If you’re going to do anything new or innovative, you have to be willing to be misunderstood. If you cannot afford to be misunderstood, then for goodness’ sake, don’t do anything new or innovative.

Jeff Bezos, interview with Mathias Döpfner, 2018

Hi Multis

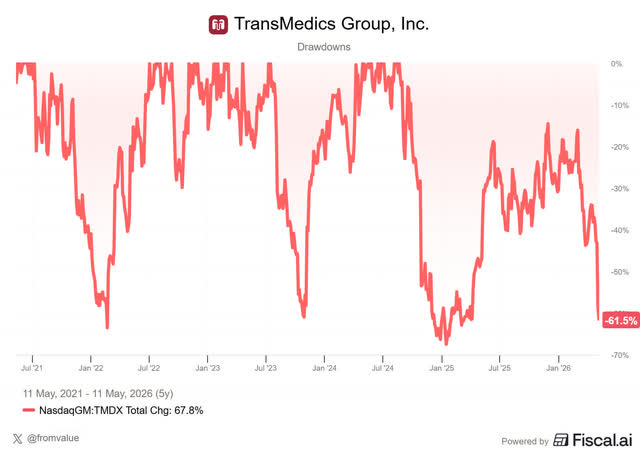

You could already read it in the Overview Of The Week, TransMedics’ (TMDX) stock dropped by about 39% in the last two weeks. Most of that came after Q1 2026 earnings on May 5.

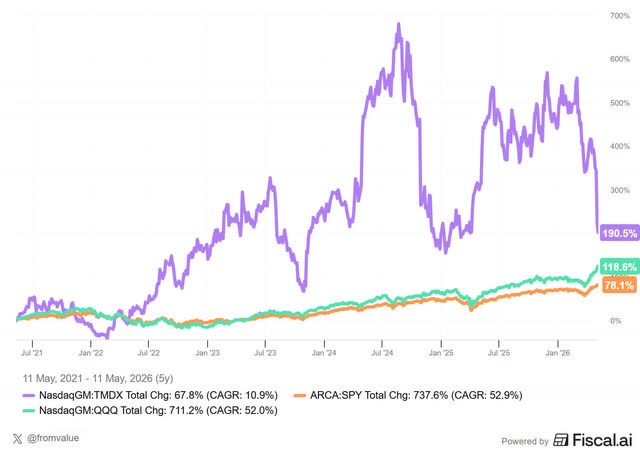

This is the 4th time in 5 years that TransMedics is down more than 60%. So, like a real Potential Multibagger, this is a very volatile stock. Despite the big drop now, it still outperforms the S&P 500 and Nasdaq over the same period.

So, why did the stock drop so much and is the thesis intact or not? Let’s dive in.

The Numbers

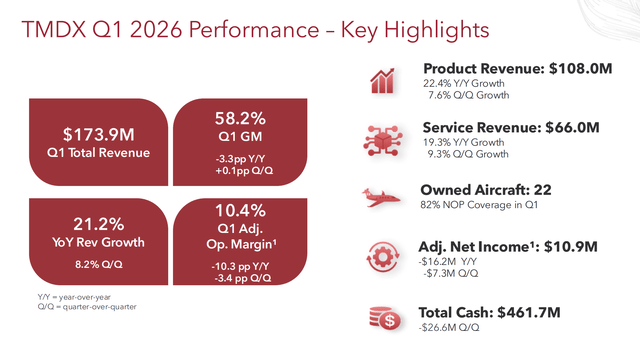

These are the results TransMedics posted in Q1 2026:

Revenue: $173.9 million, +21.2% YoY, +8.2% QoQ. That’s a slight miss of about $128K versus the consensus, so basically in line.

Adjusted EPS: $0.30, missing consensus of $0.62 by 52%. Down 59% YoY from $0.74.

GAAP EPS: $0.20 versus $0.70 a year ago. Down 71%.

Gross margin: 58.2%, down 3.3pp YoY from 61.5%, but up 1pp QoQ.

Adjusted operating margin: 10.4%, down 10.3pp YoY from 20.7% and down 3.4pp from Q4 2025.

Adjusted operating income: $18.1 million, down 39% YoY from $29.8 million.

Guidance: $727-757M for 2026, 20-25% growth. Reiterated, not raised.

TransMedics summarizes it in their earnings call slide deck.

Revenue growth is not great, but OK and I think the market dumped the stock for everything below revenue. Margins were awful and the reason is simple. Adjusted R&D was up 45%, adjusted SG&A up 41%, adjusted total operating expenses up 42.1% versus revenue growth of 21%. So, costs grew about twice as fast as revenue. That’s the opposite of operating leverage.

Is This A Broken Thesis, Or An Investment Phase?

This is the real question, of course. Let me give the bearish argument first. Margin compression of this magnitude, with management refusing to provide specifics (”I’d rather not go into those levels of detail now“ - Gerardo Hernandez, CFO), could suggest that TransMedics doesn’t know exactly what it’s doing. Or, put differently, that the company does not have control over its own model. The CFO did say to expect the adjusted operating margin to be “up to around 250 basis points below“ 2025 levels.

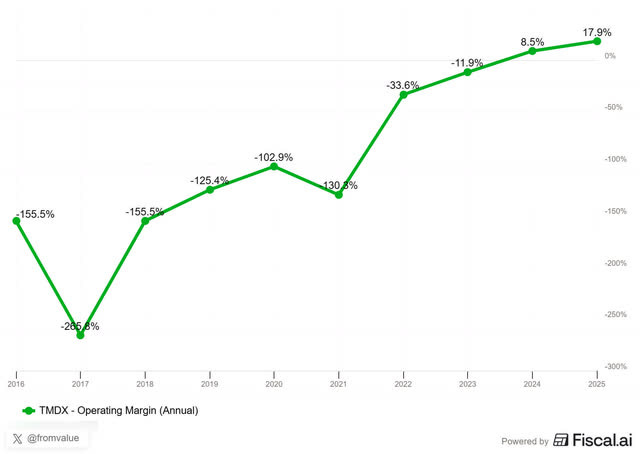

The FY2025 adjusted operating margin last year was 17.9%. If you subtract 250 bps, you get roughly 15.5% for the year. Q1 came in at 10.4%. But compare this to previous years. It’s not that this is a setback to the stone age for the company.

And to be honest, I don’t see much more for the bear case. Yes, margins will be under pressure this year, but it’s a deliberate choice. Founder and CEO Waleed Hassanein opened the call confirming this:

Specifically, I want to highlight that this is a strategic and proactive decision, and we fully expect that our financial performance over the next several quarters will reflect these necessary investments in people, infrastructure and technology development as we capitalize on the opportunities in front of us.

In other words: yes, the margins will be lower for a while but this is on purpose and the company knows what it’s doing. You can either trust that or not. To help with that judgment, you have to look at what they’re actually spending on.

Five Investments

There are four growth initiatives and another investment running at the same time right now. And that’s why costs are up so much, twice as much as revenue. Let’s look at them one by one.

If you want to read the rest of this article and all others, upgrade to a paid subscription now!