Hi Multis

A few weeks ago, Topicus (TOI:CA) (TOITF) reported its Q1 2026 results. I started the earnings analysis last week, but I couldn't get it out and so, I'm finishing it on the plane on my way to Vail, Colorado.

As you probably know, I have a second service called Best Anchor Stocks, mostly run by Leandro. He is a Topicus shareholder and wrote a short earnings analysis for Best Anchor Stocks subscribers. This article took Leandro’s article as a basis, but I added some context, a different angle here and there, and a couple of extra things from the filings.

And as always, I’ll update the Selling Rules, the Quality Score and the valuation at the end.

The Numbers

Topicus grew revenue 23% year-over-year to €435.7 million, up from €355.6 million. This acceleration came with EBITA margin expansion, as expenses grew less than revenue, at 20% YoY.

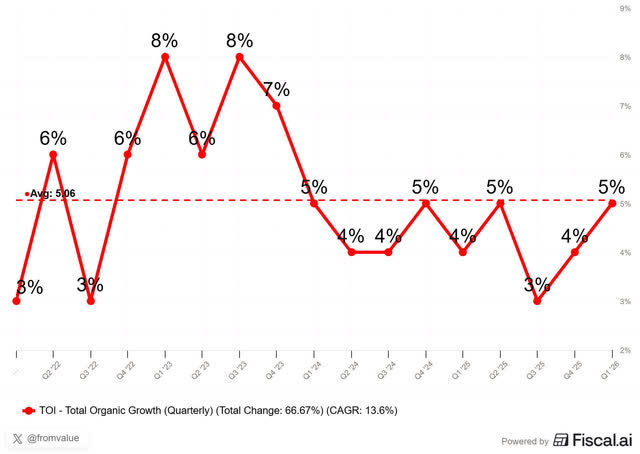

Organic growth (growth that doesn’t come from acquisitions) was 5%, the average since Topicus became a public company.

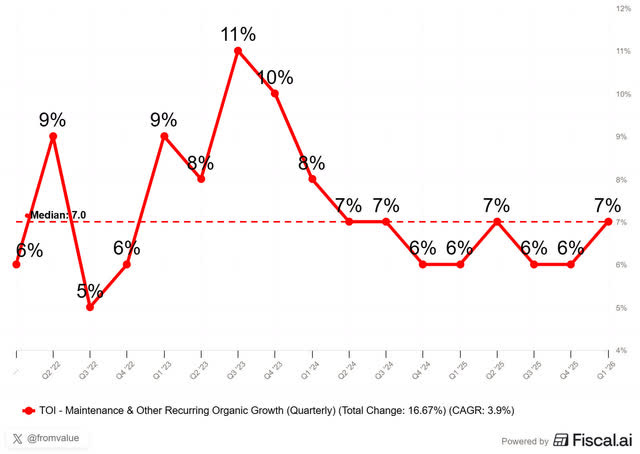

Maintenance and other recurring revenue grew 7% organically this quarter, the median over all quarters.

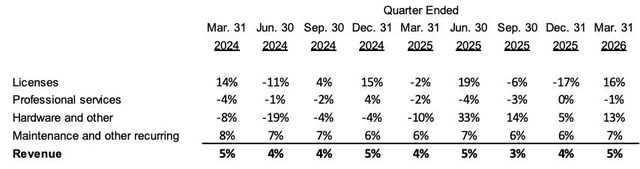

You can see a more detailed breakout here.

That recurring revenue accounts for €316 million of the €436 million, or about 72.5% of revenue. It is the sticky, predictable, high-margin business. The fact that this grew by 7% organically is an indication that there is no negative impact from AI so far.

Licenses came in at €11.5 million (+23%), and hardware and other were €9.9 million (+35%), but those are not really meaningful for revenue. Professional services generated €98.2 million (+19%). Organic growth was slightly negative here, but I have no problem with that, because services are always the lowest-quality part of any VMS business.

Net income dropped by 21.4% to €55.1 million from €70.1 million a year ago, and diluted EPS dropped from €0.54 to €0.41.

This sounds like a problem, right? But it isn’t. It’s just accounting noise.

Topicus’ Q1 2025 net income was inflated by a €32.8 million non-cash gain on its Asseco shares. The company bought a large stake in Asseco in January 2025 at 85 PLN per share, but the stock was already trading higher than that, so it booked a paper gain. That’s what causes this drop, which is only accounting.

If you exclude that, pre-tax net income this quarter was €64.4 million, versus €47 million of underlying pre-tax income last year (after removing that €32.8 million). So, the normalized growth is 36%.

This is exactly why, with Topicus, you can’t just read the headlines. The cash flows are another example. The metric that matters most for Topicus is free cash flow available to shareholders (FCFA2S). That’s the cash Topicus can give to shareholders if it stopped with acquisitions after taking out everything that goes to minority partners and to Constellation, the parent. It’s the cleanest number on what the business actually earns and I’m happy the company always provides it.

Operating cash flow rose 3% to €280.5 million, and FCFA2S 2% to €165.4 million. After a 23% revenue quarter with expanding margins, you’d expect more than 2-3% cash growth, right? So why did it grow so little? There are two main reasons.

Behind the paywall, I look at that, Topicus’ enormous acquisition firepower, the three numbers that challenge the AI bear case, the hidden value in Asseco and, most importantly, whether a stock down 51.6% is now genuinely cheap. As always, I also update the Selling Rules, the PM Quality Score, the valuation and my Buy-Hold-Sell rating.

If you want the full value, subscribe now!