The One Number That Reveals Adyen’s Future (And Nobody’s Talking About It)

Forget the headlines. This one figure tells the real story

Hi Multis

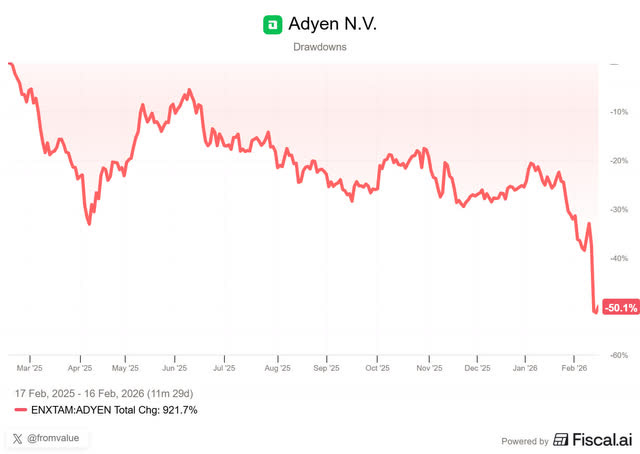

Here we go again. Adyen (ADYEY) reported its H2 2025 results on Thursday, and the stock promptly dropped as much as 20%. Ouch.

Even more painful, the stock is down 50% from its 52-week high last year.

So many investors view the stock price as the number 1 indicator of what to think. As a consequence, Adyen must be an awful investment from here, right?

My main criteria are not the stock price and the sentiment but the long-term underlying metrics and the long-term investment thesis. And Adyen has a management that thinks the same. Co-CEO Ingo Uytdehaage concluded the conference call with these words (my bold):

But we think that too much focus on the short term is not helping us in that long-term execution. And I think that is potentially something that we can explain better. But in all the decisions that we make as a Management Board, we only take the 3 to 5 years perspective and not this year’s perspective. And I think that’s something that I always like to highlight talking to investors.

That’s candy to my ear, especially since I know the company and its management well enough to know this isn’t just lip service but how they actually think.

But back to the earnings. What was the reason for the big drop? The 2026 revenue guidance of 20% to 22% constant-currency growth came in below the consensus of 22.8%. For H2 2025, processed volumes of €745.3 billion missed the €771 billion estimate.

But who’s wrong here? The company or the analysts? Long-time Multis know I call this The Wall Street Shuffle: the game with the consensus numbers and meeting, missing or beating them. The short-term misses and stock moves, no matter how dramatic, are noise if the company’s fundamentals are intact.

Let’s check the numbers first, then apply the Selling Rules, the Potential Multibaggers Quality Score and the Valuation.

The Numbers

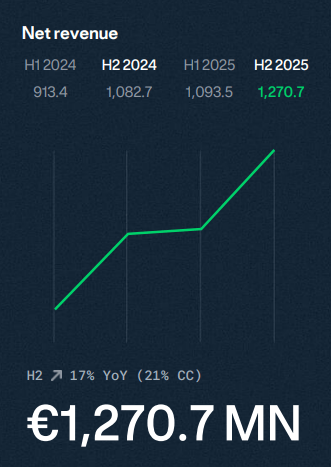

Full-year net revenue came in at €2.36 billion, up 18% YoY on a reported basis, or 21% on a constant currency basis.

H2 saw revenue of €1.27 billion, up 17% reported and 21% in constant currency.

(All images from the Adyen Shareholder Letter)

As you can deduce from the numbers, the currency exchange was a strong headwind for Adyen. The dollar lost quite a bit of ground compared to the euro, as most of you will know.

Processed volume was €1.4T for the full year, up 21% excluding a single large-volume customer. That’s Cash App, as I’ve mentioned in previous articles. Including it, it’s just just 8%. That shows that Cash App brought huge volume but very low profitability. Cash App comps make reported growth look artificially slow, but the margin quality of the remaining business is much higher.

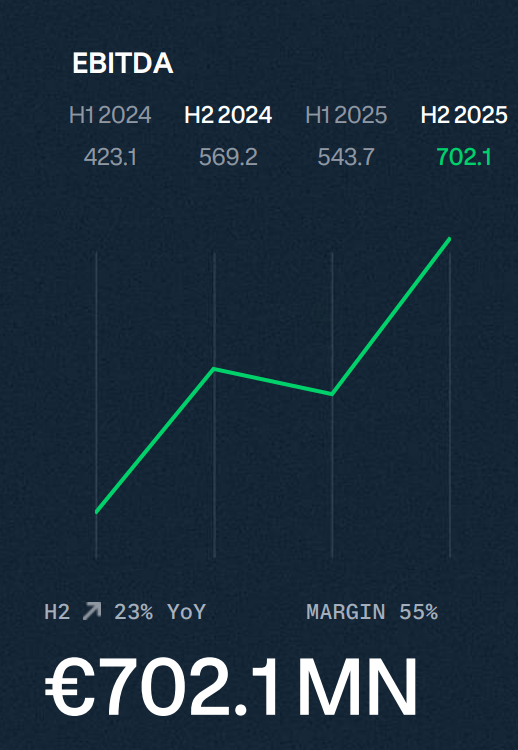

EBITDA was €1,245.7 million for the full year, up 26% YoY, again showing Cash App was not a big loss from this perspective. The full-year EBITDA margin expanded to 53%, up from 50% in 2024.

H2 even saw an EBITDA margin of 55%, showing that the operating leverage inherent in the business model remains extremely strong. EBITDA was up 23% YoY. By the way, a 55% EBITDA margin was the 2028 target

. Let’s put a green check there already in 2025. Impressive!

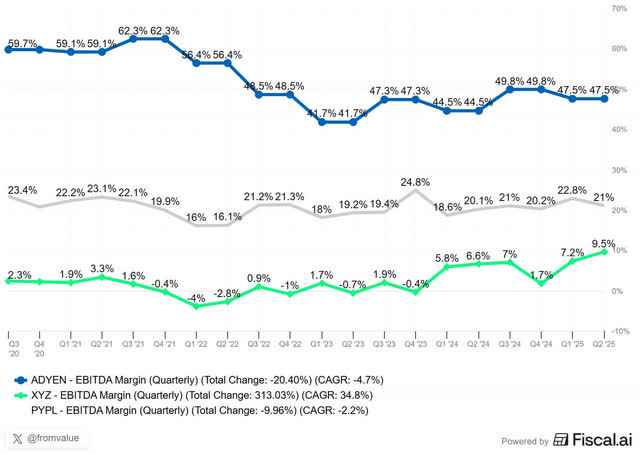

Just to show you how strong 55% EBITDA margins are, here’s a comparison with PayPal and Block. The H2 results are not in this chart yet, but they are higher, as we just saw.

Free cash flow came in at €1,081.3 million for the full year, up 26%, with an 87% conversion ratio. Very strong again. CapEx remained low, at less than 5% of net revenue.

Net income was €1,062.5 million, up 15% YoY, with EPS at €18.46 for H2 (up from €16.55). The lower net income growth compared to the strong EBITDA growth is entirely due to interest rates, which reduce finance income, not an operational issue.

Point-of-sale volumes were a standout at €311 billion of TPV (total payment volume) for the full year, up 34%. In-store terminal transactions for H2 alone reached €173 billion, up 26% YoY. This is the Unified Commerce story playing out exactly as management has been saying for years. Another green checkmark for its credibility.

The take rate matters, as it has been a part of the bear case for so many years (not completely correct, see the Selling Rules later in this article). The take rate was 17.1 bps in H2, up from 16.2 bps in H2 2024 and 16.8 bps in H1 2025. Then, the lower take rates were viewed negatively by many. I don’t see the growth in take rates being called a strength that much now, while the take rates were the strongest in years (I went back three years). I guess analysts who only emphasize the negative feel that they are considered smarter...

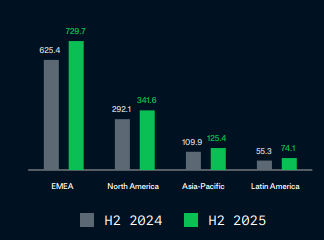

Geographically, EMEA was responsible for 57% of revenue, followed by North America at 27%, APAC at 10%, and LATAM at 6%.

In H2 2025, EMEA revenue grew by 17% YoY, North America grew 17% YoY, or 26% on a constant currency basis, APAC saw 14% growth YoY, or 22% on a constant currency basis and LATAM revenue jumped 34% YoY, or 37% on a constant currency basis.

If Adyen were a private company (and there were no consensus estimate), you’d probably just say the company delivered another solid year of 20%+ revenue growth and improving margins.

The Three Pillars (And Why the Numbers Tell a Different Story Than the Headlines)

Let’s walk through the pillar breakdown, because there’s a lot happening beneath the surface.

Digital, the largest pillar, posted H2 net revenue of €696.1 million, up 10% on a constant currency basis (7% reported).

Before you yawn or get worried, look at the context. CFO Ethan Tandowsky explained that 2025 saw several factors you need to normalize against: currency headwinds, the ongoing Cash App volume drag, and, the most important, more customers moving from Digital into the Unified Commerce pillar in H2 than in previous periods.

That last point is actually a positive. Tandowsky was clear about this during the conference call:

To me, that’s a positive, right? That’s the execution of a broader expansion strategy, being able to support our customers in more sales channels means that they put more trust, we’re able to win more of their share of wallet.”

When your Digital growth looks slow because merchants are trusting you with their in-store payments too, that’s a sign customers are happy about your services, not a negative.

The shareholder letter shared that more and more digital-native businesses are also expanding into physical interactions.

iFood, historically a purely online platform in Brazil, has expanded into in-store payments through its POS solution, Maquinona, powered by Adyen, which currently serves 800 venues in São Paulo and aims to reach 4,000 across Brazil. Netflix and Uber are experimenting with physical experiences too.

For Netflix, that’s “Netflix House.” Those are physical retail and entertainment places that opened in 2025. They’re and immersive fan experiences with themed food, merchandise, and things like a real-life Squid Game obstacle course.

Netflix House in Dallas, Source

They are already in Dallas and Philadelphia and soon in Las Vegas.

More about Uber later in this article.

It’s clear that the lines between “digital” and “physical” are blurring, and Adyen is at the center of that change. One consequence is that the three pillars won’t be as clear-cut anymore, but I’m totally fine with that.

Unified Commerce continues to be a driver of Adyen’s growth. H2 net revenue reached €431.3 million, up 33% on a constant currency basis (29% reported), with processed volume growing 30% YoY.

Transacting Unified Commerce terminals grew to 456,000, adding 92,000 in a year. That’s 25.3% growth for a physical product. Very strong.

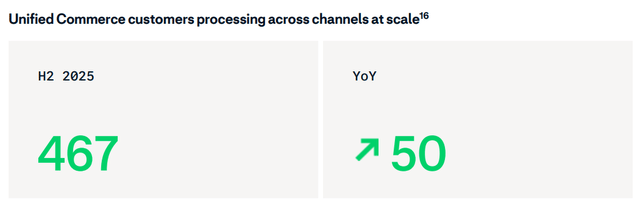

The number of Unified Commerce customers processing across channels at scale (defined as €10M+ on both POS and e-commerce, with over €50M total) rose to 467, up 50 YoY.

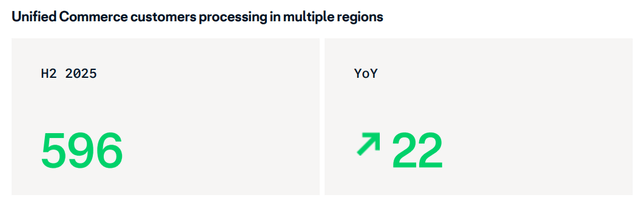

Unified Commerce customers processing in multiple regions hit 596, up 22.

Growth comes from all sides: retail, hospitality, entertainment, and food & beverage but also more complex industries like airlines, with Lufthansa deepening its partnership and Vietnam Airlines as a new customer.

The Starbucks win deserves special attention and Adyen gave it that attention in its shareholder letter.

Of course, Starbucks is another big name, but the case illustrates something that most investors don’t know or seem to be constantly forgetting about Adyen: how fast the company can execute.

They rolled out in 943 Starbucks stores across the UK, Austria, and Switzerland in just seven weeks, onboarding 120+ stores per week during standard business hours, deploying 2,375 payment terminals. I have studied this industry for years, and I don’t see a single competitor coming even close to that.

Since going live, Adyen has processed more than 20 million coffee sales across these markets. And another important data point: since August 2025, Adyen’s “Store and Forward” offline functionality has saved over 45,000 Starbucks transactions that would have failed due to Wi-Fi issues. When you’re running a coffee shop where every additional coffee matters for your profit, that’s crucial.

The Starbucks story also has a beautiful flywheel element. Adyen first won Alsea, Starbucks’ licensee in Mexico, and, through that relationship, built trust directly with Starbucks’ corporate team, leading to the European rollout. That’s the land-and-expand model Adyen constantly reminds us of. This time, it’s not just across borders, but across companies.

Adyen also expanded its LVMH partnership to support a more unified experience across its “Maisons.” When luxury houses trust you with their point of sale, you know the product is high-quality.

On to the third pillar.

Platforms remains the fastest-growing pillar, with H2 net revenue of €143.3 million, up 49% on a constant currency basis (45% reported).

Processed volume grew 54% if you exclude eBay. Platform customers processing more than €1 billion annually rose to 31, up from 28. Active business customers grew to 220,000, up from 145,000, an increase of 52%.

Here’s a detail that also demonstrates the physical-digital convergence: 31% of Platform’s volume was now on POS (point-of-sale), up from 25% a year ago. Platforms is no longer just about online payments; they’re embedding physical terminals, financial products, and full money management on Adyen’s infrastructure.

The Number That Nobody Is Talking About

Now here’s the number that really stands out for me: two-thirds.

About two-thirds of new enterprise merchants are turning on (parts of) Uplift, Adyen’s AI-powered optimization suite, from day one.

Co-CEO Ingo Uytdehaage shared this on the earnings call:

About 2/3 of our new merchants, they turn parts of Uplift on from the start. So that’s a very important KPI, and that gives us also the support that for existing merchants, it is a matter of time.

This can change the math. If new cohorts start with Uplift activated from the start, that means higher monetization and lower costs from the start. It means revenue per merchant for new cohorts starts higher and compounds faster than it did historically.

For existing merchants who don’t use the risk module yet, it’s a gradual conversation. But when two-thirds of your new customers opt in immediately, the value proposition is clearly obvious to the people actually buying the product.

Let me add a personal story here. Two weeks ago, I was on a train to Amsterdam. Next to me was a woman who was studying. Initially, I thought it was a student, until I saw the Adyen logo on her papers. I started talking to her. She said she was an Adyen account manager and was from the Paris office, heading to HQ in Amsterdam for the customer day. She worked with Lightspeed, the Canadian payments company and had to do a presentation there with someone from Lightspeed. She posted about it on LinkedIn.

On the train, she told me how she loved working for Adyen. They pay well (according to European standards), encourage personal development and working in the other offices (easy as there’s a single company culture) and a great feeling of doing work that matters. She had worked in London for a few months, for the experience and to take her English to a higher level (and it worked; her English was good!).

Several of her colleagues were also going to Amsterdam and were in the same train car. They were all very, very enthusiastic about how Adyen uses AI and is experimenting with agents, not just for security (also AI) but also for more personalized solutions for customers that have different needs than others. The company was in the quiet period (a period during which a company cannot communicate before the earnings), and they said they couldn’t share much because of that, but I certainly saw the enthusiasm.

The Personalize pilot is an example. It’s a part of Uplift. With Personalize, merchants saw conversion improvements of up to 6% alongside transaction cost reductions of up to 3%. Mobility provider Hoppy realized 2% payment cost savings while maintaining locally relevant checkout experiences as it expanded into new cities. This is a higher conversion at a lower cost, the holy grail for each and every merchant in the world.

The policy abuse detection pilot with Dynamic Identification uncovered something eye-opening. The shareholder letter detailed how a global luxury group found individual shoppers receiving up to €5,000 in refunds, which was, in some cases, up to 20 times their average basket value. In another case, a large sports and entertainment customer found a shopper with roughly 70% of transactions refunded over several years.

These are material losses that were completely invisible without Adyen’s AI insights. Dynamic Identification made them visible and merchants loved it, as they went to the tool on a daily basis.

Uber Kiosks

Let me talk about the Uber physical expansion here. The Uber relationship tells you a lot about where Adyen is heading. The two have a 14-year partnership. Adyen now supports Uber across 70+ countries, having rolled out in 40 key markets in the past year, integrating local payment methods such as Pix in Brazil, Afterpay in Australia, and WeChat Pay globally.

Adyen also powers Uber Kiosk. It’s a physical terminal now live at LaGuardia Airport (New York). Travelers without the Uber app, with no connection (not uncommon for air travelers), or a charged phone can walk up to the kiosk, enter a destination, tap a card, and get a printed receipt with their driver’s details. Additional rollouts are planned for hotels, ports, and international airports. As you can see, Uber is anoter example of a company transitioning from a purely digital company to a “unified commerce” player, and Adyen is the platform making it happen. Uytdehaage on the call:

It’s an example of a customer we’ve had for well over a decade that again says, ‘Hey, these are my priorities. This is how we’re looking to expand. Can you help us?’ And we’re there to support them.

Agentic Commerce

Agentic commerce... Ah, there we have it, one of the buzzwords of the year 2026 already. More and more, AI agents will buy things for us, but right now, it is still very early. Transaction volumes are immaterial, as Uytdehaage acknowledged. But Adyen has joined the Agentic AI Foundation and is actively shaping protocols with OpenAI, Google, Cloudflare, Visa, and Mastercard. So, it’s good that Adyen is preparing for the future.

The key insight is trust. In a world where AI agents buy things on behalf of consumers, you need to verify who’s behind the agent. That’s exactly what Dynamic Identification was built for. Uytdehaage:

Dynamic Identification is key here. And the reason why it’s key is because it’s ultimately a trust game. So in this new world, we need to know who is the consumer behind the agent and how do we know that we can trust the agent that is indeed acting on behalf of the consumer.

This won’t drive revenues in 2026. But being at the table shaping the standards for how agent-led commerce works is very crucial. That’s why I’m happy Adyen is there. There will be little to no direct benefit, but in 2032 or so, we might look back on this as a crucial decision.

Financial Products Are Inflecting

The shareholder letter revealed something the earnings call only touched on briefly: financial products are reaching an inflection point. Issuing volumes grew 8x YoY as platforms embedded cards directly into their core workflows. Capital loan volume more than doubled, with over 80% of businesses returning for subsequent loans. That’s a repeat rate that tells you the product works. And CashOut, Adyen’s instant payout product, reached a hundreds-of-millions-of-euros annualized run rate while still in pilot. Ok, let me repeat that: hundreds of millions of euros already while STILL IN PILOT! That sounds extremely promising.

Navan, the travel and expense platform, saw its issuing volume increase more than 5x throughout H2 while maintaining a 99.9% transaction success rate. Fresha and YetiPay are using Adyen Capital to embed financing directly into their vertical SaaS platforms. CFO Tandowsky highlighted issuing, capital, and bank accounts as areas where they’re seeing “nice inflection moments” and Adyen will continue investing there.

And then there’s the new product that also didn’t receive enough analyst attention: IMM (Intelligent Money Movement). This unifies money-in, money-out, and money management into a single operating environment for enterprises. This might sound boring, but for enterprises, it’s essential to have insights there.

Research Adyen did with BCG found that the average enterprise manages over 40 bank accounts across five to six banks and approximately 12 payment providers. Among respondents seeking an integrated solution, 74% want a single system that covers the full cash lifecycle, and 88% would consolidate all money management with a single provider.

That’s a gigantic addressable market that Adyen is only beginning to tap and it can do so because it already has its own banking licenses and the full stack to support it.

It would mean another expansion of Adyen’s TAM.

Why the Stock Got Hammered

At the November Investor Day, management gave a preliminary view of “low to mid-20s” growth for 2026. Three months later, the “refined” guidance is 20% to 22%. It’s not a disaster but it’s at the lower end of what was previously indicated, and below the consensus that was based on what management had shared on the Investor Day.

Tandowsky explained that this is based on deeper end-of-year conversations with customers about their 2026 road maps. Customers’ priorities vary each year. Some drive short-term revenue (e.g., the LatAm expansion, the fastest-growing region), while others are longer-term plays (e.g. agentic commerce).

I’m not worried. As long as Adyen helps its customers with their top priorities, they will give more business to Adyen. Management said the 2025 cohort of new customers was the strongest ever, driven primarily by Uplift, Adyen’s AI product. The 2026 pipeline looks like a continuation of that strength, according to management.

Management expects the margins to be about the same as in 2025, so around a 53% EBITDA margin. Adyen also keeps investing and plans 550 to 650 new hires, mainly in the U.S. and also in global tech hubs (Madrid, Bengaluru, Chicago).

The last question on the call was great. It asked what the biggest disconnect is between how Adyen performs internally and how investors perceive the story. Uytdehaage’s answer was revealing:

We’re building the company for the long term. And I think that’s very important because if you ask me, do I have confidence in how we’re building for the long term and do we have a long-term growth trajectory, my answer is a full yes. And I think what I find sometimes difficult to understand is why on the short term, the reaction is so intense, because the long-term perspective for us does not change.

He added that management takes a 3-to-5-year perspective on every decision. That’s the quote I used at the start of this article. That kind of long-term thinking is exactly what you want as a long-term investor, especially when the stock price says otherwise.

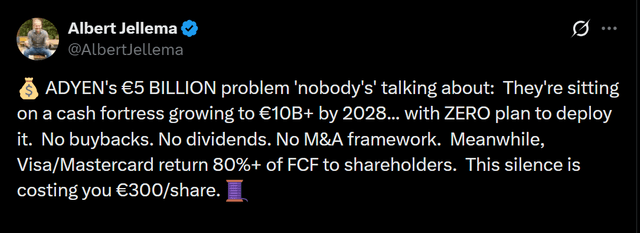

Before we go to the conclusion, I want to show you this tweet.

Oh, so having no debt and having a fortress of a balance sheet is a PROBLEM now?

Adyen has always said that in its industry, it’s important to have cash on the balance sheet. It’s a matter of trust, for customers and regulators. On top of that, the stock has never been really cheap, except for a few months. Or maybe now? We will see that in the valuation section.

Adyen has clearly said it won’t do M&A because it wants to keep its lean software. The Starbucks deal again showed where Adyen can do what no other payment provider can at that speed.

I have no problem with the company having $5B in cash (it’s more like €4.5 B, not €5B), to the contrary. It’s a key strength. Of course, if the cash pile keeps growing and at a certain moment there would be €10B, you can look at what’s best to do with that money. If the stock is undervalued then, a buyback would make most sense.

I think this is another example of short-term thinking.

Conclusion

An overwhelming majority of companies would give an arm and a leg for 21% constant currency revenue growth, 53% EBITDA margins expanding toward 55%+, 87% free cash flow conversion, a take rate zooming upward, and the kind of customer relationships that let you roll out 943 stores in seven weeks. The stock dropped because guidance came in 2-3% below expectations.

People who only read the headlines drove the stock down 20% when it opened in Amsterdam. Long-term investors who listened to the conference call later that day (6 hours after the market opened in Amsterdam, so American analysts could follow live) and read the shareholder letter understood that the slight misses and marginally lower guidance are just noise for the long-term story. With AI tailwinds on the horizon, Adyen is in a great place for outstanding growth for the long term.

Do you like this analysis? Don’t forget to subscribe if you want more.

If you are not on the paid plan yet, this is the ultimate chance.

(If you are a premium member already, just scroll past this message).

What do you get as a Premium member?

📊 The rest of this article, answering the question if Adyen is a BUY now.

✍️ Multiple high-quality articles per week (like this one)

📚 Full access to our entire library of deep-insight articles

🔎 Full investment cases

📊 Access to the Private Community

🎥 Regular Webinars (coming soon!)

📈 The Best Buys Now every month

✍️ The Overview Of The Week each Sunday

🔎 Deep earnings analysis (like this one)

Many Multis say that the community alone is already worth the price, but you get so much more.

Go to this page.

Subscribe to the yearly plan.