Hi Mulits

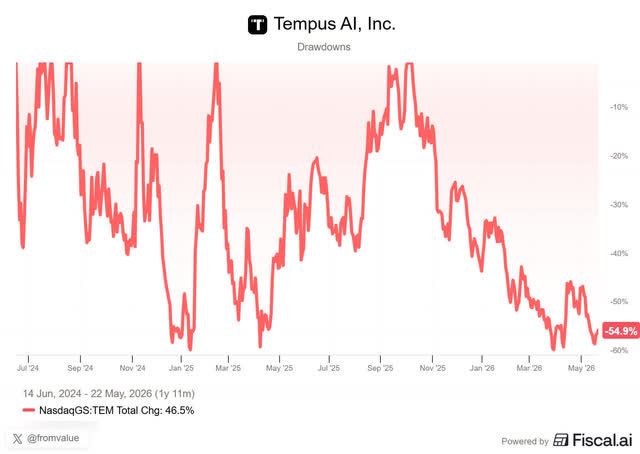

Two weeks ago, Tempus AI (TEM) reported its Q1 2026 results. The stock fell about 12% in the days that followed, and it’s now down about 55% from its October high of around $103.

Tempus was the most requested earnings analysis in our community. Your wish is my command!

I want to start with a contradiction. CEO Eric Lefkofsky opened the call by saying, “We had a great quarter,” and the press release talks about accelerating demand. But what if you read this? Revenue down sequentially, EBITDA negative, hereditary growth collapsing, profitability out the window. That sounds pretty bad, doesn’t it?

The difficulty is that both things are true and that can be confusing. So, this is a quarter where you have to know the context before you judge and that’s what I will try to provide in this article.

But first, a quick reminder of what this company is, as it’s not one that many really understand.

What Tempus Does

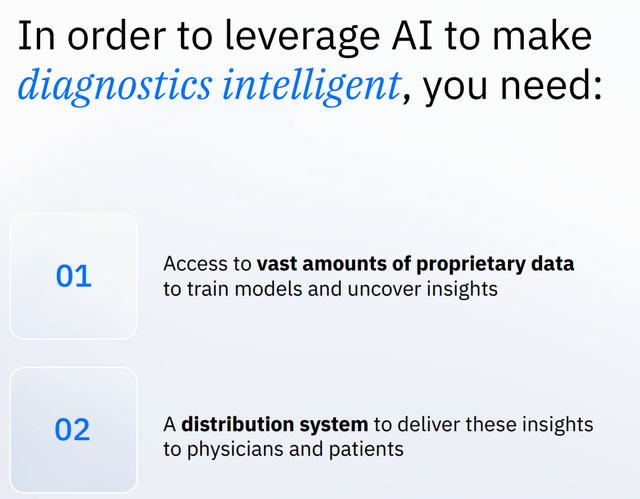

Many see Tempus as a diagnostics company and they are. But the tests are just the start of the story. The real business is using those tests to collect enormous amounts of patient data, DNA, RNA, imaging, and clinical records, and then structuring that messy data with AI and licensing it to pharmaceutical companies that can’t get it anywhere else. The confusing part is that this business currently accounts for only about 25% of the company’s revenue. 75% is still the tests.

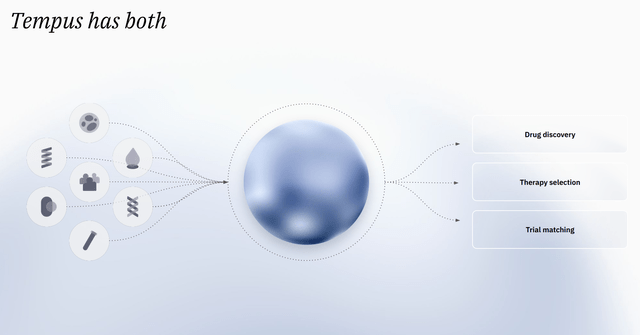

Of course, the data business has much higher margins. And there’s a flywheel. The more data comes in through the tests, the better the tests become, which sells more tests, which generates more data and so on. Almost no one else in the industry has both parts of the ecosystem.

The whole idea behind the company is on one slide from the earnings call deck.

The next slide completes the story.

The Numbers

Revenue: $348.1M, +36.1% YoY, beating the consensus of about $345.4M.

Gross profit: $222.0M, +43.1% YoY, growing faster than revenue.

Non-GAAP EPS: -$0.13, a $0.07 beat, improved from -$0.24 a year ago.

GAAP net loss: -$125.9M, versus -$68.0M a year ago and -$54.2M last quarter.

Adjusted EBITDA: -$2.8M, versus -$16.2M a year ago, down from +$12.9M in Q4.

Diagnostics revenue: $261.1M, +34.7% YoY, on oncology volume growth of 28%.

Data and Applications revenue: $87.0M, +40.5% YoY, with Insights (data licensing and modeling) up 44.1%.

Guidance: raised to $1.59–1.60B for the year (25% growth), adjusted EBITDA guidance kept at about $65M.

Some numbers evolve in opposite directions, and that’s puzzling. Gross profit grew 43% and revenue grew 36%, so the company became more profitable at the gross level. But the net losses almost doubled. Both are true. I’ll get to that later in the article.

What The Market Didn’t Like

I have recently started looking at this before my analysis. The reason is that it forces me to look into the negative story first and if I feel that it sounds convincing, it can influence the rest of my article and even the long-term thesis evaluation. If you first look at the information and then only at the end to the bearish story, it’s hard to rewrite the full article from a new perspective if you think bears have a valid point. That’s the great thing about investing and the investing process: you can always keep learning.

As far as I can see, there were four things the market didn’t like.

The sequential revenue decline, from roughly $367M in Q4 to $348M in Q1.

The negative EBITDA. A year ago, management made a real moment of crossing into positive adjusted EBITDA, and Q1 went back into the red.

Hereditary growth: the headline says 54%, but Tempus bought Ambry in February 2025, so most of that growth comes from Ambry. Real growth was just 7%.

What I would call ‘the gap.‘ I mean that there’s a big gap between gross profits up so much and GAAP losses down so much.

Let’s go into them one by one.

Below, for paying Multis: the full breakdown of all four worries, the data business and the upside that nobody's pricing in, my five new Selling Rules, the Quality Score, the valuation, and my Buy-Hold-Sell call.