Hi Multis

A few months ago, I wrote about Duolingo (DUOL) after a Q4 release the market really disliked, mostly because the 2026 guidance implied a deliberate slowdown. The stock fell 20% in after-hours and kept sliding.

Source: Duolingo

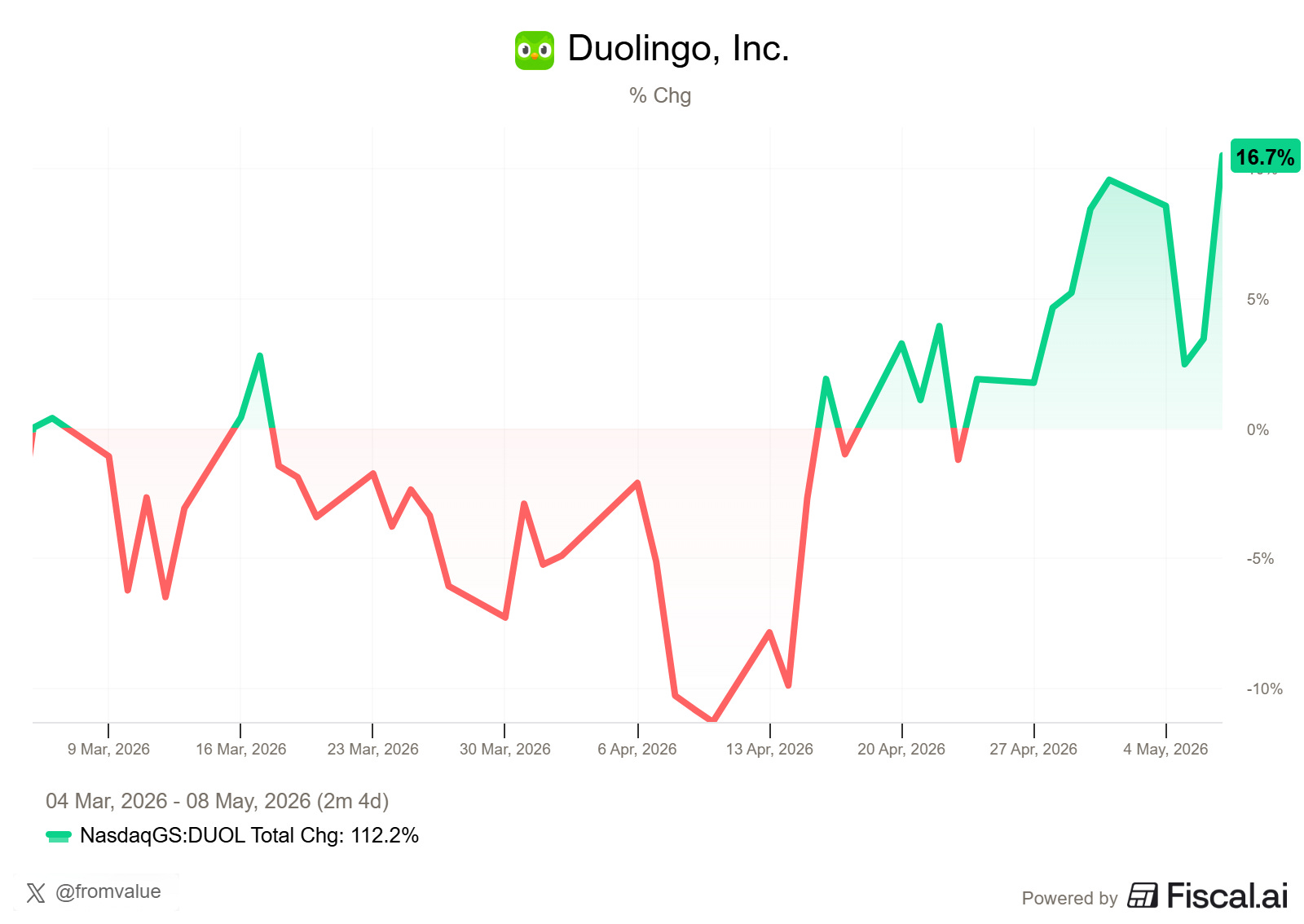

Since then, the stock has done more or less nothing. It bounced around in the $90-$110 range while the rest of the market was busy discovering new ways to be nervous or greedy (in semis). But in the last days, it saw quite a jump.

After Monday’s Q1 2026 release, Duolingo dropped 15% or so in after-hours but closed -5.6% on Tuesday, the same number as the full period after my previous article. Yesterday, it was suddenly up more than 8%. Long-term moves are often much easier to understand than the short-term silliness.

Of course, I hoped that there would be some relief. Mind you, I’m not getting desperate or need relief myself, but I know many of you are in stress about this position and could use some relief. Unfortunately, that’s not how the stock market works.

After going through the shareholder letter, the call, and Luis von Ahn’s recent communications, I think this quarter actually told us something important. Not the kind of thing that moves the stock the next day, but the kind of thing long-term investors should care about.

Let me walk you through the numbers first.

The Numbers

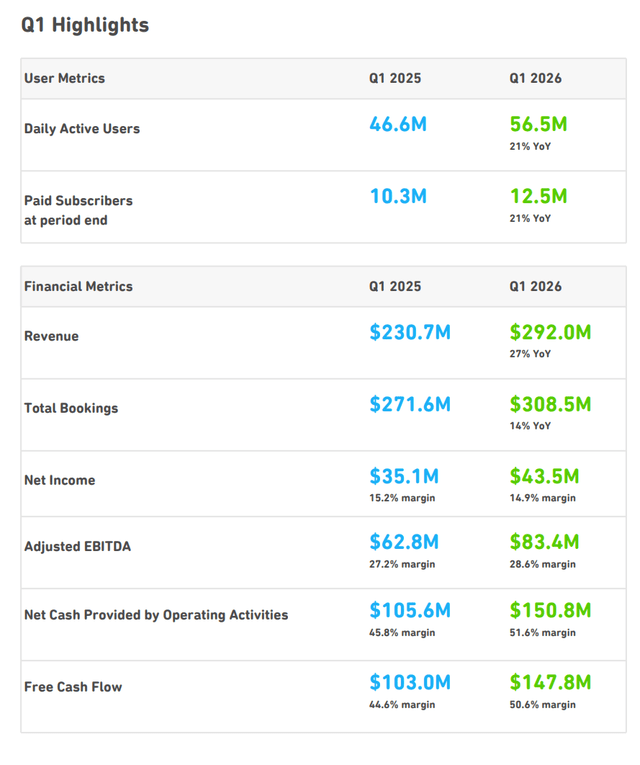

Q1 revenue: $292M, +27% YoY (+22% constant currency), beating estimates by about $3M, but it beats the company’s own guidance by 2 full percentage points.

EPS: $0.89 vs consensus of $0.79.

Total bookings: $308.5M, +14% YoY (+9% constant currency) vs 11% guidance.

Subscription bookings: $268.1M, +15% YoY.

Subscription revenue: +31% YoY. The core engine is still humming.

GAAP gross margin: 73.0%, up 190 bps YoY.

Adjusted EBITDA: $83.4M at a 28.6% margin, up 140 bps and better than the 25.5% guidance the company gave.

Free cash flow: $147.8M, a 50.6% margin. That’s impressive for a quarter the market calls a failure.

Net income: $43.5M, +24%.

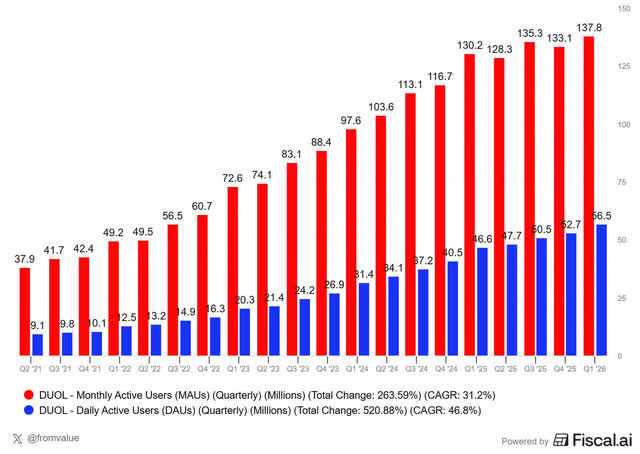

DAUs: 56.5M, +21% YoY (lapping a 49% comp from the “Dead Duo” campaign).

MAUs: 137.8M.

Paid subscribers: 12.5M, +21%.

Here’s an overview from the Shareholder Letter.

Everything in this quarter was stronger than expected. So, where did the negativity come from? Bookings grew 14% reported, but only 9% on a constant-currency basis, and guidance for Q2 is just 5.8% bookings growth. That’s all the market cares about right now, because bookings lead revenue by a couple of quarters. So if you want to know what 2027 revenue growth looks like, you look at 2026 bookings. And those don’t look great.

I’ll come back to that low guidance, but first, let’s spend some time on the part of the strategy I find genuinely encouraging.

The DAU/MAU Ratio

Last quarter, I told you that the percentage of monthly users who are also daily users had reached about 40%, an all-time high and very impressive for a freemium consumer app.

This quarter, it went up again, to 41%.

Fiscal now runs a 25% off campaign. Don’t hesitate, it ends soon!

Why does this matter? Because when management deliberately changes strategy to reduce friction in the free experience, the easy bear story is: “they’re attracting lower-quality users now.” I’ve seen that take multiple times on X. But lower-quality users would mean the DAU/MAU ratio drops. The opposite happened, so you can ignore that bearish take, I think.

This was actually one of the items on my Selling Rules from last quarter. I said I expected the ratio to drop a bit (and that would be okay). It didn’t. So far, so good.

Luis von Ahn made an interesting admission on the call when an analyst asked about MAU deceleration. He said:

In terms of growth, the main thing we work on here is daily active user growth. That’s the main thing we have worked on for the longest of time, and monthly active user growth, there’s just no team that’s looking at that, and we do report it, but it’s just not a team that’s looking at that.

That’s refreshingly honest. The company doesn’t even have a team focused on MAUs. They focus on daily engagement and retention, and the MAU number is a consequence of marketing, word-of-mouth and product quality. MAU is an output, not an input, but I think almost every single analyst and investor sees this wrong. I understand that because this is different than other businesses, but it is important to be granular enough if you analyze a company.

Von Ahn went on to say top-of-funnel has been “about flat for this quarter” and that they want to accelerate it, particularly through marketing in underpenetrated regions and product improvements that drive word-of-mouth. More on that in a moment. This shows the plans of management and it should also demonstrate why you shouldn’t panic about the MAUs.

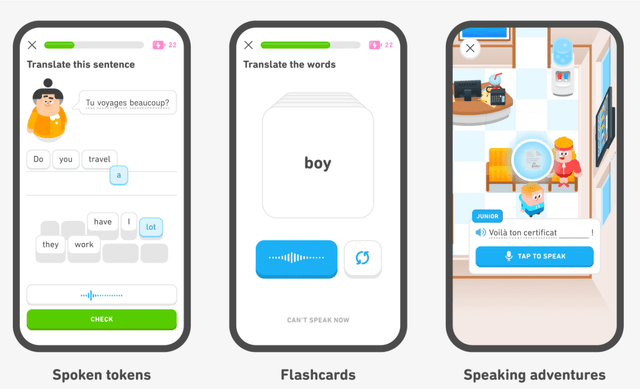

So, let’s focus on the product that should fuel growth over time. In Q1, Duolingo made speaking practice a central feature, not an add-on:

Spoken tokens: you can now answer almost any exercise out loud instead of tapping.

Flashcards: for fast verbal recall: saying words aloud rather than reading them.

Speaking Adventures: real-world conversational scenarios tied directly to the curriculum.

Video Call continues improving, and it’s expanding to Super subscribers (as promised last quarter).

The most concrete data point Luis von Ahn gave: the average words spoken per user in Video Call has more than doubled year-over-year.

Source: Shareholder letter

This is one of those details that people who don’t follow the company closely will miss. The conventional view of Duolingo is “the app where you tap matching words and the owl judges you.” Speaking has historically been the weak spot, the thing critics pointed to when arguing that AI tutors would eat Duolingo’s lunch. Well, speaking is now everywhere on Duolingo, and it’s getting better.

That brings us to content. In Q1 alone, Duolingo published 20,500 course units. That’s amazing. To put that in context:

That’s almost 3x the rate of 2025 (~7,100/quarter).

It’s more than 10x the rate of 2024 (~1,800/quarter).

It’s about as much in one quarter as the company shipped in the entire year of 2025.

Luis von Ahn’s comment on the call:

And that’s in 1 quarter, and that’s about what we put out the entire year last year. And by the way, last year, we were already using AI. So we’re just getting better and better at using it.

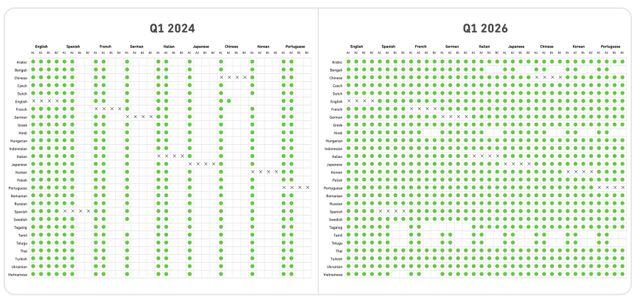

The map of which language pairs are taught up to which proficiency level is now nearly fully covered, all the way to B2 (professional proficiency, “Duolingo Score 129”) across the nine most popular languages. Visually, you can see this in this image.

There’s a quiet point hidden in this. Duolingo has been telling investors for a couple of years that intermediate and advanced English content was a major TAM expansion opportunity but that uptake would take years because word-of-mouth is slow. Now they have the content, so that “couple of years” clock has started. That’s a 2027 and 2028 story, not one for 2026, which is exactly why it doesn’t show up in this year’s bookings. Of course, you have to trust management that this will pay off, but if I look at the past, I wouldn’t know why not.

The other thing that came out of this content build is something I find really interesting. Once you have all the content, you can start using AI to personalize what gets shown to which user. Luis von Ahn:

We may even start generating content just for you. Based on everything that we know about you, we may just be able to generate content just for you, maybe not the immediate next exercise, but like two exercises from now based on everything. We’ve just generated that sentence just for you or that piece of content.

This is the part where Duolingo’s data moat starts compounding in ways that no LLM-built clone can replicate. Anyone can use AI to generate language exercises. Only Duolingo has a billion+ user hours of data telling it which exercises to generate for which user at which moment. That’s the difference between a tool and a learning system.

There’s another quiet but important change this quarter. Duolingo added a session at the end of each unit to assess whether the learner has actually mastered the concepts. If they haven’t, they don’t move forward.

This sounds like a small change, but it shows Duolingo’s intentions. For most of Duolingo’s history, the product was optimized for engagement: keep the streak alive, keep the dopamine flowing, keep coming back. Critics could easily claim that you could maintain a 500-day streak without actually learning much. Mastery checks are the company’s answer to that. You can’t progress without proving you learned the thing. That’s the right decision, in my opinion. Any learning comes with tests.

But there’s more. Better learning outcomes mean stronger word-of-mouth, which is the cheapest and most powerful growth lever this company has ever had. Luis von Ahn said it himself: word-of-mouth is “free, but we don’t have that much control over it.” You control it by making the product genuinely effective, so users tell their friends.

One of the more striking admissions on the call for me was about performance marketing. Luis von Ahn:

We’re pretty excited about that just because we’re finally building the infrastructure to have the right attribution to send users to the right place after you acquire them, et cetera, that a company our size should have probably built years ago, but we kind of just ignored it.

A company with 56 million daily active users is just now building a proper performance marketing infrastructure. Most consumer apps do this in their first year. Duolingo got to a global scale through pure word-of-mouth and “unhinged” social media, never needing to learn how to buy users efficiently. That’s pretty impressive, even to the level of weird, maybe.

Now they’re learning it, and the most interesting place they’re learning it is China, where Luis von Ahn says they can already do profitable performance marketing. That was the first time I’d heard him speak so concretely about that. He also dropped this number that I want to highlight because few people seem to track it:

China monetizes about as well as Western Europe. So about as well as France, which is not as high as the U.S. but pretty high.

That’s impressive and, again, completely different from all other companies that have much lower average selling prices abroad. The standard bear narrative is that international DAU growth is lower-quality because international users don’t pay. China monetizing like France is a strong rebuttal. And on top of that, after the successful campaigns with Luckin Coffee and Meituan, Duolingo will soon launch a partnership with McDonald’s China. The brand is becoming culturally hot in the largest English-learning market on earth. Few people seem to be paying attention to this but it could become very important in the future. At the same time, let’s be honest: it could also mean there’s a higher risk the app will be copied.

Last quarter, I wrote about the overmonetized/undermonetized paradox. Duolingo is overmonetized and undermonetized at the same time. Undermonetized because only about 12% of monthly active users pay, while comparable freemium businesses like Spotify get to roughly 50%. Overmonetized because the way Duolingo had been pushing that conversion rate up was by adding friction to the free experience, and at some point, that friction started killing the DAU growth that makes the whole flywheel spin.

Luis von Ahn talked about this again this quarter, this time with concrete examples of what “monetization without friction” looks like in practice. The most interesting one:

I mentioned one already, which is longer free trials. This is not something we’ve experimented with a lot, the length of our free trial. But if you look at other subscription businesses that are scaled, they have pretty different free trials. Usually much longer than the one we have. You see 1 month. You sometimes even see 3 month free trials. So you’re going to see us experiment with that, and we are definitely seeing certainly the 1-month experiment we already see. We are seeing that, that both increases revenue, which is good but also it’s not at odds with daily active users.

Then he added something that I think is one of the most revealing comments of the entire call:

Experimenting with a 3-month free trial, some of that we said before. That is something that we could have never done if we didn’t have a year like this one because in a 3-month free trial, what happens is that your bookings get delayed by a whole quarter.

In other words, the only reason Duolingo can run a 3-month free trial experiment is precisely that they gave themselves the cover of a “foundational year.” If you’re operating with 25% bookings growth expectations, you can’t take a quarter of bookings and shove it forward by 90 days to see if it improves long-term LTV. You can do that with 10-12% bookings growth, and shareholders are pre-warned that this is what investment looks like.

So that’s why those slow growth projections for bookings in 2026 make sense. Maybe the company will see that it doesn’t work, but at least they will have the data to know. And if it works, it’s the foundation for growing the business for years to come.

There are also the “softer” monetization levers in the pipeline that mobile gaming has used for over two decades. Think of avatars, for example. Luis von Ahn:

Very soon, you’ll see really cool avatar costumes that’s directly coming from mobile games. I think users are going to love that. We’re doing a number of changes in terms of how we show rewards to users. I mean, for example, we’re showing them as cards now, and that feels really collectible. So we’re doing things like that.

He then pointed out that he’s currently dressed as a hot dog on the app, which is the kind of detail that makes me believe Duolingo will not lose its weirdness in pursuit of becoming a more serious product.

Buybacks

Quick capital allocation update. Through May 1, Duolingo has bought back approximately $50.6M, or about 514,000 shares. Gilian Munson framed it nicely:

This represents more than 100% of our 2025 net dilution from equity awards.

That’s worth focusing on, because the SBC argument was a fair criticism in 2024 and 2025 (and I made it myself). The buyback at current prices isn’t enough to fully neutralize 2026 dilution yet. The company is still guiding fully diluted share count to grow 3.5-4% before buyback effects, with SBC at nearly 15% of revenue. So I won’t pretend dilution is solved. But the direction of this is right, and at the current price, stock buybacks are a good choice, as the company has a very strong balance sheet.

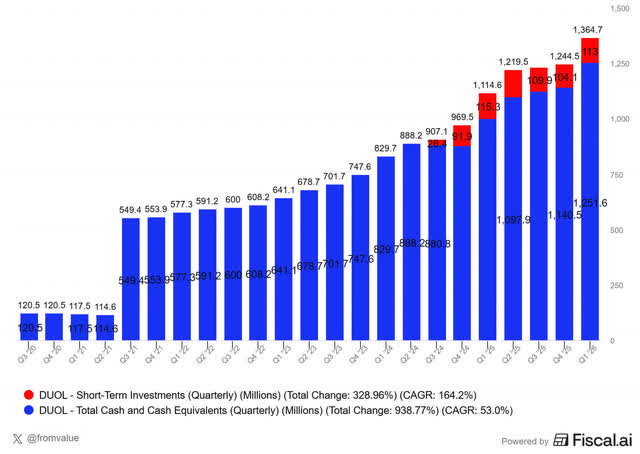

The company ended Q1 with $1.25B in cash, $1.36 billion if you add short-term investments and no debt.

That’s a very strong balance sheet. And with the FCF the company generates, it can pay for growth initiatives, fund the $400M buyback authorization, and still end the year with about the same level of cash as they started with. That’s a pretty rare combination, especially for a company with a market cap of just $5B.

What’s Disappointing (And What’s Not)

Q2 bookings growth of 5.8% guidance (4.1% constant currency) is the kind of number that would make me nervous if I didn’t understand why. There are a few reasons. First, the Q2 2025 comp was unusually strong because of the Energy rollout, a price increase, and exceptional ad performance. CFO Gilian Munson said bookings should accelerate by about 3 points in Q3 and rise further in Q4. Fine. But “trust us, it accelerates later” is a story the market usually doesn’t like and doesn’t trust. I have faith in management, but this is a big part of the reason why the stock is down so much. I would not call it a disappointment because of the context I explained but I understand it could be perceived as such.

In-App Purchase revenue and Duolingo English Test revenue both declined YoY (-11% and -6% respectively). These are small contributors to Duolingo’s revenue, but they’re not encouraging. Worth keeping an eye on.

MAU growth is flat. Luis von Ahn admitted it. He’s working on it. But this is the metric that would tell us whether the strategy is actually working at the top of the funnel, and so far it’s not telling us anything yet. Von Ahn said he doesn’t focus on it, but he should (and will, I think) from now on.

The U.S. is growing slowly. Luis von Ahn admitted that DAU growth in the U.S. is “very low” compared to other regions. Asia is carrying the growth right now. International DAU growth is great, but the U.S. is the highest-monetization market, and it would be nice to see it reaccelerate.

What I don’t think is disappointing: gross margin guided down to 69% by Q4. The bear take here is “margins are crashing.” The right take is “they’re putting more AI into the product on purpose because users love it, and the unit economics of AI are actually improving fast enough that they keep choosing to spend on more features rather than just pocket the savings.” CFO Gilian Munson explained this dynamic well:

There are always these waves of efficiency that come with AI. So you might have AI costs come up and then the team optimizes and then you move forward… So if you look, for example, at the Q1 gross margin, it was better than we would have expected and pretty good on a year-over-year basis. And yet there’s still a lot of new AI content in our product. And that’s because on a per unit basis, the costs have come down a lot.

Q1 gross margin actually came in better than where Q4 margin will land. So the trajectory toward 69% isn’t a margin collapse — it’s a deliberate reinvestment of AI cost savings into more AI features.

The Bottom Line

Q1 2026 didn’t move the stock much and I think that may go on for a while. 2026 is a transition year for Duolingo.

But what Q1 told us, in the data, is that Duolingo is still a very strong company. Let me summarize the strengths from this quarter:

Subscription revenue grew 31%.

Gross margin expanded despite AI investment.

Free cash flow margin went over 50%.

The DAU/MAU ratio went up again.

Content velocity went up roughly 3x.

Speaking is now core, mastery checks are live, personalization is starting.

Buybacks have already neutralized 2025 dilution.

China is accelerating and monetizing like France.

Performance marketing infrastructure is finally being built.

The free trial experiments are showing they can lift revenue without hurting DAU growth.

None of this guarantees that the strategy will work, of course. There are few certainties in the stock market and especially not about the future. Two years from now we’ll know whether Duolingo took the right steps. Right now, we can only guess and that’s what makes the market so uncertain about this company. As I said in my Selling Rules last quarter, the proof is in Q3 and Q4 of this year and beyond.

Many investors say they can hold through uncertainty. But if the stock is down 80%+ and there is uncertainty (the chicken and egg problem), they usually fall into pessimism. And I understand that.

But for me, I see a management with a great track record and a credible plan for the future. There’s still a lot of potential left and the general story up to (AI will kill it) doesn’t show up up to now.

What’s for sure is that the stock is much cheaper right now. So, does that make it a buy? We will look at the Quality Score and Valuation to answer that question.

But first: the Selling Rules!

Selling Rules

It’s now more important than ever to follow up Duolingo, to know whether it’s just talking or executing. Focusing on the long term is what we want as long-term investors, but sometimes, companies use it to hide weaknesses. I don’t have that feeling for Duolingo but a feeling is not enough. Hard data matter and that’s why I made the selling rules.

Do you want to see if Duolingo is a BUY? Become a paying member of Potential Multibaggers!

(If you already are, just scroll past this)

What do you get as a member?

✍️ Multiple high-quality articles per week

📚 Full access to our entire library of deep-insight articles

🔎 Full investment cases

📊 Access to the Private Community

🎥 Regular Webinars

📈 The Best Buys Now every month

✍️ The Overview Of The Week each Sunday

🔎 Deep earnings analysis

Many Multis say that the community alone is already worth the price, but you get so much more.

Go to this page.

Subscribe to the annual plan.