From $115 to $56: Is The Trade Desk Finally Cheap?

Does this quarter effect the Quality Score? And is the stock cheap now?

Hi Multis

The Trade Desk dropped by more than 40% after the earnings.

That's why I wanted the earnings analysis out as quickly as possible. You can read it here if you haven't done so yet.

But is the stock a buy now? Has the quality declined? And how about the valuation? Some say it’s a screaming buy now, others call it ‘still very expensive.’

At this point, I'm probably as curious as you are to see the impact of the last quarter and the guidance for the next quarter. Let's find out together.

Personal conviction 9/10

Since February 2025

This is my or your own conviction based on everything I/you know about the company. Your personal conviction may be very different than mine and you can adapt this score to your own liking.

You can download the sheet here to give your own score alongside me.

I have followed this company for so long already, long before I finally decided to buy the stock in May 2019 at (a split-adjusted) $19.5.

Over six years of intensely following the company has made me realize how unique this company and its CEO are. Up to Q4 2024, my conviction was always 10/10. That doesn't mean there's no doubt at all, but that it's the highest possible level of conviction in investing.

I downgraded my conviction score to 9/10 after that quarter. I don't see a reason why I would slash my conviction score further. The stock price reaction was fierce but the quarter was solid. There were headwinds from the tariffs and the tough comps but the quarter was strong enough. That's why I keep my conviction score at 9, which is still high.

Profitability 9.5/10

Since October 2024

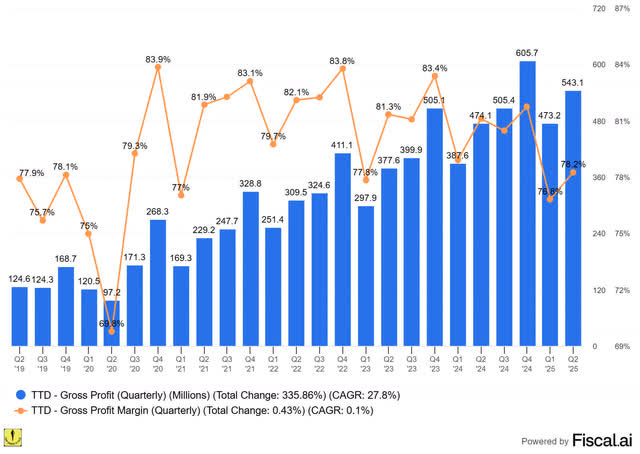

You can see that the gross profit has a CAGR of 27.8% since Q2 2019.

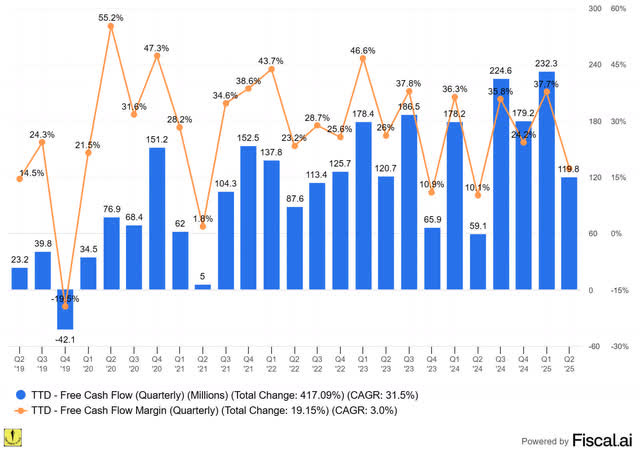

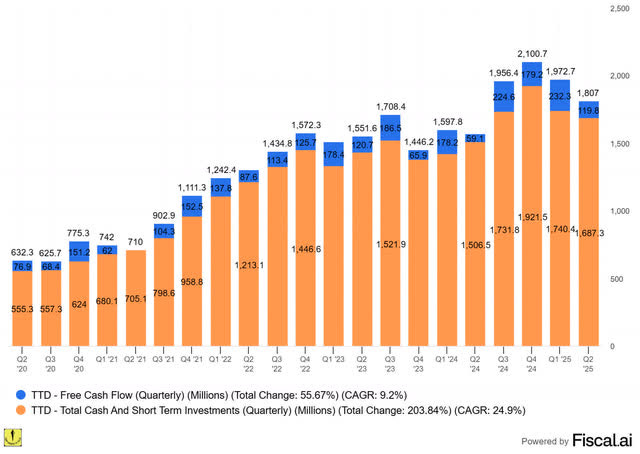

Again, the quarters are volatile, but the company has generated positive free cash flow in every quarter since Q1 2020.

The Trade Desk has also been profitable on a GAAP net income base every year since 2013. Except for three quarters (one because of the IPO, two because of stock-based compensation), that has been even the case in every single quarter since 2013.

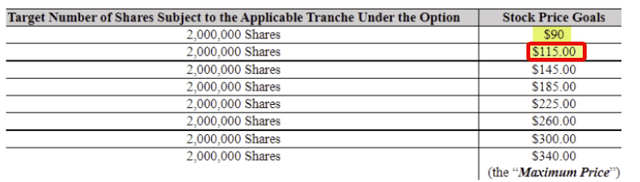

The dip in GAAP net income you see in 2022 is due to the big stock bonus Jeff Green got for getting the stock price above a certain level. Other such bonuses are also in his contract. I don't mind these too much, as they are not automatic. The stock has to be at certain levels for at least 30 trading days before he gets the bonus. This is the compensation summarized.

The stock crossed $115 in October 2024 and that why Jeff Green's compensation plan kicked in. The next trigger is $145. But we are very far from that now, of course.

If Jeff Green achieves all those targets before the plan expires in 2031, he will have received 16 million shares. Of course, we will return to this when we look at the dilution, as this is about profitability.

The Trade Desk is profitable on all ratios you can think of. That's why I keep my score at 9.5/10.

Sales efficiency 5.5/10

Since August 2025

The sales efficiency formula first looks at S&M (sales and marketing) as a % of revenue. Then I look at growth this year and the expected growth next year and I take the average. That is divided by the S&M number. That gives me the marketing efficiency. If you add gross margins then and you multiply, and divide by 10, you get the efficiency score.

These are TTD's numbers.

As you can see, the score is 5.5, mostly as a result of the lower revenue growth and guidance.

Innovation 4/5

Since August 2025

This is part subjective, part measurable. Subjective as in: how many new products does the company issue versus its competitors? You can partly measure that, too, if you want, but the magnitude of the innovations is much more important than the sheer number of innovations.

As for measuring, you can look at the percentage of revenue that goes to R&D. At the same time, I want some efficiency there, too, so I look at R&D efficiency by dividing R&D expenses in the previous year by revenue growth in the trailing twelve months. Let's look at how The Trade Desk does.

The company spent 18.95% of its revenue on R&D last year.

With revenue growth of 18.73%, the R&D efficiency is 0.99, which puts TTD in the second quartile, a drop from the first quartile.

With the continuous roll-out of innovations like UID, the complete rehaul of its platform with Kokai, the long-time use of AI, and many other big, impactful new initiatives, I think The Trade Desk still deserves cedit on the qualitative side, but the lower R&D efficiency warrants a drop from 4.5, which The Trade Desk had since introducing this system in 2022, to 4/5.

Must-have? 4/5

Unchanged since June 2022

I introduced it because of what Matthew Prince, the founder and CEO of Cloudflare said:

I think that the world is about to get sorted into must-haves and nice to haves.

The sector TTD is in is sensitive to the economic cycle, of course. We saw that again with the impact of tariffs this quarter.

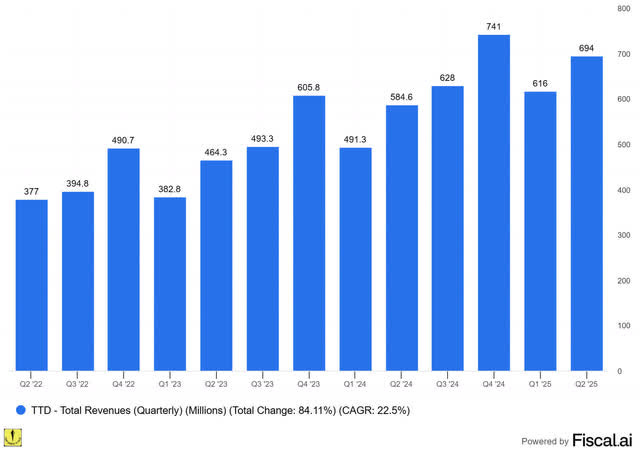

Revenue growth 4/5

Since February 2025

This is very simple: how high was the revenue growth over the last twelve months? For The Trade Desk, that's 18.73% this quarter. That's still high enough, but with the guidance for 'at least' 14% revenue growth in Q3, I thought about taking down half a point. I decided to wait, though. Also because the company foresees a re-acceleration in revenue growth next year.

Revenue growth durability 9/10

Since August 2025

At least as important as revenue growth, is the durability of revenue growth. This is what I always wrote:

The Trade Desk has a gigantic TAM and the trend is moving away from the walled gardens. With so little real strong competition when it comes to the open internet, with CTV still expected to grow for so long, and the company's innovation and execution, I rate The Trade Desk the maximum score here, 10/10.

Now, after this quarter, I wonder if that's still true. I think it is, but I'm not as convinced as before, which costs The Trade Desk a point. Here too, the score had always been the same since the start of the Quality Score in 2022: 10/10. So, you see that I try to stay flexible and objective in the scoring.

Management Quality Score 10/10

Unchanged since the start

Jeff Green is one of those rare CEOs that I will rate 10/10. Everything he predicted, including things outside his own influence, became a reality. IDFA postponed? Yep. 3rd-party cookies postponed? Yep. CTV growing like gangbusters? Yep. I could go on, but I think you know what I mean.

The introductory remarks of The Trade Desk's earnings conferences are fantastic overviews of where ad tech stands. Also, you shouldn't forget that he invented ad-bidding exchanges in 2002 already. Q4 2024 was a bad quarter and he owned the mistakes that had been made. But this was NOT a bad quarter, despite the ugly price drop. So I see no reason to change the score.

Insiders' Ownership 5/5

Unchanged from the start

Does management have skin in the game? This is out of 5 (and not 10) as it is not always a make-or-break but often it's a useful indication.

Founder, Chairman and CEO Jeff Green owns 4.75 million Class A shares and 42.24 million Class B shares. That means he owns almost 47 million shares of a total of 489.9 million. That's more than 9.6%, worth more than $2.62 billion with the current stock price of $55.69. That's a very high ownership stake and worth 5/5.

Multibagger potential 4/5

Since February 2025

When I picked The Trade Desk, it had a market cap of $9.5 billion. Right now, it trades at a market cap of $39.6 billion. That means it will probably be harder to 10x over the next 10 years, but I think it's more doable now than when the market cap exceeded $60 billion. That's why I add half a point to this score.

Of course, the multibagger potential also depends on revenue growth, which is by far the most important contributor to long-term stock performance.

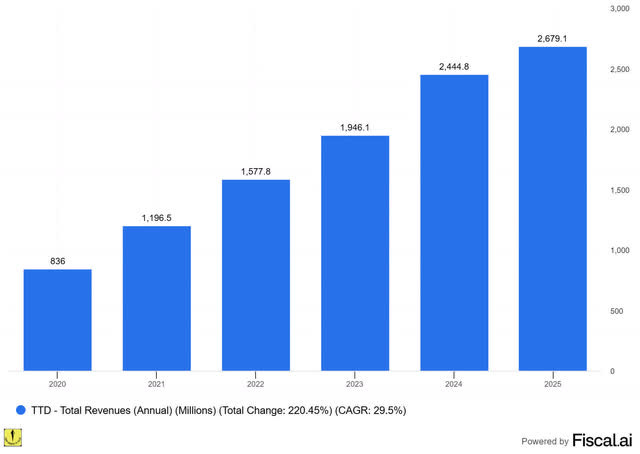

The Trade Desk has grown its revenue by 22.5 % in the last 3 years and 29.55% in the last five years.

Revenue growth is expected to moderate in the next years, though.But of course, it's tough to forecast, as there are so many moving parts.

Now, suppose that 20% would become the norm in the next years, even with the multiple coming down, it could be a fivebagger, not bad at all, too, of course. In the end, we'll have to see.

The Trade Desk's TAM (total addressable market) has only grown, and it is an important player in CTV. So, it has the potential to become really big, like in a few hundred billion. I'm just pointing out the potential, nothing more. But it's enough for me to keep this score the same, especially at this price.

TAM/SAM: 5/5

Unchanged from the start

TAM stands for total addressable market and SAM for serviceable addressable market, the market you serve because of your specific product and geographical limitations.

Both the TAM and the SAM are huge for The Trade Desk. Advertising is poised to become a $1T market. That's per year, yes. Jeff Green is convinced that all advertising will become programmatic. So, The Trade Desk plays on a huge field of opportunities, the field where Google and Meta became such gigantic players.

Financial Strength 10/10

Unchanged since the start

In this environment, financial stability is much more important too. That's why I rate it out of 10.

If we look at the financial strength of The Trade Desk, the first thing we notice is that the company has no debt. With a cash position of more than $1.69 billion and additional free cash flow, The Trade Desk is financially unshakeable.

There are two reasons the cash has shrunk a bit: buybacks and acquisitions. But with no debt, I like that the company doesn't just cuddle its money but uses it.

So, I think a 10/10 is warranted here, especially because the company has been profitable every year since 2013.

The negatives

I also have negative scores, that can subtract extra points from that score. The scores are marked on 5 because a lot is implicitly captured in the other numbers.

Risk 1.5/5

Since February 2025

A lot is already baked into financial strength, but this is an overall risk score that shows more than just financial risk. It's also the risk that you will lose money if you hold for ten years.

I think there's no reason to believe that The Trade Desk has become riskier now. To the contrary, even. With the lower stock price, the risk of losing money has even decreased.

Competition 2/5

Since July 2024

How strong is the competition? Again, you can't objectively measure that but there are indications.

For The Trade Desk, it competes with the big boys. Walled gardens are under more and more pressure, both from the governments around the world and competitive pressures; they might be extra dangerous. When cookies are abolished, The Trade Desk has UID 2.0. Up to now, that has worked well to compensate for things like Apple's IDFA change.

When it comes to the open internet, The Trade Desk is the clear leader, also on CTV. However, YouTube still has a large portion of streaming, and Amazon has an increasing number of ads, which is not really attainable for The Trade Desk.

Now, there are some workarounds, but that inventory could become even more valuable in the future. That, to me, is the biggest risk.

AppLovin announced it would start in CTV as well and it could become a competitor of The Trade Desk as well, but for now, it's not a real competitor yet.

Overall, the Trade Desk will benefit from the move to programmatic advertising, even if the big boys also do well.

Dilution 0.5/5

Since October 2024

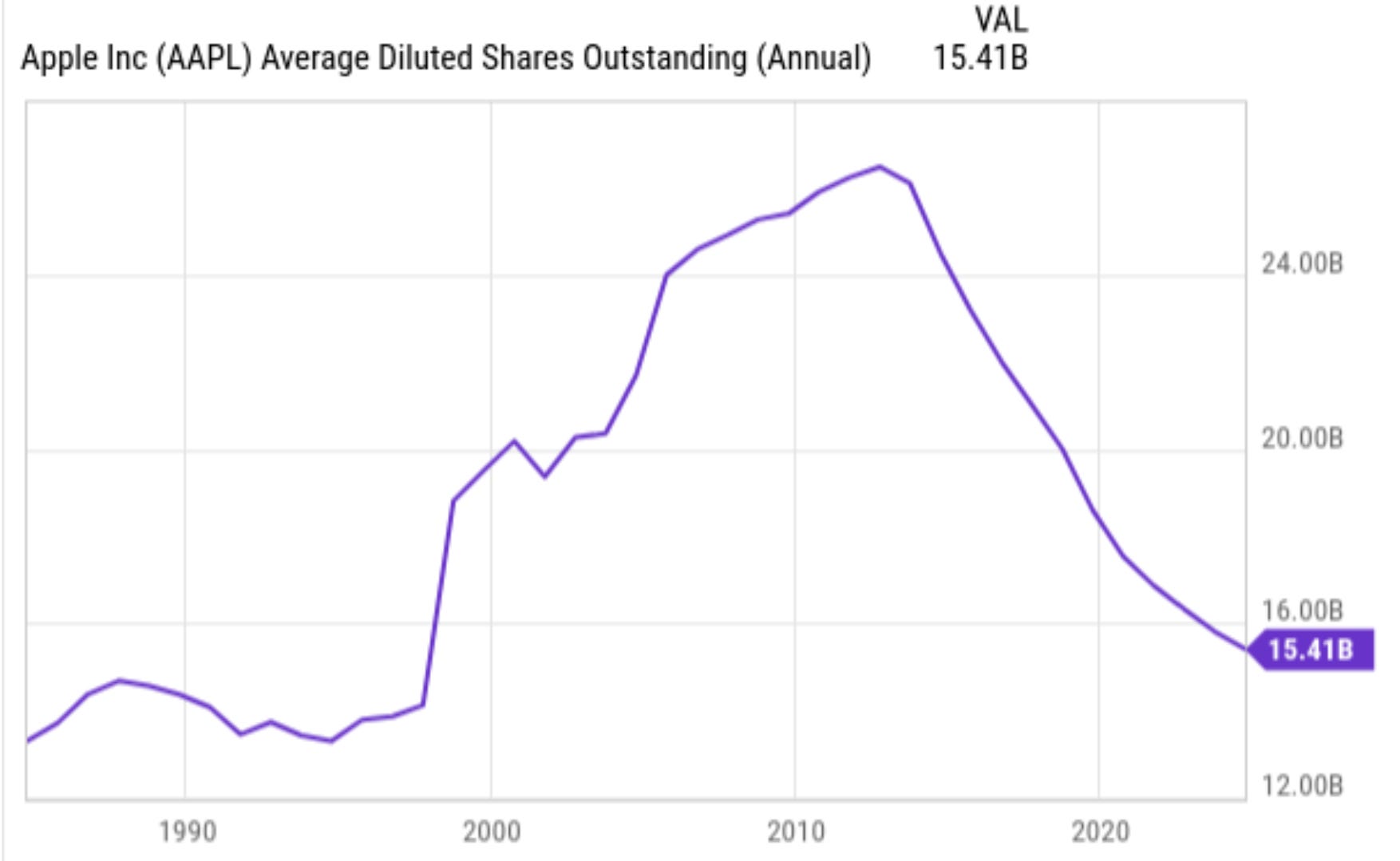

Dilution is a negative over the long run but that doesn't mean that companies should not issue stock when they are still growing fast. Look at Apple's shares outstanding before 2012, when it started buying back shares:

Here we have to talk about Jeff Green's big bonus again. You know, this one, that I already shared before.

If Jeff Green gets all those targets before 2031, when the plan expires, he will have received 16 million shares.

Right now, there are 493.96 million fully diluted shares outstanding. That already included the first two tranches, of course. That means if Jeff Green gets all the remaining 12 million shares, that would mean a total dilution of 2.4%. For 6.2x of the current stock price before 2031, I think that would be a small price to pay. That's a CAGR of 44%.

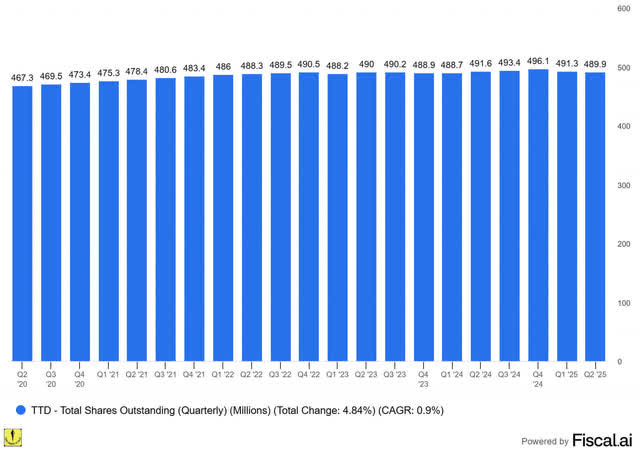

This is the evolution of The Trade Desk's outstanding shares over the last five years.

As you see, in the last five years, there was a total dilution of 4.84%. The CAGR is 0.9%.

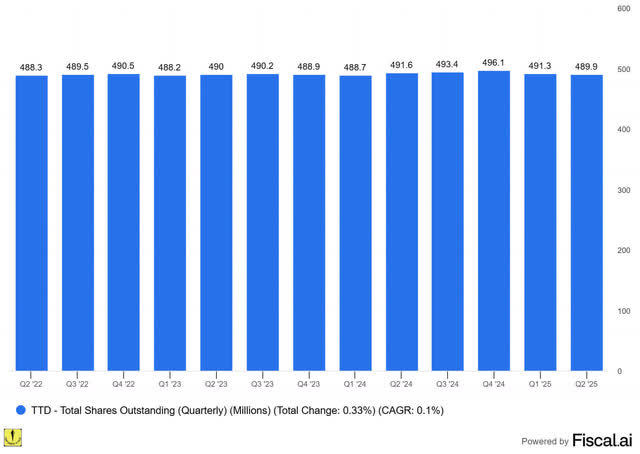

Over the last three years, the dilution was even lower, at 0.33 or a CAGR of just 0.1% per year.

(PS: I'm very happy Fiscal AI (formerly Finchat) provides all these wonderful charts, forecasts, conferences, earnings calls, and SOOOO much more. And it’s affordable, unlike many good data platforms. If you want to try it out you can do that here. You also get a 15% discount if you take one of the paying plans.)

That's also because The Trade Desk has bought back shares opportunistically. I would not be surprised that they are buying right now.

With its big war chest, no debt and a robust free cash flow generation, those buybacks make sense. Normally, that would not be the case, but The Trade Desk is already investing heavily in its R&D and infrastructure (and people), promised to ramp that even up, doesn't have to pay off debt, already and a dividend would be less efficient than a buyback. I'm happy with the buyback.

The company earmarked $700 million for buybacks in Q4 2024 and there was $53 million left from the previous buyback program. Of that $753 million, $375 million remains for share repurchases.

That's why I keep the score of 0.5.

Scale Advantage Shared 4/5

Unchanged from the start

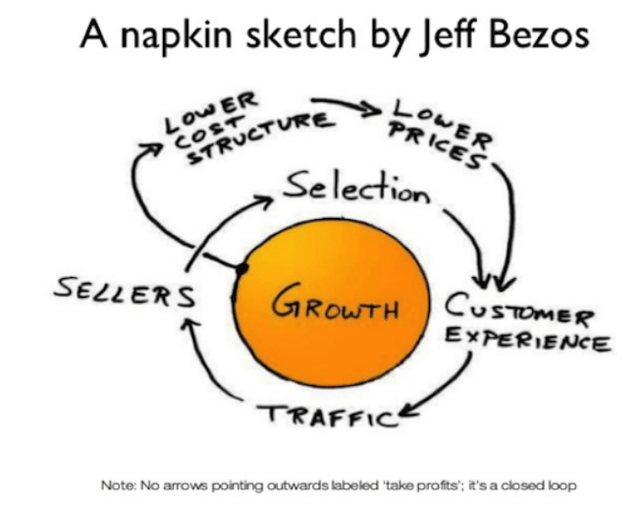

When I look back at a few of the best investments, they not only had substantial scale advantages, but also shared them with their customers in some way. For Amazon or Walmart (at the time), I think this criterion is obvious. Because they are bigger, they can give their customers better prices.

For Google (GOOGL), for example, it was maybe not that clear. But Google has always had a scale advantage: the more people use their products, the more they can give away for free. The data of people was leveraged to generate profits for Google, but the fact that Google could offer so much for free (Gmail, Photos, Drive storage up to a certain limit, etc.) was because of this mechanism.

I have not come up with this concept myself. This is one that I borrowed from Nick Sleep from Nomad Capital. He uses this concept to guide all of his investments. That's why he started investing in Amazon in 2003 already. He has mostly held on to that position to now. He did the same thing with Costco, another company that shares the advantages of its scale with its customers, by only charging 15% on the purchase price, no matter what. This makes these companies almost impossible to compete with unless you start doing exactly the same thing.

I came across this concept in Richer, Wiser, Happier a few weeks ago and I dug deeper by reading several articles (like this one) about Sleep and this concept more particularly. The most prominent advocate of this? Jeff Bezos, who made this napkin sketch about it.

So, this competitive advantage can be significant. I'm going to withdraw or add points with this criterion. For some companies, extra scale only adds extra complexity. Those will get a negative score. I think of Uber (UBER) here, although that probably has changed because of the services it added. The normal scaling is the second level, which can be given little to no points. This means that if you grow, your scale gives you cost advantages. The third level is where all users also benefit from the scale. Here you will see higher scores, 4/5, maybe 5/5.

I give The Trade Desk 4/5, as the data its customers bring it can be leveraged on the platform for everyone. So, for example, if you want to target female 30 to 35-year-old women with a Master's degree in Malaysia, that's possible because the data of all customers is used anonymously by the AI The Trade Desk has employed. That's incredibly powerful.

Conclusion

The Trade Desk's Potential Multibaggers Quality Score drops from 81 to 78. That's at the same time still a high score overall and the lowest score the company has ever had.

The Quality Score is only half the story, of course.

The real edge comes from knowing exactly what to do with it and that’s in my updated valuation analysis and Buy–Hold–Sell verdict.

After a 40%+ drop, is The Trade Desk a screaming buy or a falling knife?

You’ll see my valuation breakdown, exact rating, and where TTD now ranks among all Potential Multibaggers, but only if you’re a paid member.

Free readers: upgrade today to unlock this decision, my full portfolio, and every future pick the moment it’s released.

Even one well-timed call can pay for your subscription, like my Adyen buy in 2023 after it dropped 40%. It gained 90% in just a few months.

On top of that, the price of the subscription will increase from $479 to $499 soon. So, grab the lower price now!