Hi Multis

A few hours ago, I launched a poll in the community. The question was which earnings analysis I should do next.

SEA Ltd (SE) was number two. That was great, as Zack had promised the SEA analysis for Friday, but he was early and already sent it this morning. Awesome, Zack!

So, even if Sea was only number two in the poll (you can still vote if you are in the community for the next one you want me to tackle!), the SEA analysis is the first to be published. But, I’ll clear the floor for Zack. I’ll see you back for the Selling Rules, the Quality Score update and the valuation. At the end of the article, you should know if SEA is a BUY.

But to know that, we need top-notch information on the earnings. Take it away, Zack!

Hi Multis

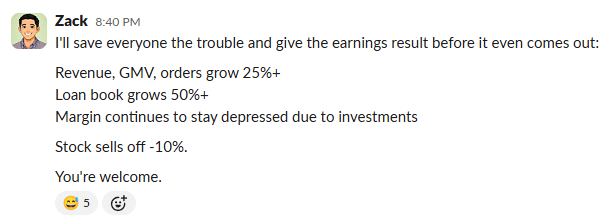

It’s been a tough earnings quarter for multiple Potential Multibaggers stocks in terms of post-earnings price reactions. In the private chat group, I made a tongue-in-cheek comment the day before Sea Limited’s earnings:

I was generally right with the metrics, except for the price reaction:

A 10%+ earnings reaction made me think the sell-off streak might be broken, but a few days later it was reversed, and we’re pretty much back where we started.

It’s another testament to how random stock price reactions to earnings can be. There’s a lot of noise and just a bit of signal. To separate both better, we have to analyze the earnings. Let’s jump into the results to find out.

Sea Limited Group Results

First, we look at the results of the whole group.

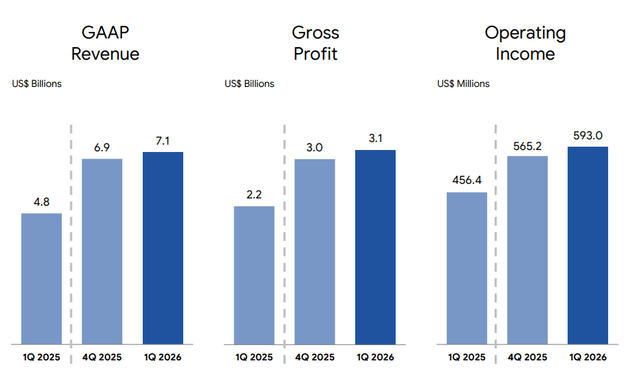

Source: Sea Limited

Revenue came in at $7.1B, growing 47% year-over-year, beating estimates by a whopping 11%. I already want to stress that right now, at the stage Sea is at, this is the most important metric to look at. The company is investing heavily and this 47% revenue growth shows that the investments are working. The majority of revenue growth came from Shopee and Monee; we’ll dive into each segment in detail later, of course.

Gross profit was $3.1B, growing 40.7% year-over-year.

Gross margins were 44% versus 46% the previous year. Investments in Shopee continued to pressure margins.

Operating Income was $593M, growing 30% year-over-year.

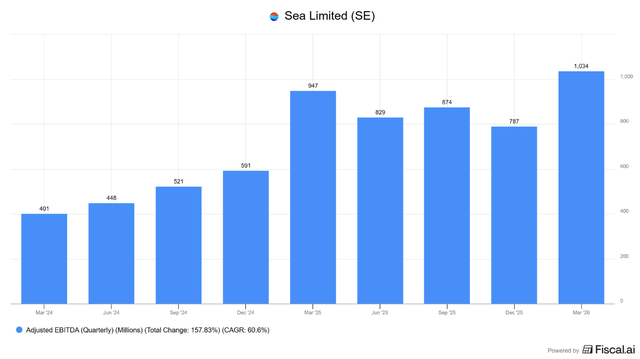

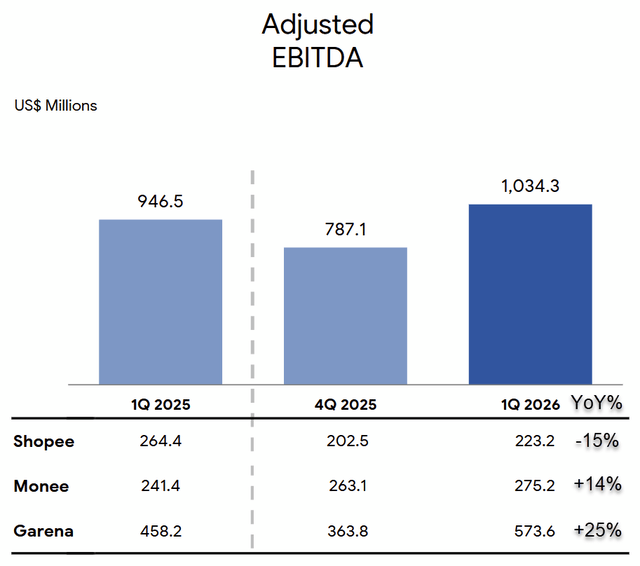

Adjusted EBITDA increased to $1B, growing 9.3% year-over-year.

For Sea Limited, we primarily use Adjusted EBITDA as the core profitability metric to remove accounting distortions that don’t reflect the true growth of the business, specifically Bookings (more on that in the Garena section).

Single-digit EBITDA growth doesn’t sound like much, but the fact that the company grows its profitability despite the big investments is great.

The largest contributor to Adjusted EBITDA was Garena, which had a standout quarter. You can see that in the graphic below with my annotated year-over-year growth:

Source: Sea Limited

Net Income was $438M, growing 6.7% year-over-year which led to an EPS of $0.70. Again, good to see that despite the big investments, Sea remains solidly profitable.

Additionally, Sea repurchased 1.8M shares for $168.4M this quarter under its $1B share repurchase program.

The limited FY 2026 Guidance was reiterated: GMV growth of 25% year-over-year and adjusted EBITDA no lower than 2025 in absolute dollar terms. Sea has a history of often general, loose guidance, so this is no surprise.

Overall, the top-level business metrics looked great, but the individual segment metrics tell the real story.

Shopee

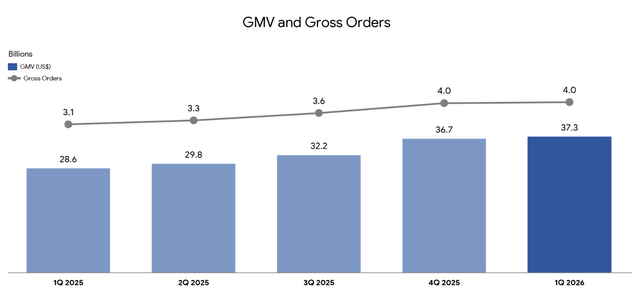

Gross Merchandise Volume (GMV) was $37B, 30.2% growth year-over-year.

Orders came in at 4B, 29.3% growth year-over-year.

Gross Merchandise Volume (GMV) was $37B, up 30.2% year-over-year, while orders came in at 4B, representing 29.3% year-over-year growth.

Source: Sea Limited

Investment continues to drive higher volume and more purchases:

Monthly active buyers increased 16% year-over-year

Monthly average purchase frequency grew 12% year-over-year.

Fulfillment order volumes grew 25% quarter-over-quarter

Shopee VIP membership continues to boom, reaching over 10M members (up 40% quarter-over-quarter) with program retention averaging 80%. Keep in mind, it had only 1M members just one year ago. That’s 10x growth in twelve months!

VIP is Shopee’s higher-tier membership subscription (think Amazon Prime or Coupang WOW) offering perks such as free shipping with no minimum spend.

Source: Shopee Indonesia

Unsurprisingly, VIP members spend more, with a double-digit uplift of 30% to 40% in some markets. VIP members currently contribute around 20% of GMV across Asia, and the program just expanded to Brazil in April.

On the AI front, innovation continues to drive efficiency and growth for Shopee:

AI-enhanced search/recommendation algorithms for buyers and AI-generated content tools for sellers led to a 14% improvement in purchase conversion rates year-over-year.

80% of customer queries are now handled by AI chatbots, helping reduce cost-per-contact by 30%.

AI-driven personalization and targeting contributed to the strong ad growth

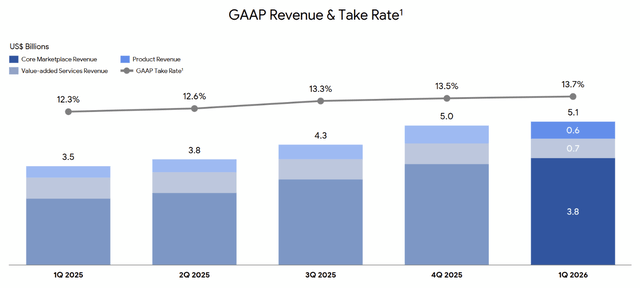

Moving on, Shopee Revenue grew to $5.1B, 45% year-over year:

Source: Sea Limited

Breaking out the Shopee revenue segments further:

Core Marketplace Revenue grew 60% year-over-year to $3.8B. Marketplace revenue consists primarily of transaction fees and advertising revenue.

Product Revenue grew 50% year-over-year to $612M. These are first-party products that Sea sells itself rather than relying on third-party merchants. It comes at much lower single-digit gross margins (4% this quarter), but management believes this is worth the cost to improve the buyer experience, expand selection, and ensure prices remain competitive.

Value-added Services Revenue was down 5.9% year-over-year to $692M. This drop was due to shipping subsidies as they build out better delivery and fulfillment services. Despite that, we’re seeing those investments pay off. From CEO Forrest Li:

With greater economies of scale, we are seeing lower delivery costs per order for these faster services compared to last year. For example, in Indonesia, our instant delivery service can deliver orders in as little as two hours in urban areas. Order volumes for this service grew over 35% in the first quarter, with cost per order reducing by around 20% year-over-year.

The overall Take Rate increased sequentially to 13.7%. That’s largely due to ads, which grew 80% year-over-year, and to an increase in ad take-rate of more than 90 bps year-over-year.

Source: Sea Limited

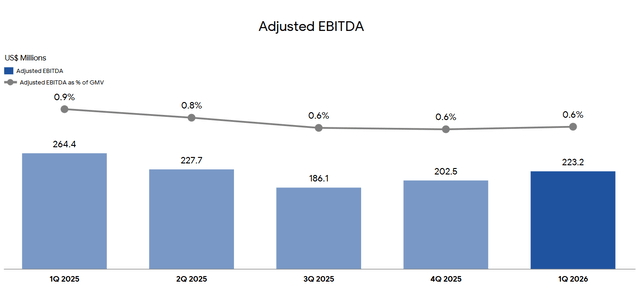

Despite that, Adjusted EBITDA was still down 15% year-over year at $223.2M

Shopee’s Adjusted EBITDA margin continues to track lower than in previous years, but as management has reiterated multiple times, the company is in an investment cycle. Management’s medium- to long-term target is to achieve an Adjusted EBITDA margin of 2% to 3%, up from currently 0.6%, as you can see. That said, the longer this goes on, the more critics will point to it as a persistent, structural defensive posture due to rising competition. The rising take rate is a counterargument.

Fred Liu of Hayden Capital had an insightful comment related to this in his most recent investor letter:

For example, China is the most competitive ecommerce market in the world with four large ecommerce companies all competing heavily. Despite this, all the companies are making ~2% EBITDA / GMV – 3x higher than Shopee’s current 0.7%. I think China clearly illustrates that relative competition and absolute market share isn’t necessarily correlated with lower terminal margins.

It seems more than plausible for Shopee to increase its EBITDA margin to its target goal once this investment cycle scales out, despite competitive forces.

Competition

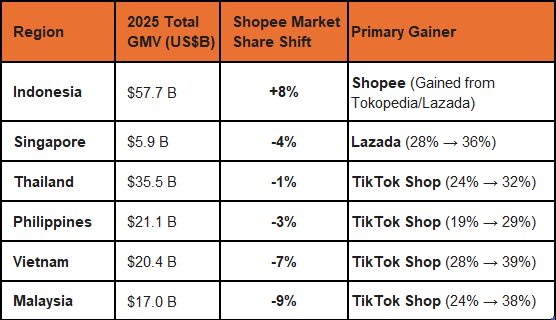

Some new data came out this past quarter on the e-commerce landscape in Southeast Asia. Below is a chart I made aggregating data from a report:

Source: Momentum Works

TikTok Shop is indeed gaining GMV share, some at the expense of Shopee, but also other players, which aren’t depicted here. More importantly, Shopee still gained market share in the biggest market (Indonesia) and retains a dominant share over the region overall:

Source: Momentum Works

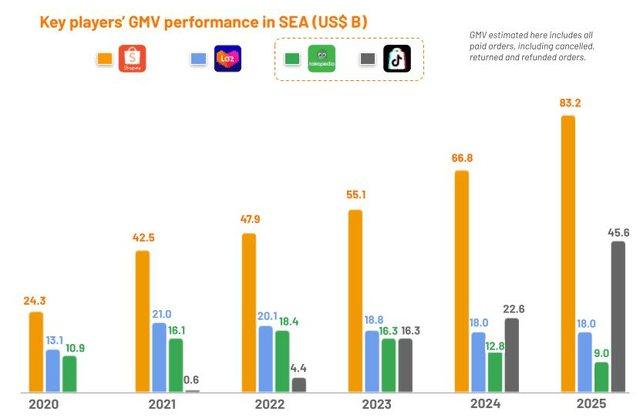

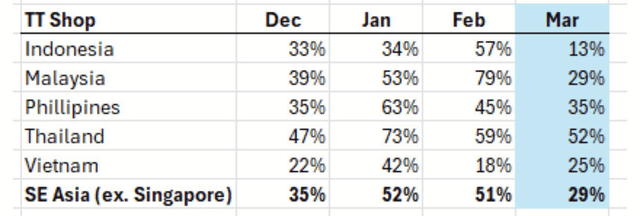

Some of this data may elicit some fear regarding competition. Even I had questions, but I also found alternative third-party data depicting TikTok Shop’s GMV decelerating, not accelerating:

Source: X

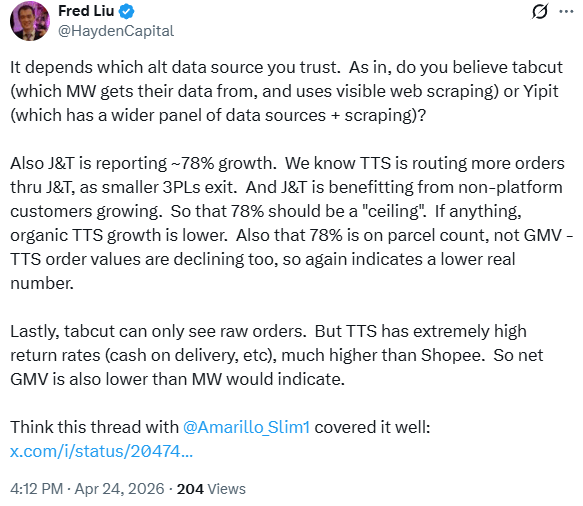

So what data should we trust? Below is a recent interaction I had with Fred Liu on the topic:

Source: X

That looks better for Shopee, doesn’t it? It was a good reminder of the wide range of conclusions one can draw depending on where data is sourced. It’s on us as investors to aggregate information and make our best educated guess. Third-party data is merely one data point among direct earnings reports. One piece of data should not be the end-all, be-all.

Personally, I see rising Shopee GMV, orders, revenue, and take-rates over the past few quarters. Management also commented on the competitive environment in Q4 2025:

Regarding your question on the competitive landscape, I think what we observed is relatively stable competitive landscapes across most of the market. Yeah, I think that we didn’t observe anything very different from what we see from last quarters.

TikTok Shop has grown in the region but so far has not adversely affected Shopee. In addition, there is no proof that they can’t co-exist. TikTok Shop targets a spontaneous, discovery-led “shoppertainment” audience buying low-cost items like fashion and cosmetics.

Shopee, on the other hand, captures high-intent, utility commerce where buyers proactively search for goods, including consumer electronics and everyday household products. More importantly, they have a comprehensive platform to nurture existing customers and drive repeat purchases, rather than relying on one-time, impulse-driven relationships.

If anything, Shopee is encroaching on TikTok’s territory with its expanding partnerships with YouTube and Meta as confirmed by CEO Forrest Li:

Our content ecosystem continues to grow healthily. In the first quarter, orders from live streaming and short-form video grew more than 50% year-on-year.

These orders accounted for more than 25% of total physical goods orders in Southeast Asia. To further strengthen our content ecosystem, we continue to deepen our content partnerships.

Orders driven by YouTube more than doubled year-on-year. Our collaboration with Meta is scaling well with over 4.5 million affiliates across our market, up nearly 30% quarter-on-quarter. In Indonesia, we have extended our Meta collaboration to enable seamless product promotion and checkout, not just on Facebook, but also on Instagram.

That was Shopee, next we move to the fintech segment of Sea Limited.

Monee

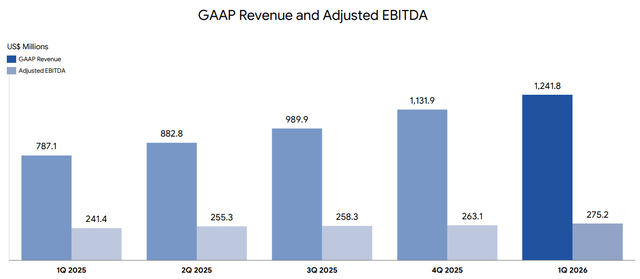

Revenue was $1.2B, up 58% year-over-year.

Adjusted EBITDA was $275M, up 14% year-over-year.

Source: Sea Limited

While topline revenue growth has held strong, Adjusted EBITDA growth continues to slow due to two reasons:

Provisions for credit losses are increasing due to expansion of the credit book.

Sales and Marketing expenses continue to grow significantly (up 142% year-over-year this quarter).

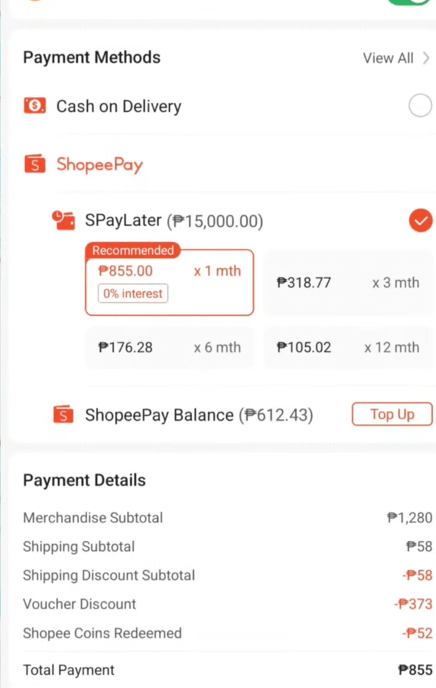

Similar to MercadoLibre and Nu Holdings, Sea Limited is capitalizing on the opportunity to expand its lending services aggressively to capture market share. Just last quarter, they opened up their SPayLater (buy now, pay later) application to all users, and that momentum is continuing:

Source: Sea Limited

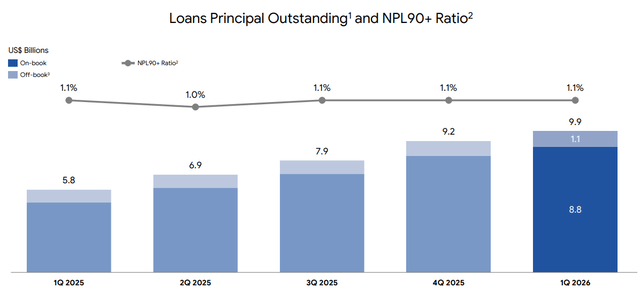

Loans Outstanding grew 71% year-over year to $9.9B

First-time borrowers this quarter were 4.9 million with 38 million active credit users, up more than 35% year-over-year.

Despite continued credit expansion, non-performing loans (NPLs) remained steady at 1.1%. As Kris mentioned in previous articles, NPLs can be artificially held down when a loan book grows this fast; there are simply more “good” new loans, outnumbering the bad, before the most recent cohorts have had time to season or default. In the future, it is completely normal to see NPLs rise slightly.

Sea has also been actively expanding credit to Brazil:

The Brazil loan book crossed $1B, growing more than 250% year-over-year.

SPayLater GMV penetration on Shopee Brazil is at 10%, well below mature Asian markets, indicating a massive runway.

They obtained the SCFI license, which will allow Monee to broaden the scope of financial services offered.

Sea also continues to expand credit use cases to offline settings (Off-Shopee SPayLater). This past quarter, Off-Shopee SPayLater loans in Thailand and Indonesia exceeded 20% of the total portfolio. On-Shopee lending now accounts for less than half of their total fintech business. CFO Tony Hou noted:

This proves that we’re not only able to drive our SPayLater or in general, lending in the Shopee ecosystem, but also we successfully drive this in the off-Shopee ecosystem.

Critics argue that the fintech arm was only successful because it was piggybacking on Shopee’s massive user base. With Off-Shopee expanding past On-Shopee lending, that argument is convincingly refuted. Monee has evolved into a standalone financial solution.

The last point to highlight is the growth of on-book versus off-book loans:

Source: Sea Limited

Taking another look at this graphic, we see that off-book loans have stagnated for a while. In the past two quarters, however, we have seen some growth again, albeit just 10% sequentially. Off-book loans are loans funded without the use of Sea’s balance sheet, allowing it to obtain revenue from financial fees while offloading the risk to other institutions. This is a part of a bigger thesis I have regarding Monee, but more on that at the end of this article.

Moving on to the final segment of Sea Limited, its gaming division, Garena.

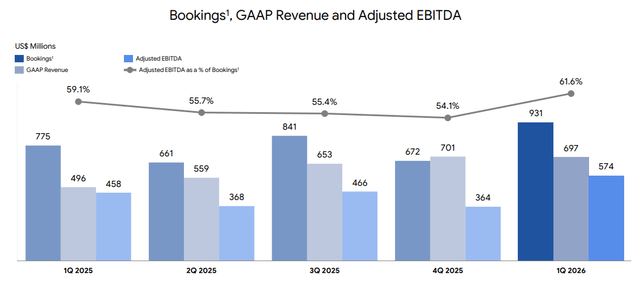

Garena

Q1 2026 came in stronger than expected, marking the best-performing quarter since the pandemic-fueled peak of 2021:

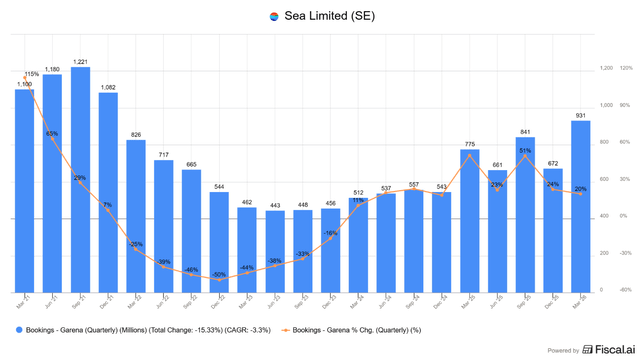

Bookings for the quarter came in at $931M, 20% growth year-over-year.

As a reminder, we choose to emphasize bookings over GAAP revenue due to revenue recognition rules. When Garena users buy in-game credits, it isn’t recognized as revenue until it is actually spent in-game.

While a 20% growth number doesn’t seem mind-blowing on the surface, zooming out reveals it was built on a very high base. Q1 2025 had a massive 51% year-over-year growth thanks to the Naruto Shippuden campaign. Stacking 20% growth on top of that is incredibly impressive at the maturity Garena is.

This quarter’s boost can be attributed to Free Fire’s collaboration with Jujutsu Kaisen, which generated over 700 million official content views.

Source: Free Fire

Unsurprisingly, the bookings boost lifted profitability, monetization, and engagement across the board:

Source: Sea Limited

Adjusted EBITDA came in at $574M, 25% growth year-over-year with a strong 61.6% margin.

Source: Sea Limited

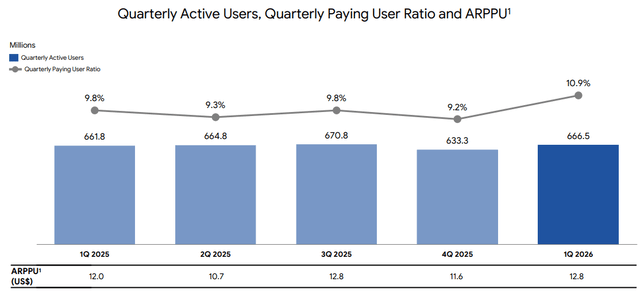

Quarterly Active Users were 666 million.

Paying Active Users were 73 million.

Average Revenue (Booking) Per Paying User was $12.8

Quarterly Paying User Ratio increased significantly to 10.9% which means a higher percentage of active players are converting to paying users.

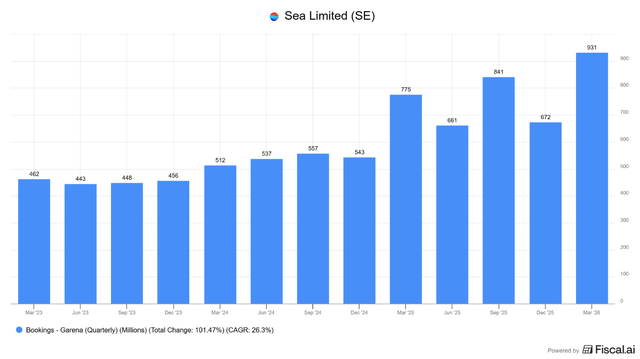

To close out this section, let’s take a look at the quarterly bookings chart again:

With this link, you get a 15% discount for Fiscal AI, so you can make these great charts yourself. Or use their top-notch screener. Or listen to the earnings calls, or… So much more.

After a slow period in 2023 and 2024, the quarters from 2025 onward prove that Garena can generate bookings acceleration almost on demand through high-impact partnerships with global IPs (Naruto, Squid Game, Jujutsu Kaisen). How sustainable this is in the long term remains to be seen, but I am very optimistic after seeing how significant these partnerships have been in driving bookings lately.

The Future: What Sea Limited is Building

This quarter was fantastic, with all business segments showing strong momentum. Let’s zoom out for a moment to gain perspective on what management is building for the long term.

As we saw in the Momentum Works report, Shopee is the undisputed #1 e-commerce player by GMV in Southeast Asia. Instead of just chasing raw user growth, they are deepening existing relationships through logistics investments and the VIP program. 10M VIP members against a backdrop of roughly 400M active buyers means penetration is only about 2.5%. Compare that to Amazon Prime or Coupang WOW, which exceed 50% penetration, and you see the massive runway ahead.

Additionally, continual improvement of customer experience leads to an increase in mindshare among buyers; they no longer consider comparing prices with other competing platforms, even if there may potentially be lower prices elsewhere.

CFO Tony Hou from the 2025 Q3 earnings call:

And Shopee remains consistently regarded as the e-commerce platform offering the most price-competitive products in both our Asian markets and Brazil, based on Qualtrics surveys.

I live in the US and I can resonate with this feeling as a frequent shopper of both Amazon and Costco.

When I go to purchase an item at either place, I can rest assured that I will most likely have paid close to the best possible price. Even if it isn’t, it’s not worth the effort to look elsewhere to save a bit more; the customer experience for members (e.g. perks, shipping, returns) more than makes up for it.

The large, high-engaged Shopee base serves as a zero-acquisition-cost funnel for Monee. When a Shopee buyer checks out, they are offered SPayLater:

Source: YouTube

Sea underwrites these loans using proprietary internal transaction histories, a massive data advantage over traditional banks in underbanked regions. Once a user builds a clean repayment history, Monee cross-sells them higher-value, off-Shopee financial products.

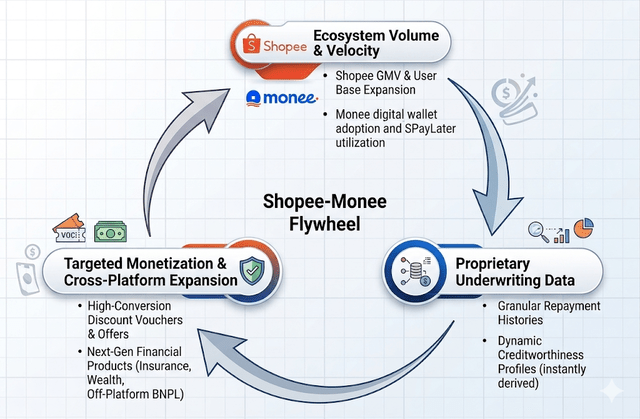

Combining these two businesses together creates the flywheel effect:

Source: Google Gemini

In the Monee section, I also mentioned off-book loans offering additional optionality. The shift toward an off-book model is the ultimate scaling mechanism. Actively utilizing partner capital allows Monee to act as a lending marketplace, taking high-margin origination fees while avoiding balance-sheet risk. This can unlock immense operating leverage.

What’s even better is that this model can be replicated across other developing countries that are underpenetrated in both e-commerce and financial services. We see that happening within Latin America (Brazil):

Brazil was the fastest-growing market in the past two quarters, and the investment is just getting started. In Q1 2026, SEA opened up three new fulfillment centers, bringing the total to five. The VIP program just launched this past April, and the loan book grew 250% year-over-year.

If you can’t tell already, Sea is successfully running the same playbook from Asia now in Brazil, and there’s nothing stopping them from applying it to other developing countries.

Here is the playbook summarized below.

Phase 1: Launch Shopee in the target country with aggressive, cash-burning market-share play, e.g., free shipping vouchers, discounts, low take rates. Subsidize with cash from other countries and Garena.

Phase 2: Once an active user base is established, transition from third-party to building out a proprietary logistics network (SPX Express) to drive down per-order delivery costs, speed up fulfillment, and establish a logistics moat.

Phase 3: Leverage Shopee customers to cross-sell low-risk fintech services such as a digital wallet for payments, but once credit history is established, start opening applications for SPayLater loans.

Phase 4: Lock-in engaged customers with higher-value services such as Shopee VIP, Off-Shopee loans, insurance, and wealth management services. Profit from long-term lifetime value from customers.

Taking a step back, we can clearly see Sea Limited executing this playbook masterfully. To realize it, you just have to look past the short-term price action and see the forest (or I guess Forrest?) from the trees. Shopee is solidifying its moat through a high-barrier logistics network and a sticky membership ecosystem; Monee is aggressively expanding its user base into a legitimate regional financial powerhouse; and Garena continues to serve as the ultimate cash cow, efficiently funding the entire enterprise.

So was the muted earnings reaction deserved? I think after reading this, you probably know the answer. But I’ll let Kris officially answer that with his upcoming parts of this article.

If you enjoyed this analysis and want to read more of what I have to say, you can find me on X @ZackStacksKap. Thanks for reading! Back to Kris.

Thanks, Zack. Fantastic work as always.

So that’s the quarter, and it was a strong one across all three segments. The question Zack kept pointing at is the one that matters: was the muted price reaction deserved, and is SEA a buy here?

That’s my part, and it’s for paying Multis.

Below the paywall:

The Selling Rules for SEA, the lines that would make me trim or sell.

The full Quality Score update.

My full valuation and where SEA lands in my QPI (Quality-Price Index), and what I’m doing with my own position in the Forever portfolio.