continue.

Growth

Global-e delivered growth across all key metrics in 2025, and the projected growth rates are not extreme.

The strong GMV demand is currently increasing and is even ahead of the most optimistic projections. This strong performance reflects both new merchant additions and growth from existing merchants, with results exceeding historical averages. Management continues to indicate a strong merchant pipeline.

The net-dollar-retention rate for 2025 came in at 122%, an improvement over 2024. Gross dollar retention was 96%. These numbers tell you two things: existing merchants are growing on the platform, and very few are leaving. The 122% NDR means that even without signing a single new merchant, revenue would still grow by 22% from the existing base alone. Very strong.

And that will probably continue. President and co-founder Nir Debbi said on the call that it “looks stronger today than it did in the same period in 2025.” 2025 was already a record year for growth in new merchant contributions, so that statement deserves attention.

Another tailwind can be found in foreign exchange (’FX’). As Global-e is in the middle of international transactions, the FX part of its business cannot be underestimated. Global-e collects revenue globally, but reports in USD.

With a weakening dollar, it can report higher revenue and profit in USD.

The table above illustrates Global-e’s geographic revenue mix. Approximately half of the revenue is generated in the United States, while the remainder is derived from international markets. As a result, a meaningful portion of revenue is affected by foreign exchange movements.

The partnership with Shopify continues to deliver strong results. The collaboration supports continued expansion of the merchant base and geographic coverage.

More specifically: Managed Markets 2.0 is now live. The critical upgrade in this version is full integration with Shopify Payments, replacing the separate payment rails used in the previous version. This means merchants can now run their international store exactly the same as their domestic store; they have the same processes, the same financial flows, and no learning curve. CEO, Chair of the Board and co-founder Amir Schlachet called it the biggest change. Management expects this to have an even bigger effect in the back half of 2026.

And one more thing, Global-e has already integrated the Universal Commerce Protocol (’UCP’), co-developed by Shopify and Google. As agentic commerce evolves, the complexity of cross-border infrastructure only increases and that is exactly what Global-e is built to handle. The company is more than ready.

Tariffs as a lead-generation mechanism

And then... we have to talk about tariffs. It was by far the most discussed topic on the call and one of the things I (Kris) am most asked about in the context of Global-e.

When the tariffs were introduced in 2025, in the short term, this created some pressure on US volumes. But as Amir Schlachet said on earlier calls, the tariff complexity had a positive effect on the pipeline in the midterm and that is now showing up in the Q4 numbers and 2026 guidance.

The EU de minimis removal is the next wave. Until now, small packages into Europe could pass customs without an import tariff. That’s about to end. When that comes into effect, it adds another layer of trade compliance for merchants, which is another boost for Global-e. Companies that previously shipped small parcels into Europe without customs handling will now need what Global-e does.

Global-e also launched its duty drawback offering for U.S.-based merchants in Q4. It allows merchants to reclaim import duties on internationally exported goods, and reclaim certain tariffs on returned goods. Initial adoption among the first group of merchants is described as “very high,” and it’s now being rolled out to all eligible U.S. clients. It’s embedded in the 2026 guidance, though management took a conservative approach given it’s still a new offering.

Saying to merchants: “Hey, if you just take this subscription, you will earn it back multiple times through claimbacks, where we do all the complicated stuff for you” is a pretty good selling point.

Or, in other words, the tariffs are an outstanding lead-generation mechanism for Global-e. Back to you, David!

Costs

One aspect I always look at is the costs. Not only the costs to generate revenue, but also the other costs that a company chooses to make, such as sales and marketing, and general and administrative costs.

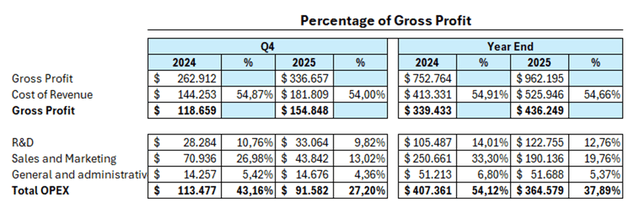

The table below presents these costs as a percentage of gross profit. The left side compares Q4 2024 with Q4 2025, while the right side compares full-year 2024 with full-year 2025.

Cost of revenue remained stable at approximately 54% in both 2024 and 2025, with limited variation on a quarterly basis. These costs are typically more difficult to optimize and include items such as payment processing fees, shipping, and logistics.

Operating expenses declined relative to gross profit compared with both the prior year and the comparable quarter, contributing to improved profitability.

More numbers:

R&D dropped from 9.2% to 8.5% of revenue in Q4.

Sales and marketing fell from 11.3% to 9.4%.

G&A from 4.1% to 3.2%.

You see that everything moves in the right direction. Management is guiding for this to continue.

AI and Other Improvements

Global-e is increasingly using artificial intelligence to improve growth and operating efficiency.

One example is a large language model used in customer support, where chatbot interactions are reducing the need for human intervention.

Another example is an internally developed AI tool designed to improve sales efficiency. The tool analyzes customer characteristics, product attributes, and geographic priorities to estimate conversion potential before sales outreach. This helps improve demo targeting and conversion rates while supporting more efficient sales and marketing spending.

But the AI story at Global-e goes considerably deeper than these two examples.

Vibe coding is already having a measurable impact. Entire features and even entire subsystems are designed, developed, tested, and deployed through AI-assisted coding. The efficiency gain is already visible in the lower R&D spend as a percentage of revenue in 2025.

Global-e also launched a full-site localization offering. It’s an in-house LLM-based service that translates entire merchant websites into multiple languages, including text embedded in graphics, a common problem for merchants.

Amir Schlachet made a good point on the call about this. Scale and AI are not separate advantages but they compound each other. Data fuels AI models and Global-e has unique, proprietary transaction data across 200+ markets that no competitor can even dream of.

The bigger Global-e gets, the better the models get. That’s a self-improving moat over time.

Conclusion

Global-e posted a strong quarter and 2026 looks to be strong as well. Does that make it a BUY?

Let’s find out with the Selling Rules, the PM Quality Score and the valuation.

If you want the full advantage of Potential Multibaggers.

Go to this page.

Subscribe to the annual plan.