Hi Multis

Some weeks ago, Topicus (TOI.V) (TOITF) reported its Q4 and FY 2025 results and this is a deep dive into those earnings and the potential AI impact on the company.

As you probably know, I have a second service called Best Anchor Stocks, which is run by Leandro. He is also a Topicus stockholder and wrote an earnings analysis for Best Anchor Stocks subscribers. I used that as a basis for this article, but I added context, commentary, and my takes. Of course, as always, I will update the Selling Rules, the Quality Score and the valuation.

Right now, the stock is down more than 50% from its all-time high, set not even a year ago.

Is that warranted or not? Let’s find out.

The Numbers

Topicus grew its revenue 20% year-over-year in both Q4 and the full year. Q4 revenue came in at €436.8 million, up from €364.9 million. Full year revenue came in at €1,552.3 million (or about $1.8B), up from €1,294.9 million. Not bad for a “small” European software compounder that most people haven’t even heard of.

Organic growth was 4% for both periods, with maintenance and other recurring organic growth at 6%. Now, 4% organic growth doesn’t make you jump out of your chair. But 6% on the recurring side, the revenue that’s sticky and predictable, is actually quite decent for a serial acquirer that constantly buys companies with sometimes flat but mostly declining organic growth. Remember, the Constellation/Topicus playbook is to buy cheap, stabilize, and slowly get that organic revenue moving upward. The 6% recurring organic growth tells you the existing portfolio is healthy.

What most people miss here is the composition of that revenue. Maintenance and other recurring revenue hit €1.097 for the full year, up from €900 million in 2024. That’s a 22% increase and represents about 71% of total revenue. This is the core of the business. This revenue stream is highly predictable, sticky revenue and margins are high.

Professional services came in at €372 million (up 14%), while hardware and other revenue jumped to €39 million from €25 million, a 59% increase that likely reflects some of the acquired businesses. But overall, it’s just 2.5% of revenue.

One of the problems with Topicus is that the numbers are not easy to read and that was the case again with these earnings. The headline earnings look terrible if you take them at face value. Net income dropped 53% for the full year, from €149.5 million to €70.1 million. On a per share basis, diluted EPS fell from €1.11 to €0.50. If this is all you look at, you’d think the company is under pressure. But it’s not.

The full-year net income decline is almost entirely driven by a €221.7 million non-cash (!) expense related to the Asseco Poland investment. When Topicus elected to record this investment at cost under the equity method of accounting, it triggered this one-time charge. It’s accounting noise, not operational problems. On top of that, the company also recorded €119.7 million in income from derivatives, fair value adjustments, and a dilution gain tied to Asseco. So, even within the Asseco-related items, it’s a messy picture that tells you essentially nothing about how the actual business is performing.

This is why you need to look at cash flows. And the cash flows are singing a beautiful song.

Operating cash flow grew 19% for the full year to €412.7 million, up from €347.6 million. In Q4 alone, CFO jumped 35% to €107.7 million.

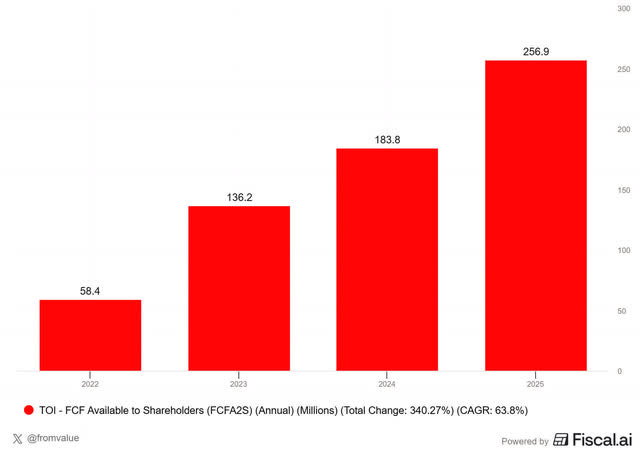

The metric that matters most for Topicus is free cash flow available to shareholders, or FCFA2S. In short, FCFA2S is the cash flow Topicus would generate for its shareholders if it stopped doing acquisitions, after stripping out all the money that goes to minority partners and Constellation Software, the parent company.

FCFA2S grew 23% to €218.7 million for the year.

In Q4, FCFA2S was up 40% to €51.2 million. One thing I appreciate about Topicus versus Constellation is that FCFA2S is actually a clean number here. There’s no IRGA (intergroup revolving account) muddying the waters, which makes Topicus’ cash flow a much more transparent measure of what shareholders are actually earning.

Digging into the FCFA2S numbers, a few things stand out. Interest paid on other facilities nearly doubled from €5.7 million to €13.0 million in Q4, and went from €21.1 million to €24.9 million for the year. Not very high on the total, but it reflects the higher debt load from the Asseco stake and, of course, other acquisitions.

Lease obligations also grew meaningfully: from €24.6 million to €30.1 million for the year. This tells you the acquired businesses come with real physical footprints.

But the most important takeaway is that despite these increased costs, the FCFA2S still grew 23%. That’s strong.

Topicus now also receives interest and dividends from its Asseco stake. This contributed €9.5 million in 2025 and €1.4 million in Q4 alone. It’s a small but new source of cash flow that will recur and probably grow over time.

Record Capital Deployment

This is where the quarter and the year get really exciting. 2025 was by far the strongest year on record for Topicus in terms of capital deployment, and it wasn’t even close.

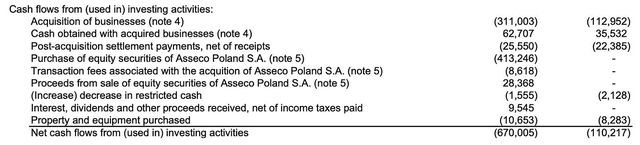

Between Asseco and other acquisitions, Topicus deployed €662 million of capital (net of cash acquired) during 2025. To put that in perspective, last year the number was €77 million. The year before that, €199 million. This was a big shift.

Now, a huge chunk of this was the Asseco Poland investment (€384.9 million net). But even excluding Asseco, the company completed acquisitions for total consideration of €390.4 million (including holdbacks and contingent consideration). The net cash spent on non-Asseco acquisitions was €248.3 million (€311 million in acquisitions minus €62.7 million in cash obtained with those businesses). That’s still an all-time record for Topicus.

What’s important here is that this capital deployment was roughly 3 times the full-year FCFA2S. In other words, Topicus deployed significantly more than it earned. How? By leveraging. That’s only good as long as the leverage stays manageable. And it does.

Topicus ended the year with €326.7 million in cash and total debt of €692.5 million (split between €345.3 million in revolving credit facility/current term loans and €347.2 million in non-current term and other loans). That puts net debt at roughly €366 million.

That’s a leverage ratio of about 0.9x operating cash flow. For any normal company, that’s very conservative and that also goes for a serial acquirer.

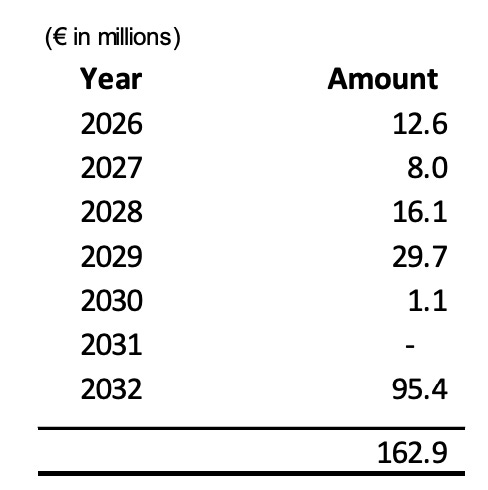

I also want to highlight the maturity structure: the non-current term loans of €347.2 million don’t come due until at least 2032.

That’s crucial because it means Topicus can continue using debt as fuel for acquisitions without worrying about near-term refinancing.

The balance sheet also reveals the scale of change this year. Total assets grew from €1.54 billion to €2.51 billion — a 63% increase in a single year. Intangible assets (the acquired software) went from €951 million to €1.20 billion. The investment in equity method associates (Asseco) is now €515 million, up from just €2.5 million. This shows that the company completely transformed in 2025.

And there’s still plenty of dry powder. Topicus has room under its revolving credit facility, generates over €400 million in annual operating cash flow, and has debt maturities far out. This is a company that could keep deploying capital aggressively if the opportunities are there.

The environment looks favorable for deals. Private equity distributions grew meaningfully in 2025, but these were concentrated in large deals. The mid-market, where Topicus hunts, remains stagnant. PE holding periods have stretched, and limited partners are pressuring funds for returns. That’s the kind of environment where a disciplined buyer like Topicus can find deals at attractive prices.

You should know that right now many VMS companies are somewhat in panic. They don’t want or can’t adapt to the new AI wave. They see valuations crumble and that’s when they are more ready than ever to sell. With so much flexibility left, Topicus can seize the moment for some attractive acquisitions.

Of course, capital deployment is always lumpy for a company like this. Remember that just two years ago, Topicus was being criticized for paying a special dividend because it couldn’t find enough deals. How the tables have turned.

AI Disruption? Look At These 3 Numbers

Let’s address the (supposed?) elephant in the room. A significant part of Topicus’ drawdown from its all-time high is tied to the broader AI fear sweeping through the software industry. The narrative is that AI-native tools will replace vertical market software. I’ve written extensively about why I think this fear is overblown for a company like Topicus, but let’s look at what the actual numbers tell us.

First, organic growth. Maintenance and recurring organic growth of 6% doesn’t scream “being disrupted by AI.” It’s right in line with the historical trend. If AI were eating Topicus’ lunch, you’d expect to see churn accelerating and organic growth collapsing. We’re not seeing that. Not yet, anyway.

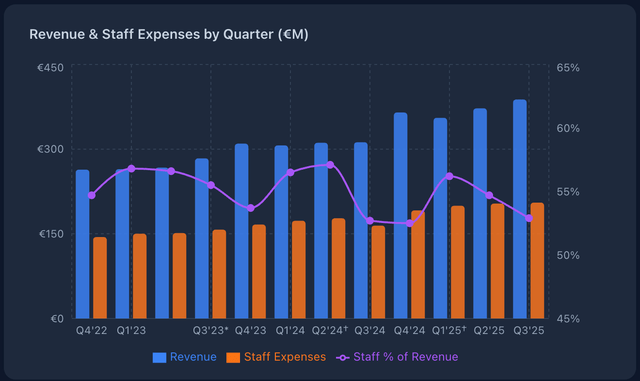

Second: staff expenses as a percentage of revenue actually decreased in 2025.

For the full year, staff costs were €835 million on €1,552 million in revenue, or about 53.8%. In Q4 specifically, this ratio dropped even further to around 52%. And this happened during a year of massive capital deployment, where newly acquired businesses typically come with a bunch of employees and usually drag efficiency down.

Within staff expenses, R&D spending grew considerably faster than overall staff costs. That’s the exact pattern you’d want to see in an AI world: the company is getting more efficient on the operational side while investing more in product development. One quarter doesn’t make a trend, but it’s a data point worth tracking closely.

Third, contingent considerations grew in 2025, while impairments slightly decreased. Contingent considerations are extra payments that the sellers of an acquired company can get if the company reaches certain milestones. An impairment is a write-down of an asset (like goodwill or an investment) when its value has dropped below what you paid for it. It’s an accounting recognition that you overpaid or the asset lost value.

If AI were destroying Topicus’ portfolio, you’d expect to see the opposite: acquired companies missing their milestones, resulting in lower contingent considerations and more impairments showing up. This is another indicator that the acquired businesses are performing in line or better than expected.

Now, I don’t want to be dismissive of the AI risk. It’s real, and it’s uncertain. But there are several structural reasons why I think Topicus is better positioned than most:

The switching costs in vertical market software go far beyond price. I’ve given the example before of a clerk in a Belgian municipality who’s been using Cipal Schaubroeck for twenty years. You’re not ripping that out because some kid built something with Claude. The compliance requirements, the security concerns, the retraining costs, the risk of downtime and so much more parameters protect the VMS software.

Topicus is heavily exposed to Europe and to government entities. These are among the most conservative buyers of software on the planet. As Asseco recently noted, customers in their space are reluctant to even store data outside of Europe or use the hyperscalers. That’s a structural tailwind for an entrenched European VMS player.

And perhaps most importantly: Topicus is not just a software company. It’s a capital allocator. If the VMS landscape changes because of AI, Topicus can pivot its capital allocation to wherever the returns are best. The compounding machine doesn’t depend on any single piece of software but on the discipline of buying great businesses at good prices.

Conclusion

2025 was a good year for Topicus. The company crossed €1.5 billion in revenue for the first time, deployed a record €662 million in capital, grew FCFA2S by 23%. Still, the stock price is down by more than 50%. The AI narrative has created fear, and the Mark Leonard succession story at Constellation has added uncertainty, even though Topicus has been operating independently under Robin van Poelje for years now.

The business is performing. The capital allocation is performing. The balance sheet is in good shape with room to keep going. That’s all I needed to know to know that the sell-off is, so far, only based on sentiment and stories, not the data.

So, on to the Selling Rules, the Quality Score and the valuation to know if Topicus is a buy.

The Selling Rules

I made Selling Rules for Topicus. Here they are.

Let me go over them one by one.

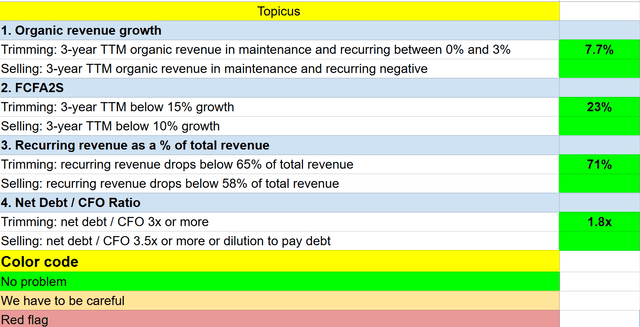

1. Organic revenue growth

You want to see organic revenue growth. Topicus buys businesses with low, no or even negative revenue growth. That’s why they are much cheaper. But the company optimizes those businesses to see revenue growth again, especially recurring revenue.

At the same time, I want to look at the 3-year trailing twelve months, not just the quarter or the year. The reason is that if Topicus does a big acquisition one day, it will need time to turn that business around. And there’s another reason to do this. Let me explain that with the numbers of this year.

Organic growth was 4% in both Q4 2025 and full-year 2025, but over the last three years it was 7.7%. So, you might conclude that organic growth was weaker in 2025, but that is not necessarily the case. In 2025, Topicus had record capital deployment. If you acquire more businesses, organic revenue will be lower that year because the new businesses have more influence on the total. Conversely, if the company deploys less capital, organic revenue will be higher.

2. FCFA2S

Free Cash Flow Available To Shareholders is a temperature check for how well the business compounds. I’m very happy that Topicus reports it, as it shows the fundamentals. If the company acquires well, FCFA2S will grow at a good pace.

So, why 15% and 10%?

FCFA2S shows what the business would do without acquisitions and accounting necessities. If growth is under 15%, it means that the business is decelerating in revenue growth or that the company’s acquisitions are of poorer quality.

Under 10% growth, the thesis would be broken.

Again, this is not something you want to look at on a yearly basis, let alone quarterly. Acquisitions are made when they are attractive. Once the company would start doing them just because, it would be a red flag. The lower quality would then also be visible in FCFA2S.

3. Recurring revenue as a % of total revenue

Recurring revenue was €1.097B in 2025, 71% of total revenue. This is the structural health metric for VMS businesses. The entire Constellation/Topicus model depends on sticky, recurring revenue.

If recurring revenue as a percentage of total declines, it means either: Topicus is acquiring lower-quality businesses (more project/services revenue), or its businesses see churn in recurring contracts. Both signal a deterioration of the business.

A drop to 65% recurring revenue, therefore, would signal more services-heavy businesses, which have worse economics: lower margins, less predictable, and lower switching costs. Below 58% fundamentally changes the character of the portfolio from recurring revenue to consulting/services, and then Topicus is simply another story, and the thesis is broken.

4. Net Debt / CFO Ratio

Net debt was €742.4M at the end of 2025, and cash from operations came in at €412.7M. That means a net debt/ CFO ratio of 1.8x. This is conservative for a serial acquirer but it is significantly higher than the previous years.

Constellation Software has never taken more than 2x in debt, but Mark Leonard also said that this may change because of certain circumstances.

So, a higher ratio would not be a red flag immediately, but of course, too much is too much. If the ratio were 3x, I’d trim because of the higher risk. Ät 3.5x, I’d sell, because it would totally change the dynamics. The same goes for issuing shares to pay debt. That would undercut the whole model. This is not about issuing shares if it’s an offensive move. In other words, if Topicus sees more opportunities than it has money and it is convinced this will be temporary, it’s OK to raise some money. But if it’s to pay off debt, that’s a red flag to me.

If you are not a paid member, this is where it stops for you. If you want to learn about Topicus’ Quality Score and my current valuation, you can try out Potential Multibaggers for 7 days. You can unsubscribe in the first 7 days with just a few clicks.

Don’t wait! Try it out now!