Hi Multis

I hope you don’t feel sick yet from the plunges in our picks. I’ve said this multiple times, but it feels like 2021 or early 2022. Our stocks have dropped hard and the indexes are still close to all-time highs, although the Nasdaq is also down 7.5% now.

During uptimes, Potential Multibaggers will do much better than the averages, but during downtimes, this strategy will dramatically underperform. That how it has always been and will remain.

As my investing horizon is far away (20+ years) I don’t mind the big volatility (up and down) too much, but I know that many of you have a different investing horizon or are more affected by the sudden price moves.

Duolingo (DUOL) is now down almost 82%.

And the Q4 results on February 26 added another drop to what was already a painful crash. The stock was down 20% in the after-hours, but recovered a bit. But with the general market, Duolingo’s stock keeps falling as well.

Let’s look at what’s going on here.

The Numbers

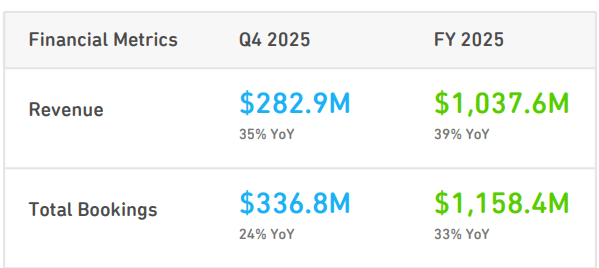

Let me first give you the Q4 numbers:

Q4 revenue: $282.9M, +35% YoY, beating estimates by $7M.

Non-GAAP gross margins: 72%, down about 1 percentage point YoY.

Adjusted EBITDA: $84.3M at a 29.8% margin. Strong.

Net income: $42M (but note: FY25 had a one-time non-cash tax benefit of $256M that inflated full-year net income substantially — exclude that noise).

Free cash flow: $93.7M for Q4, about a 33% margin. For the full year, free cash flow reached roughly $360M.

Of course, for a company like Duolingo, the engagement numbers are at least as important:

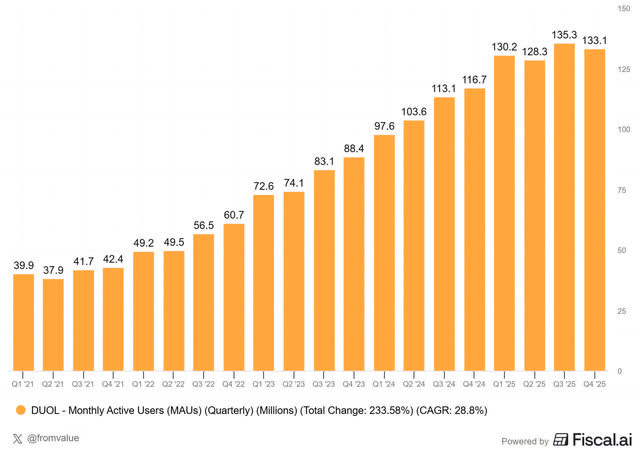

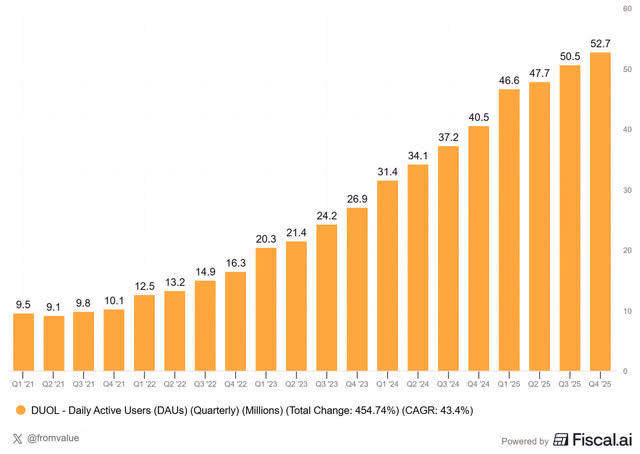

DAUs (daily active users): 52.7M, +30% YoY (vs. +36% in Q3).

MAUs (monthly active users): 133M, +14% YoY (vs. +20% in Q3).

Paid subscribers: 12.2M, +28% YoY (vs. +34% in Q3).

Paid subscriber penetration: 9.2% of MAUs, up from 8.1% a year ago.

We go deeper into the numbers further in this article.

But overall, I think we can say without hesitation that the Q4 numbers were good. Revenue up 35% with a beat, strong free cash flow, DAUs and Paid subs up strong and so on.

The full year was strong as well: revenue crossed $1 billion, up 39%. Duolingo has now delivered 23 consecutive quarters of 30%+ revenue growth. Only Mercado Libre (28 quarters) has a longer streak among all 83,000+ publicly traded companies worldwide.

So why did the stock tank again?

The Strategic Shift

A few factors explained the drop.

First, the 2026 guidance. The company guided for bookings growth of 10-12% and revenue growth of 15-18%.

I already want to point out that Duolingo’s management are experts in sandbagging. Last year, they guided for 25% bookings growth in 2025. This is the real result.

That’s a big difference and this is just one example. Management really has a history of sandbagging. But right now, the market doesn’t really seem to care about that, not even as a footnote.

The adjusted EBITDA margin is expected to be around 25%, down from 29.5% in 2025. For a company that just delivered 39% revenue growth and 30% EBITDA margins, this is a dramatic slowdown.

But no blaming the macro situation here. It’s a deliberate choice. CEO Luis von Ahn is deliberately sacrificing near-term profits to have 100 million daily active users by 2028. That would be a near-doubling from the current 52.7 million. His strategy is simple: grow the user base now, monetize it later.

Or in his own words:

Long-term value in this business is driven by 2 things: the size of our active learner base, that’s like the size of the pie. And how effectively we monetize that base. You can think of that as the piece of the pie that pays. At this moment, we are prioritizing growing the size of the pie.

There was a remarkable moment when von Ahn pulled out his IPO letter to shareholders, so the first one, and read it aloud during the call:

Dear potential investors, the main thing you need to know is that I plan to dedicate my life to building a future in which, through technology, every person on this planet has access to the best quality of education.

The message was clear. He wants to play the long-term game. At least, it’s very clear. You can agree or disagree with the strategy, but you can’t say that von Ahn is not clear or doesn’t follow his guiding star.

The Paradox: Overmonetized AND Undermonetized

One of the most insightful moments of the call was when Luis von Ahn described a seeming paradox. He was asked how the shift back to user growth eventually becomes a monetization strategy again. His answer was fantastic:

Look, we got ourselves into an interesting situation where both Duolingo is undermonetized and overmonetized at the same time. It’s undermonetized in that, look, only about 10% of our monthly active users pay us. We wholeheartedly believe we can do much better than that. If you look at comps, if you look at things like Spotify, half of their users are paying them, give or take. And a lot of these freemium businesses, we really think we can get much higher than 10%.

However, the way we were increasing monetization was we found that the quickest way to increase monetization was basically by adding friction. The more we added friction, the more we got people to subscribe. And that’s okay, but I think that we got it to a point where it really became at odds with DAU growth.

This is honest and straightforward in a way you rarely see in business. Management is admitting that they over-optimized for near-term monetization growth by adding friction to the free experience, and it came at the expense of user growth. The quick fix, like doubling ad loads, reducing energy, and adding more paywalls, was easy money, but it hurt the long-term prospects.

Now, if you only have 10% of users paying and Spotify has 50%, you don’t need me to say that the upside is big. But you need to find different ways to monetize. Luis mentioned in-app purchases (avatar customizations), direct ad sales, and pricing experiments. These take longer to build than just cranking up friction, but they don’t kill DAU growth.

The User Deceleration

Let’s address the elephant in the room: user growth. Look at MAUs (monthly average users).

As you can see, from the first quarter of 2025 to the fourth quarter, there has been no meaningful growth in MAUs and for the second quarter out of three, the number of MAUs was down compared to the previous quarter. That doesn’t look great and it only confirms what management said, that MAUs need attention urgently.

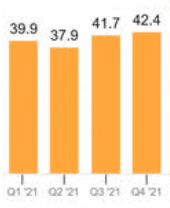

At the same time, I think there’s an overreaction to this. It’s not the first time this has happened. Look at 2021.

You see a similar pattern, though Q4 was still slightly above Q3. But Q4 growth compared to Q1 was just 6.3%. It’s even lower now, at 2.2%.

To me, it’s clear that focusing on MAUs is clearly the right thing to do for management.

DAU growth also decelerated throughout 2025, from 40%+ in Q2 to 36% in Q3 and 30% in Q4. Management now expects about 20% DAU growth throughout 2026.

Is this saturation? The market thinks it is, but Luis von Ahn disagrees:

In the United States, 2% of all Internet users on a given day use Duolingo. So 2% penetration in the U.S. for daily users. In the U.K., that’s 3%. In Germany, that’s 4%. And Germany is not the highest country we have. We actually think we can get much higher than that. But even if we only assume that every country got to 2%, which is the U.S. penetration, we would more than double our daily active users.

For context, daily usage penetration for platforms like Spotify and Netflix in established markets ranges from 30% to 50%. Duolingo is at 2-4%. Now, I don’t claim that the TAM is as big for Duolingo as for TV entertainment and music, but I’m convinced that it’s higher than this.

And the churn data backs this up. When Duolingo surveys users who stop using the app, the most common answer hasn’t changed in years: they got busy. Not “I switched to ChatGPT“ or “I use Google Translate now.” They got busy, which, as Luis von Ahn candidly admits, basically means they’re scrolling social media instead.

I have mentioned this multiple times. I have a Duolingo streak of 1,500 days (today, yes) and it took away time from my social media scrolling. Since I use Duolingo, I almost never use Instagram anymore. Only when someone sends me a link.

On top of that, 40% of monthly active users are also the daily active users, which I still find very impressive and shows the power of the platform.

The AI “Threat” (Again)

Every earnings call, someone asks about AI disruption. And every time, the answer is the same, because the facts are the same.

Luis von Ahn:

AI translation has been essentially perfect among the large languages for like more than 10 years. I mean between Spanish and English, it’s essentially been perfect. Our users use Duolingo for 2 main reasons: one, as a hobby, they actually want to learn. And those people, whether there’s AI translation, it doesn’t matter, it’s a hobby for them. And then the other group of people is learning English. They want to learn English, and they actually want to learn English.

I’ve been saying consistently for months now. Of course, if the stock price drops, then the stories come. And the AI story is just that, a story.

Even more importantly, the data support this.

Retention remains healthy (about flat) and in the cohorts.

Paid subscriber growth was 28% in Q4.

The DAU/MAU ratio hit an all-time high of about 40% in 2025, as I pointed out.

Marketing spend as a percentage of revenue stayed stable at around 12%, so growth is not driven by excessive marketing spending. If AI were meaningfully disrupting Duolingo, you’d see it in churn, engagement, or acquisition efficiency but the numbers are clear.

Do you think these things would happen if AI were killing Duolingo? Sure, I know what some think now: “It could happen.” Who knows, but I don’t pay much attention to stories without data to back them up.

I’ll put it differently: how many people do you know who have been learning a language through an LLM and have been doing so consistently for months? I know zero, while I know multiple people using Duolingo. How about you?

As for the “vibe-coding” threat, so someone building a Duolingo clone with ChatGPT or another LLM, Luis von Ahn put it best:

If I were to write down just the spec of Duolingo, just... and I’m not talking about recreating it in a programming language, like write it down in English, it would take me years because there are 1 million corner cases of things that we do that we’re really smart about.

And even if someone builds a decent clone, they still face Duolingo’s free product as their main competitor. Over 15 years, hundreds of apps have tried. Duolingo still holds roughly 85% of all language learning app DAUs worldwide. That number hasn’t changed. Not before and not now with LLMs.

So, can we please finally stop with this nonsense story? Of course, I’ll keep an eye on it because things can change quickly in tech. But so far, it’s a BS story.

Product Updates

There were a few interesting product updates.

First, the decision to move Video Call with Lily, Duolingo’s flagship AI conversation feature, from the $168/year Max tier down to the $84/year Super tier is one of the most interesting decisions in this whole strategy.

It’s not a defensive move, as Max retention numbers are “actually quite good.” Luis von Ahn was clear about this:

None of the Max numbers are making us do anything with video call. The Max numbers are actually quite good. We’re happy with the Max numbers. We are taking, what I call, an offensive move with Max.

I just believe that the cost of video call has gone down enough. It just kind of doesn’t make sense for us to just have it in Max when we can offer it in much cheaper packages.

There are about 10x as many Super subscribers as Max subscribers. If you put Video Call in Super, 10x more people get access to conversational practice and I’m sure this will boost engagement.

The data also backs this up. Users who engage with Video Call become promoters: they post online about how they’re shocked they can actually hold a conversation after using Duolingo for a while, and they tell their friends and family.

Of course, there’s a risk that this can cannibalize Max subscriptions and management knows that. That’s why it’s being A/B tested, like almost everything at Duolingo. If the data shows terrible Max cannibalization, they’ll restrict the feature, maybe one video call per day on Super, unlimited on Max. But they want to do this now, from a position of strength, rather than being forced into it later by a competitor.

As Luis von Ahn put it:

We’re going to do this on our own terms... at the moment, we really are not worried about competition. So we’re getting ahead of it.

Something that might get lost in the guidance drama: chess has reached 7 million daily active users in less than a year. Duolingo is now the second-largest chess platform in the world, after chess(.)com.

But if you search for “chess” on the App Store, Duolingo doesn’t even appear in the results. They haven’t done any App Store optimization for it yet. Those seven million DAUs (of which I am one) all come from essentially zero dedicated marketing.

Of course, many Duolingo language users are doubling up with chess. Luis von Ahn acknowledged that the majority are. Languages are still growing at roughly the same pace. But over time, more people are discovering Duolingo through chess, and that standalone user base is building. The cross-pollination works both ways, and users who study multiple subjects show higher retention.

If chess is the quiet blockbuster, math is the sleeping giant. There are roughly 1 billion people learning math worldwide. That’s a market almost as large as the language-learning market. The difference, as Luis von Ahn said, is that most of those people don’t want to learn math. They’re in school and have to.

But he thinks Duolingo can change that:

I believe that this year, we’re going to have the best tutor app for math.

Rather than pursuing school district deals, which are complex, slow, politically tricky, and expensive, management wants to position Duolingo Math as a supplemental tool, a bit like a competitor to Kumon. There’s a large market of parents already paying for outside help. And, as Luis von Ahn pointed out, the willingness to pay (from parents, not kids) is very high for math. I think we all know this. So, math could become a real revenue growth driver in the future.

New CFO & Buyback

Matt Skaruppa, Duolingo’s CFO since the IPO, has moved on. His replacement is Gilian Munson, who joined Duolingo’s Board years ago and chaired the Audit Committee. She’d been on the job for only 3.5 days at the time of the earnings call and delivered what was honestly an impressively detailed walkthrough of the guidance.

The best moment was how she presented the two paths Duolingo could walk:

We could have grown the business, probably we would be at about a mid-teens CAGR over the next couple of years. If we could keep our margins where they are, we’re probably looking at a $1.5 billion business, $400-plus million in adjusted EBITDA. But we, at the company, are really motivated to go for the bigger prize.

(...)

If we can get to that DAU and even reasonable monetization assumptions from where we are today, and we believe we can scale our expenses over time, you’re looking at a business in a couple of years, it could be $2.5 billion with over $700 million in adjusted EBITDA.

So: the safe path is a $1.5B revenue, $400M EBITDA business. The ambitious path, which requires hitting 100M DAUs, is $2.5B in revenue and $700M+ in EBITDA. Management is going for the ambitious path and I like that. It’s something I have seen from multibaggers in the past. Of course, we don’t know whether they will hit their target, but setting it is, in itself, what I like.

The Board also authorized a $400M share buyback. With the stock down 80%+ from its 2025 highs, that’s significant. Duolingo has the cash ($1B+) and the free cash flow ($350M guided for 2026) to fund both growth and buybacks. So, good decision at this price.

What Could Go Wrong

I read everything bearish I could, to know the bear case very well. There’s a lot of misinformation out there, like people saying AI is clearly eating Duolingo’s cake. But it’s too easy to just dismiss everything. My main takeaway of my bear research was that there’s much more uncertainty now. I agree there. The bookings guidance of 10% to 12% may imply that revenue growth falls to that pace in 2027, unless management can really accelerate the MAUs growth.

As we all know, markets hate uncertainty and opportunity costs. Most “investors” are no investors but traders in disguise. If you think like a business owner, you would think it’s a good decision to choose for the long term, not the short term.

Second, the 100M DAU target by 2028 implies accelerating from 20% growth to significantly higher levels in 2027 and 2028. That’s not easy. If DAU growth doesn’t reaccelerate or worse, if it keeps decelerating, it would suggest the issues aren’t just about overmonetization but about saturation, or engagement fatigue. That’s why I used this for my Selling Rules. More about that later in this article, of course.

I also want to use my knowledge of past losers to assess Duolingo. I have an article here that is called The Wall of Shame, where I look at my past losers to learn one or more lessons from each one of them. Duolingo doesn’t seem to fit into one of the patterns so far. More in the Selling Rules.

Conclusion

Duolingo has built one of the most impressive consumer apps in the world. Five years of 30%+ revenue growth in every single quarter, gross margins above 70%, free cash flow margins above 30%, a strong balance sheet and a founder-CEO who clearly thinks in years and even decades, not quarters. And don’t forget that Duolingo has a product that more than 50 million people use every single day.

The 2026 guidance is disappointing in isolation, but I think it’s essential to understand why the numbers look the way they do. The company decided to build a much larger business. The parallel with Spotify’s 2022-2023 investment phase (before its massive stock rerating) is worth thinking about.

New CFO Gilian Munson described 2026 as “a foundational year.” That’s the right framing. This year will be messy in the financial models and most “investors” don’t have the patience and equanimity to endure such a year. I’m fully aware that this could take more than one year.

So, if you are not prepared for your investment to pay off, I can understand that you want out. But if management executes, so if MAU/DAU growth reaccelerates, if math and chess become meaningful growth engines, if new monetization methods offset the friction reductions, the business could become quite a bit larger and stronger.

I’m not going to pretend that I won’t have my moments of doubt. After all, management can have plans, but there are no guarantees that they will work or become a reality. That feels uncomfortable.

But if you look at the track record of Luis von Ahn and Duolingo, I can’t help but give him the opportunity to prove he will execute as he has planned.

On to the Selling Rules, the PM Quality Score update and the valuation, to decide if this is a stock to add to or to dump.

Selling Rules

It’s now more important than ever to follow up Duolingo, to know whether it’s just talking or executing. Focusing on the long term is what we want as long-term investors, but sometimes, companies use it to hide weaknesses. I don’t have that feeling for Duolingo but a feeling is not enough. Hard data matter and that’s why I made these selling rules.

Do you want to see if Duolingo is a BUY? Become a paying member of Potential Multibaggers!

(If you already are, just scroll past this)

What do you get as a member?

✍️ Multiple high-quality articles per week

📚 Full access to our entire library of deep-insight articles

🔎 Full investment cases

📊 Access to the Private Community

🎥 Regular Webinars

📈 The Best Buys Now every month

✍️ The Overview Of The Week each Sunday

🔎 Deep earnings analysis

Many Multis say that the community alone is already worth the price, but you get so much more.

Go to this page.

Subscribe to the annual plan.