The Trade Desk: Scoring the Quality and Valuation

Is TTD A Buy Now?

Hi friends!

Paying members of Potential Multibaggers, my paid Seeking Alpha service, get very regular updates about the stocks I have picked and they own. And I do that very systematically. Of course, the earnings are analyzed in all detail, but I have also developed a few scoring systems to look at the quality of a business and how attractive a stock is to buy right now. Let me introduce you to the PMQS, the QPI score & the BHS scale.

If you want to try out Potential Multibaggers for free for two weeks and get a 20% discount if you decide to stay, you can do that through this link.

If you read the previous post, about Paycom, you may already know but if you didn’t, what do these abbreviations stand for? If you don’t want to miss these free updates, subscribe to Multibagger Nuggets.

PMQS means Potential Multibaggers Quality Score. It’s essential to understand that it’s not just QS, quality score, but PMQS. What I mean is that stocks are not just scored on their overall quality but also on their potential to multibag. I think nobody questions the quality of Apple (AAPL) and it would score very well on several parameters (like financial stability, for example) but poorly on others (multibagger potential and revenue growth, among others) and overall, its PMQS would be rather mediocre. I focus on multibaggers, though, and that’s when you have to score for multibaggers, not only for quality, which remains a very important part of the equation as well.

I introduced the PMQS in 2022 when I saw that I had been deceived by some sweet-talking CEOs who knew what I (and other growth-oriented investors) wanted to hear. But it was just that, talk. The PMQS looks at all the granular details to see if the numbers match the talk. To put it differently, the PMQS should help me avoid losers like Twilio, Peloton, Teladoc, DocuSign and Stem. It was the PMQS that showed me clearly I had to sell these stocks and I did. At small or big losses, for sure, but all have either crashed a ton more (Stem, Teladoc, Peloton) or have gone nowhere since (Twilio, DocuSign).

Okay, so with the PMQS, you know how good a stock's quality is and how much potential it has to multibag, but how attractive is it to buy right now? That depends on the valuation, of course, and that’s where the QPI comes in.

QPI stands for Quality-Price Index. The name already suggests it: with the QPI score, I balance quality and price. The reasoning is that higher quality often deserves a higher price and lower quality a lower price and if you bring those two together, quality and valuation, you get a better idea if a stock is attractive to buy now or not.

How I do this is simple: I score the valuation out of 10, divide the PMQS by 10 and then add them up. I rank the scores of all my picks and that’s how I can see which are most attractive to add to. On top of that, I follow up the price of the stocks. If there’s a 20% move up or down, I update the valuation to see if the stock has become more or less attractive with the price movement.

The BHS scale is then simply a visual representation of how I see a stock based on the QPI. BHS simply stands for buy, hold, sell. But I don’t want to simply tag these terms, I put them on a scale to not oversimplify things. Often, it’s something between two things.

Before we go scoring The Trade Desk, don’t forget to subscribe, so you don’t miss these free updates.

Personal conviction 10/10

Unchanged from the start

This is mainly my or your own conviction based on everything you/I know about the company. Your own conviction may be very different here and you can adapt this score to your own liking.

You can download the sheet here to give your own score alongside me.

I have followed this company for so long already, long before I finally decided to make it a Potential Multibaggers pick in May 2019 at (a split-adjusted) $19.59.

What I have seen from Jeff Green's insights and the company's execution has impressed me the whole time, without any faltering so far. I know 10/10 is extreme and you can disagree and make your own score. But for over five years of intensely following the company has made me realize how special this company and its CEO is.

Just to make sure, my 10/10 conviction doesn't mean that I don't have doubts about the company. I should, because otherwise I'm not critical enough. It's just that my conviction could not be stronger than this. That's not the same as 100% conviction in real life, as this is still investing and there are no certainties in investing. It just means that my conviction for The Trade Desk is as high as it can get in investing.

Profitability 9/10

Unchanged since July 2022

If you want to create all of these graphs and use its extremely powerful AI insights, all the graphs are made with Finchat. I know no other investment research platform that provides so much value for such a low price. You pay about 1% of a Bloomberg subscription, but you get 85% of the value. You can try it out here and get a 15% discount.

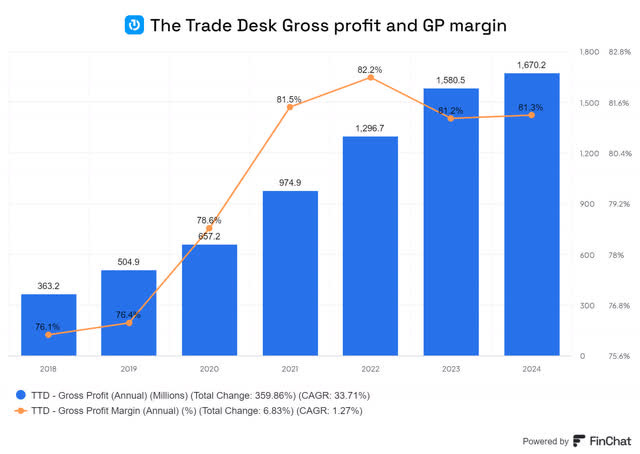

You see a CAGR of almost 34% for gross profits since 2018, which is great, of course. But gross profit is just that, gross profits. I also want positive free cash flow for The Trade Desk, which is not that new anymore.

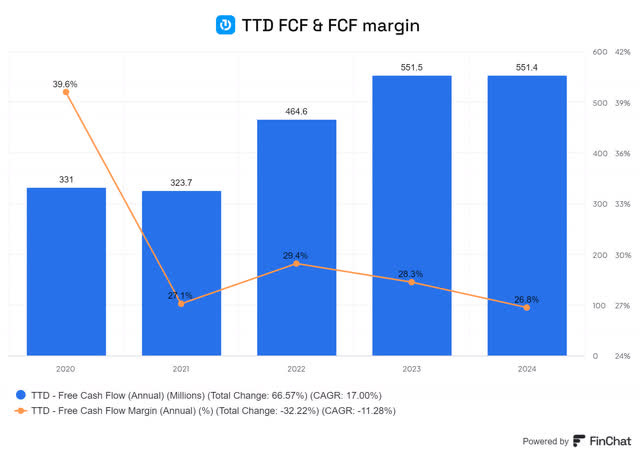

As you can see, that's not a problem. With an FCF margin of 27% and $551.5 million in free cash flow in 2023, The Trade Desk generates big piles of cash. By the way, the 2020 cash flow margin, at almost 40%, had to do with the pandemic, as travel was not possible.

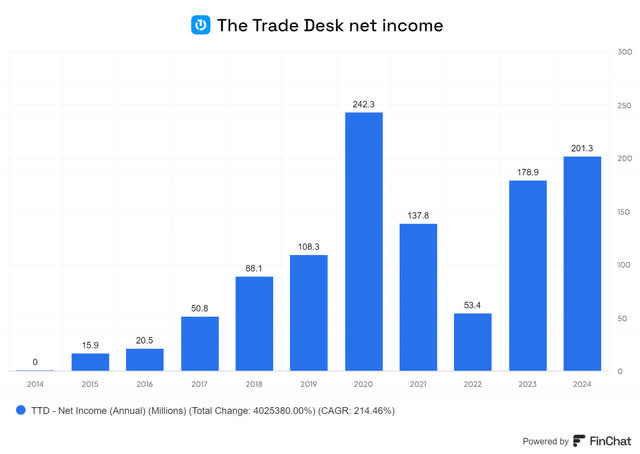

The Trade Desk has also been profitable every year on a GAAP net income basis since 2013. With the exception of Q2 2020, the pandemic quarter, that has even been the case in every quarter since 2013.

The dip you see in 2022 in GAAP net income is because of the big stock bonus Jeff Green got because he got the stock price above a certain level. Other such bonuses are also in his contract. I don't mind these too much, as they are not automatic. The stock has to be at certain levels for at least 30 trading days before he gets the bonus. This is the compensation summarized.

If Jeff Green gets all those targets before 2031, when the plan expires, he will have received 16 million shares. Of course, we come back to this when we look at the dilution, but this is about profitability. The Trade Desk is profitable on all metrics you can imagine.

But still, only 9/10. Why not 10? Because of this.

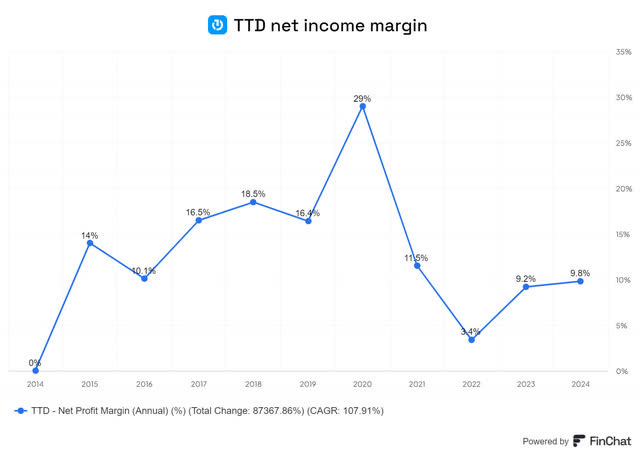

The net income margin could be higher than this. 9.8% is not bad, not at all, but it could be higher. Of course, this is just a minor point and 9/10 is still outstanding.

Sales efficiency 8.5/10

Up in July 2024

The sales efficiency formula first looks at S&M (sales and marketing) as a % of revenue. Then I look at growth this year and the expected growth next year and I take the average. That is divided by the S&M number. That gives me the marketing efficiency. If you add gross margins then and you multiply, you get the efficiency score.

These are TTD's numbers:

The score is up (from 8) because The Trade grew its revenue more and S&M as a % of revenue was down again. This shows the company's profitable scalability, exactly what we want to see.

Innovation 4.5/5

Unchanged since June 2022

This is part subjective, part measurable. Subjective as in: how many new products does the company issue versus its competitors? You can partly measure that, too, if you want, but the magnitude of the innovations is much more important than the sheer number of innovations.

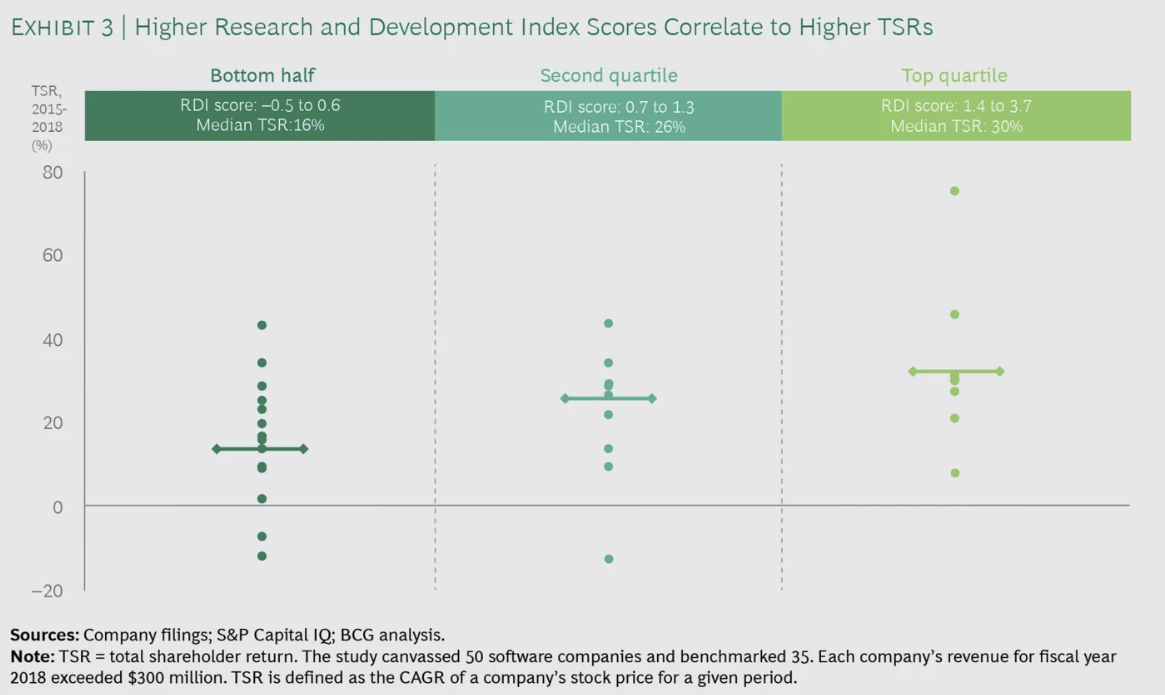

You can measure by looking at the percentage of revenue that goes to R&D. At the same time, I want some efficiency there, too, so I divide R&D expenses of the previous year by revenue growth in the trailing twelve months. Let's look at how The Trade Desk does.

The company spent 24.5% of its revenue in Q1 2023 on R&D.

With revenue growth of 28.3%, the R&D efficiency is 1.15, which puts TTD in the second quartile, but not that far from quartile 1, based on the 2015-2018 numbers.

Now, this is based on numbers from 2015 to 2018, when the environment was not as tough as it is now. So, while The Trade Desk is in the second quartile based on these numbers, I'm convinced that if they were updated, it would be in the best quartile.

With the continuous roll-out of innovations like UID, the complete rehaul of its platform with Kokai, the long-time use of AI, and many other big, impactful new initiatives, I think The Trade Desk deserves 4.5/5.

Must-have? 4/5

Unchanged since June 2022

I introduced it because of what Matthew Prince, the founder and CEO of Cloudflare (NET), said in May 2022:

I think that the world is about to get sorted into must-haves and nice to haves.

For The Trade Desk, it came through the tough period quite unharmed so far. Its revenue growth continued to be at a high level. I don't want to give it a full score because I want to be cautious. After all, the sector TTD is in, is sensitive for the economic cycle.

Revenue growth 4.5/5

Up in July 2024

This is very simple: how high was the revenue growth over the last twelve months? For The Trade Desk, that's 28.3%. As TTD re-accelerated its revenue growth, this warrants a 4.5/5, up from 4 earlier.

Revenue growth durability 10/10

Unchanged since the start

At least as important as revenue growth, is the durability of revenue growth.

The Trade Desk has a gigantic TAM and the trend is moving away from the walled gardens. With so little real strong competition when it comes to the open internet, with CTV still expected to grow for so long, and the company's innovation and execution, I rate The Trade Desk the maximum score here, 10/10.

Management Quality Score 10/10

Unchanged since the start

Jeff Green is one of those rare CEOs that I will rate 10/10. Everything he predicted, including things outside his own influence, became a reality. IDFA postponed? Yep. 3rd-party cookies postponed? Yep. CTV growing like gangbusters? Yep. I could go on, but I think you know what I mean.

The introductory remarks of The Trade Desk's earning conferences are fantastic overviews of where ad tech stands. Also, you shouldn't forget that he invented ad-bidding exchanges in 2002 already.

Insiders' Ownership 5/5

Unchanged from the start

Does management have skin in the game? This is out of 5 as it is not always a make-or-break but often it's a useful indication.

Founder, Chairman and CEO Jeff Green owns 1.1% of the A-class shares and 97.6% of the class B shares.

Jeff Green owns 48 million shares of a total of 498 million. That's more than 9.6%, worth more than $4.77 billion. That's a very high ownership stake and definitely another 5/5.

Multibagger potential 3.5/5

Since January 2024

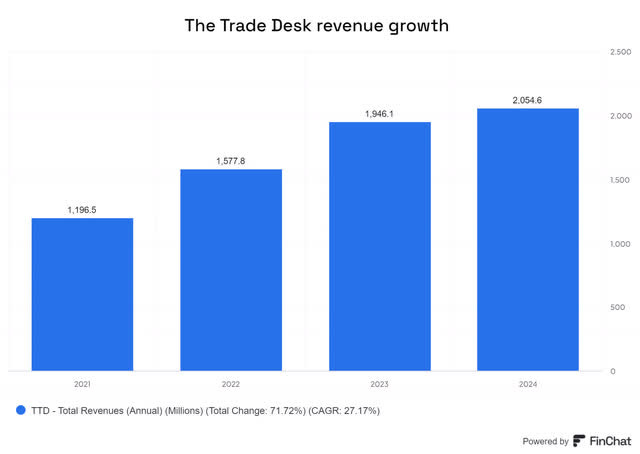

When I picked The Trade Desk, it had a market cap of $9.5 billion. Right now, it trades at a market cap of $49 billion, which makes it a fivebagger already since I picked it. That means it will probably be harder to 10x over the next 10 years.

Of course, the multibagger potential also depends on revenue growth, which is by far the most important contributor to long-term stock performance, as you can see in this graph.

The Trade Desk has grown its revenue by 27% in the last 3 years and 30% in the last five years.

If The Trade Desk can keep up that 27% growth pace for a full decade, it won't be much of a problem to 10x. But that's a big question mark, of course. Revenue growth is expected to moderate in the next years.

But of course, it's tough to forecast and The Trade Desk is a serial overdeliverer. Now, support that 20% would become the norm in the next year, even with the multiple coming down, it could be a fivebagger, not bad at all too, of course. In the end, we'll have to see.

The Trade Desk's TAM (total addressable market) has only grown and is an important player in CTV. So, it has the potential to become really big, like in a few hundred billion. Of course, I'm just pointing out the potential, nothing more. Having said that, the next score is the TAM.

TAM/SAM: 5/5

Unchanged from the start

TAM stands for total addressable market and SAM for serviceable addressable market, the market you serve because of your specific product and geographical limitations.

Both the TAM and the SAM are huge for The Trade Desk. Advertising is poised to become a $1T market. That's per year, yes. And Jeff Green is convinced all advertising will become programmatic. So, The Trade Desk plays on a huge field, the field where Google and Meta became such gigantic players.

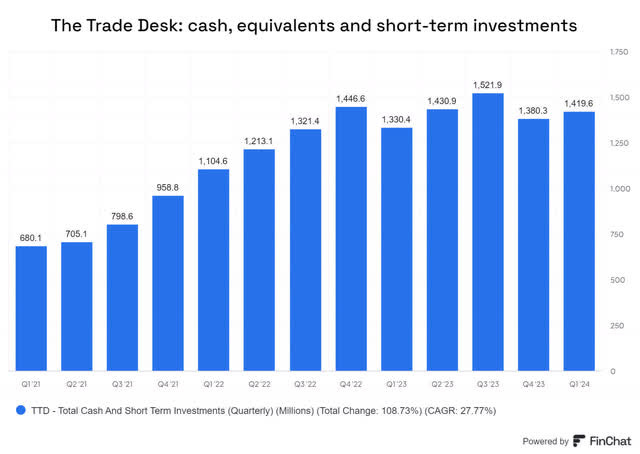

Financial Strength 10/10

Unchanged since the start

In this environment, financial stability is much more important too. That's why I rate it out of 10.

If we look at the financial strength of The Trade Desk, the first thing we notice is that the company has no debt. With a cash position of more than $1.4 billion, The Trade Desk is financially unshakeable.

So, I think a 10/10 is warranted here, especially because the company has been profitable every year since 2013.

The negatives

I also have negative scores, that can subtract extra points from that score. The scores are marked on 5 because a lot is implicitly captured in the other numbers.

Risk 0.5/5

A lot is already baked in financial strength, but this overall risk score shows more than just financial risk.

I don't see much additional risk for The Trade Desk, but out of principle, I still subtract 0.5.

Competition 2/5

Last change: July 2024

How strong is the competition? Again, you can't objectively measure that but there are indications.

For The Trade Desk, it competes with the big boys. Walled gardens are under more and more pressure, both from the governments around the world and competitive pressures, they might be extra dangerous. When cookies are abolished, The Trade Desk has UID 2.0. Up to now, that has worked well to compensate for things like Apple's IDFA change.

But when it comes to the open internet, The Trade Desk is the clear leader, also on CTV. But YouTube still has a big portion of streaming and Amazon also has more and more ads and both are not really attainable for The Trade Desk. Now, there are some workarounds, but that inventory could become even more valuable in the future.That, to me, is the biggest risk. But overall, The Trade Desk will benefit from the move to programmatic advertising, even if the big boys also do well.

Dilution 1/5

Lowered in January 2024

Dilution is a negative over the long run but that doesn't mean that companies should not issue stock when they are still growing fast. Look at Apple's shares outstanding before 2012, when it started buying back shares:

At the same time, I don't want to completely ignore SBC, and that's why I give a negative score.

Here we have to talk about Jeff Green's big bonus again. You know, this one, that I already shared before.

If Jeff Green gets all those targets before 2031, when the plan expires, he will have received 16 million shares.

Right now, there are 498 million fully diluted shares outstanding. That already included the first tranche, of course. That means if Jeff Green would get all the remaining 14 million shares, that would mean a total dilution of 2.8%. For a 3.4x of the current stock price, I think that would be a small price to pay.

This is the evolution of The Trade Desk's outstanding shares.

As you see, in the last three years, there was total dilution of 2.82%. Many high-growth companies have more than that in a year. For The Trade Desk, the CAGR is 0.93%.

That's why I only give 1/5 and that may even be a bit harsh.

Scale Advantage Shared 4/5

Unchanged from the start

When I look back at a few of the best investments, I see that they not only had substantial scale advantages but also shared them with their customers in some way. For Amazon or Walmart (at the time), I think this criterion is obvious. Because they are bigger, they can give their customers better prices.

For Google (GOOGL), for example, it may not be that clear. However, Google has always had a scale advantage: the more people use their products, the more they can give away for free. People's data were leveraged to generate profits for Google, but because of this mechanism, Google could offer so much for free (Gmail, Fotos, Drive storage up to a certain limit, etc.).

I have not come up with this concept myself. This is one that I borrowed from Nick Sleep from Nomad Capital. He uses this concept to guide all of his investments. That's why he started investing in Amazon in 2003 already. He has mostly held on to that position to now. He did the same thing with Costco, another company that shares the advantages of its scale with its customers, by only charging 15% on the purchase price, no matter what. This makes these companies almost impossible to compete with unless you start doing exactly the same thing.

I came across this concept in Richer, Wiser, Happier when I read it a few years ago and I dug deeper by reading several articles (like this one) about Sleep and this concept more particularly. The most prominent advocate of this? Jeff Bezos, who made this napkin sketch about it.

So, this competitive advantage can be significant. I'm going to withdraw or add points with this criterion. For some companies, extra scale only adds extra complexity. Those will get a negative score. I think of Uber (UBER) here. The normal scaling is the second level, which can be given little to no points. This means that if you grow, your scale gives you cost advantages. The third level is where all users also benefit from the scale. Here you will see higher scores, 4/5, maybe 5/5.

I give The Trade Desk 4/5, as the data its customers bring it can be leveraged on the platform for everyone. So, for example, if you want to target female 30 to 35-year-old women with a Master's degree in Malaysia, that's possible because the data of all customers is used anonymously by the AI The Trade Desk has employed. That's incredibly powerful. 5/5 may be even more appropriate, but I want to be conservative. After all, we don't know all the details.

Conclusion

The Trade Desk's Potential Multibaggers Quality Score is 85. For you, this may not say too much as you don’t have a lot of comparisons yet, but let me tell you that this indicates really high quality.

Of course, we also want to have the QPI or Quality-Price Index. Therefore, we need the valuation.

Valuation 3/10

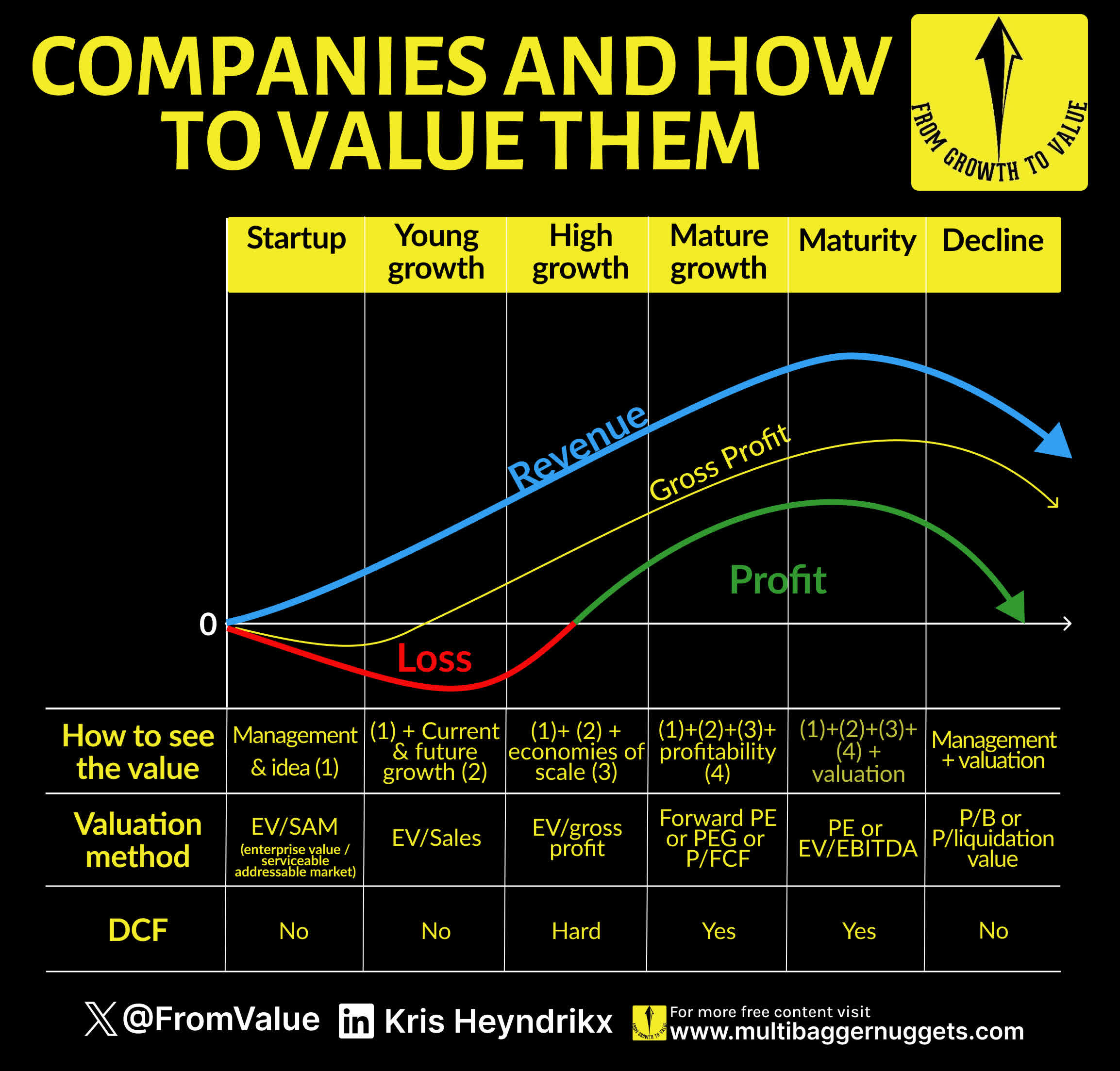

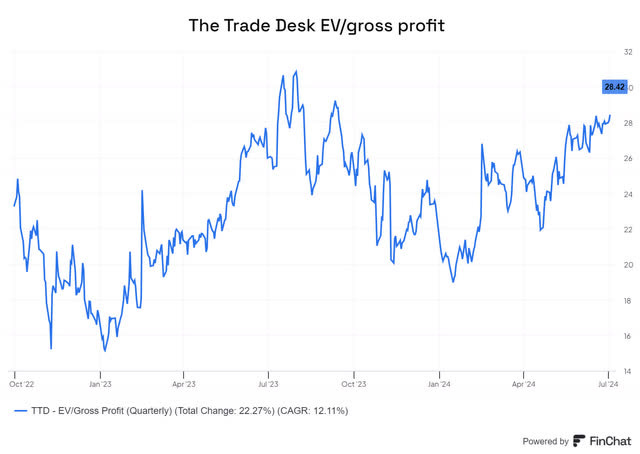

It’s important to look at this visual I made for the valuation.

I think it's fair to say that The Trade Desk is between high growth and mature growth. Let's first look at the EV/Gross profit. I'm very happy Finchat provides this as well, while many much more expensive platforms don't. If you want to try it out you can do that here. You also get a 15% discount if you take one of the paying plans.

At 28.4 times gross profit, the stock looks expensive.

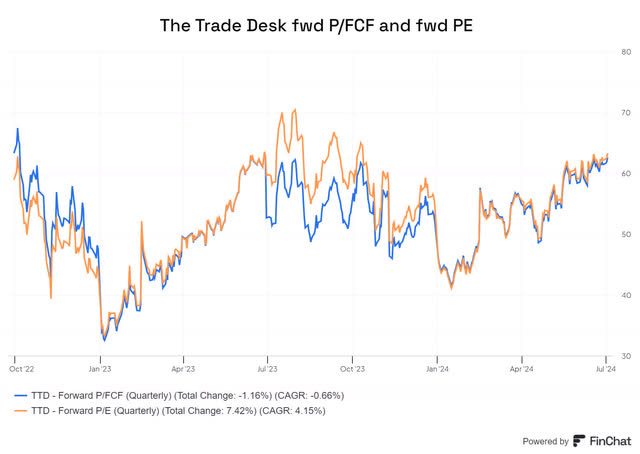

How about the forward PE and forward price/free cash flow?

At 62.5 times and 63.2 times, that looks really expensive as well.

If we look at the 2025 PE, we see 53. The expectations are that The Trade Desk will grow its EPS by about 20%. That means a 2025 PEG ratio of 2.65, which, again, looks very expensive.

Morningstar sees the stock as overvalued by 91%.

Of course, this assessment depends on the individual covering the stock at Morningstar. He only started in 2022, so I don't think he already knows the company well, as he gives no economic moat (a narrow moat would be the least I expect) and standard capital allocation, which I also disagree with. His fair value has increased from $43 to $46 to $48 to now $52.

Overall, I think there is no way you can sugarcoat this: The Trade Desk's stock is very expensive right now around $100.

If we add up the quality score and the valuation score, we see 11.5, which is a rather low score. Here you see the value of the QPI score. While the PMQS clearly shows the quality of TTD is very high, the valuation score makes it unattractive to buy now.

I think you already know that this will not be a strong buy. Let's go to the B-H-S scale.

The Buy-Hold-Sell Scale

The Trade Desk is a clear hold to me.

I never sell based on valuation. If you don't know why, I know dozens of people who could have been multimillionaires if they had not sold that one stock. The Trade Desk could be such a stock, and that's why I won't trim or sell based on valuation. If the stock goes down, great, then I can maybe add at a more reasonable price. Pennywise and dollar-foolish? Not me. But of course, to each their own approach. If you want to trim your position based on the valuation, I totally understand.

There's a sizeable chance that The Trade Desk's stock drops, but as long as the results keep coming, the stock price will follow eventually.

In the meantime, keep growing!