Hi Multis

This is such a period in which the punches don’t seem to stop when you are a growth investor. But that’s also often when the best opportunities are found.

Just look at this “unknown” company.

It just delivered record revenue of $23 billion, up 36% YoY, grew net income by 260% to $1.6 billion, and generated $3.4 billion in adjusted EBITDA. Would you think the stock would drop 25%?

Of course, it’s the old story: the stock price determines the stories that are being told. If you think that the fundamentals determine the stories, very often that’s not the case.

Just look at the stock price yesterday, up 8.23%. Fundamentals that suddenly improved in a day? Yeah, right.

I’ve seen this before with Sea (SE). I picked it at $54 back in 2020. I held and bought more when it crashed from $350+ to under $40. And I held when the market declared Sea a “Covid stock.” Every single time, the company has proven that great execution overcomes market sentiment over time.

The question is whether this time is different or just another chapter in the same book.

That’s what we will explore in this article.

The Numbers

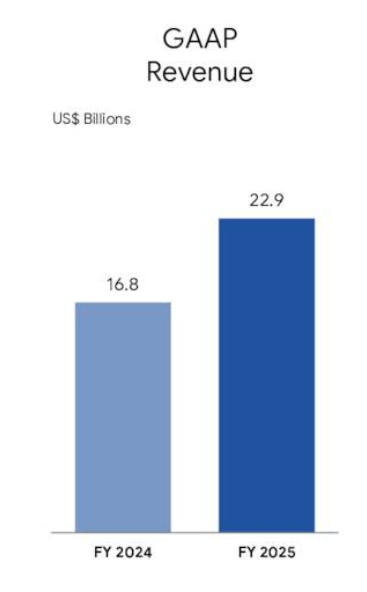

Let’s start with the full-year numbers. In 2025, Sea generated $22.9 billion in total revenue, up 36%.

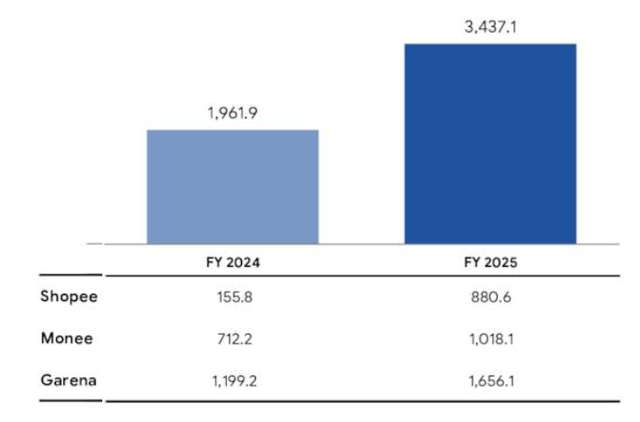

Adjusted EBITDA came in at $3.4 billion, a jump of 75.2%.

As you can see, Shopee did especially well, with more than a fivefold increase in adjusted EBITDA. This was mainly because of economies of scale. As you may know, Shopee raised its take rate, which positively impacted profitability.

I know that if I say take rate, many comment that it’s unsustainable, but the biggest part of that was driven by ads, which are growing fast. Therefore, this is sustainable and probably there’s a lot of growth left.

Garena’s adjusted EBITDA was up 38%, also very strong for a division that mostly runs on a game from 2017 (Freefire, of course). Monee’s (formerly Sea Money) adjusted EBITDA was up 43% YoY.

If something’s adjusted, it’s always interesting to know what. If you start with net income here, what’s added back (because it’s EBITDA) is the I (interest income or expense), the T (taxes) and the DA (depreciation and amortization). There’s also stock-based compensation and loan provisions.

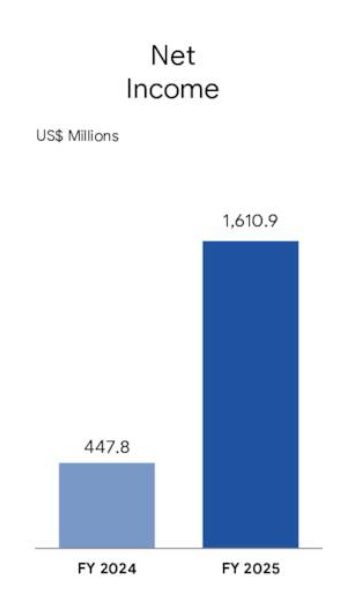

Net income came in at $1.6 billion, versus $448 million in 2024. That’s a 260% increase. Very strong.

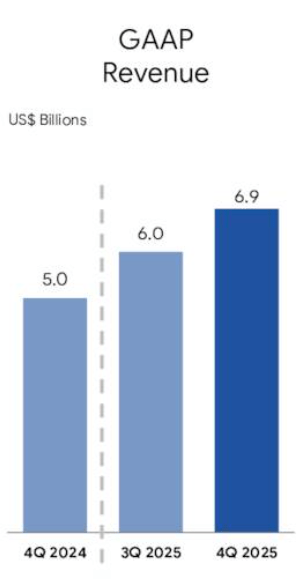

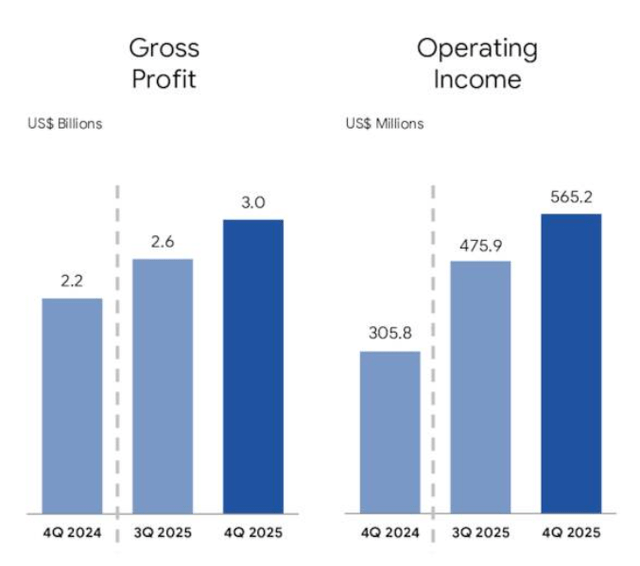

For Q4, revenue was $6.9 billion, up 38% YoY, beating consensus by about 6%. For revenue, that’s a lot.

Gross profit rose 36% to $3.0 billion. Operating income grew to $565 million, nearly doubling YoY.

The EPS came in slightly below analyst estimates. And the 2026 Shopee guidance mentioned ‘at least the same adjusted EBITDA’ despite 25% GMV growth guidance. That alone was enough for a 25% selloff.

So, what is the market actually worried about here? It’s not the growth because that was great. It’s the uncertainty about why continued growth in guidance doesn’t translate into greater profitability.

The market is always very impatient about an investment phase, even if it thinks it’s a good investment. The reason is simple: the market is not dominated by investors, but by traders.

Of course, that means we can focus on the crucial question: is this a temporary and intentional investment or a fundamental weakness in the business?

Let’s first dive into the different divisions.

Shopee

Shopee had a phenomenal 2025. I am sensitive to words and, to be honest, I myself wouldn’t expect the word “phenomenal” in an analysis of a stock that just dropped 25%. That also means that I use it very intentionally. Just look at why I use it.

For the full year, GMV came in at $127 billion, up 27%. As a reminder, GMV or gross merchandise volume, is the dollar amount of everything sold on the platform.

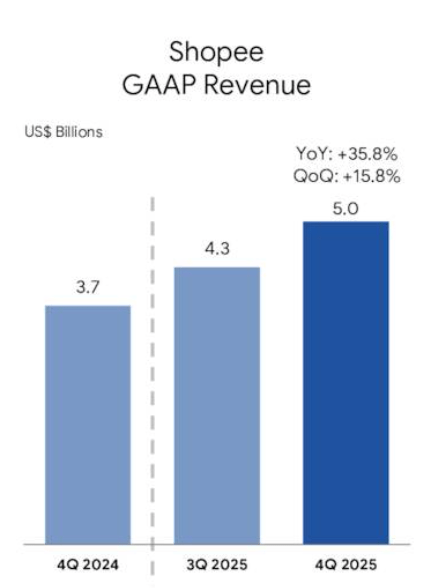

There were 400 million active buyers and 20 million sellers. For Q4, GMV was $36.7 billion, up 29% YoY from 4 billion orders, up 30%. Revenue came in at $5 billion for the quarter, up 36%, with core marketplace revenue (so, the countries in Southeast Asia) growing 50% YoY to $3.6 billion. That’s really impressive.

I have already mentioned this earlier in the article, but adjusted EBITDA for Shopee went from $156 million in 2024 to $881 million in 2025. Remember, this was a deeply loss-making business just a few years ago. The fact that Shopee generated almost $900 million in adjusted EBITDA while growing this fast seems to be completely ignored by the market.

This difference between GMV growth and revenue was mostly driven by ad revenue, which grew over 70% in Q4, with ad take rate up more than 80 basis points YoY. More than 20% more sellers are now paying for ads, and their average ad spend increased by more than 45%.

The overall take rate reached 13.5%, up from about 11.3% just two years ago. That’s a big improvement. And the great thing about ads is that it’s a self-fortifying machine. If more merchants run ads, those that don’t yet see them work also start using them.

But the market only looked at one thing. CEO Forrest Li stated that Sea aims to grow Shopee’s GMV by around 25% YoY, with adjusted EBITDA “no lower than 2025 in absolute dollar terms.” In other words, margins will compress. The market didn’t like that, to put it mildly.

But there’s a fundamental difference between a company that can’t generate margins and one that chooses not to because it sees larger opportunities ahead. If you are a shareholder of Mercado Libre, you have seen this play out there too: invest heavily, market panics, then the investments pay off nicely. Rinse and repeat. Sea’s investments have clear timelines and identifiable returns.

CFO Tony Hou was very explicit about this on the conference call (for context: VIP program is Shopee’s equivalent to Amazon’s Prime):

If you look at the fulfillment network, there will be a period of time we build it up, but there’s a clear investment cycle come with it rather than that is ongoing perpetual investment...

If you look at the VIP program, there’s a pure time that we will kind of educate the market, but as we get everything in place, I think the cost structure will be a lot better.

He also added something crucial: the 2-3% EBITDA of GMV margin target for e-commerce remains firmly achievable. And if you look at Q4 2025’s EBITDA margin at around 0.55% of GMV, that still improved year-over-year. The sequential decline from H1 to H2 was a conscious ramp-up of investments, not a competitive threat, which the market seems to assume. It’s funny how the market always seems to prefer the negative explanation. Of course, if you are an analyst, it’s better to be negative than positive. It makes you sound smarter, as you seem to warn investors. The funny thing is that many bring this as if bringing negative news is hard. It’s exactly the opposite. If you are positive, you get a lot more mud thrown at you in the market. Trust me, I know. :-)

So, where is Sea investing?

(If you don’t want to miss these articles, don’t forget to subscribe, for free or paid, if you want more).

Logistics

SPX Express, the company’s fulfillment arm, now processes over 30 million parcels every single day, making it one of the largest e-commerce logistics providers in its markets. In cities like Bangkok and Jakarta, instant and same-day delivery already made up more than 10% of order volume by the end of 2025.

That’s not just a charity service, of course. Aside from appreciating the service and not churning as quickly, such buyers also spend around 15% more on average than before they started using the program. That’s a great flywheel: better delivery leads to more spending. This is a part of the Amazon playbook, of course.

The great thing is that buyers have the choice. In Indonesia, orders using the cheaper shipping option more than doubled in Q4. Fulfillment services, from warehouses closer to buyers, already handle more than 10% of orders in some markets. The goal is to double that by the end of 2026.

Shopee also expanded instant delivery into groceries, partnering with local supermarkets in Thailand to deliver fresh groceries in as little as 1 hour. This expands the addressable market.

Then, Brazil. CFO Tony Hou explained the Brazil logistics angle nicely:

We have been operating with a much more efficient logistics network compared to what’s available to our — to the other players in the market with much lower cost. And we are able to run the businesses profitably with sort of a much lower basket size.

Brazil was again the fastest-growing market for Shopee in 2025. Delivery times improved by about 1.5 days YoY in Q4, which is quite impressive.

Shopee Mall GMV more than doubled YoY, and more than 300 new brands were onboarded. That matters because Shopee Mall is the higher-end segment. It has branded sellers and, therefore, higher basket sizes. It shows Shopee is moving upmarket in Brazil, not just sticking to cheap goods, as it’s often portrayed wrongly. That’s just the foot between the door.

The next step in Brazil is rolling out fulfillment capability at scale in 2026, another investment.

The VIP Membership Program

This is Sea’s equivalent of Amazon Prime. Subscribers get better free shipping deals, daily vouchers, and exclusive discounts.

Total VIP members surpassed 7 million by year-end. That’s impressive because it’s more than double what it was just a quarter ago. In every market where it launched, members increased their spending by double digits after joining. In Indonesia, VIP members spend 30-40% more than before joining. In some markets, VIP members already contributed more than 15% of total GMV in Q4.

Tony Hou shared a very interesting detail. Historically, the biggest challenge for subscription programs in Southeast Asia was the low payment success rates. Most people don’t have credit cards for auto-renewal. Retention rates were only around 40%. But by working closely with Shopee and Monee to enable smooth payment processing, Sea increased subscription retention from 40% to 70% in Indonesia over just a few quarters. And probably, there’s more room for improvement. This may seem like a detail, but it’s fundamental.

It also shows that the SEA ecosystem works. It’s a structural advantage that competitors without a fintech arm will have a very hard time replicating. Such seemingly “small” details add up.

The Content Ecosystem

This was an investment that already showed clear positive results. Orders driven by YouTube content more than tripled in Q4 YoY. The Meta partnership, launched in October, already has more than 3 million affiliates who linked their Shopee and Facebook accounts. Content’s share of business is already more than 20% and growing.

AI across Shopee

This one doesn’t get enough attention. I mentioned it in the Overview Of The Week a few weeks ago.

Sea is deploying AI across its e-commerce platform in ways that directly impact revenue and cost. On the search and recommendation side, they rolled out multimodal search: users can now search with a picture plus a description, similar to how you’d use Gemini or ChatGPT. CFO Tony Hou said the higher ad take rate is partly a result of the AI improvements: the platform now understands products and what users are looking for much better.

On the seller side, Shopee built AI chatbots that sellers can customize for their own stores. This helps sellers reduce employee or service costs. At the same time, it improves upsells to buyers.

Shopee also introduced tools for sellers to create product videos, pictures and descriptions using AI. All of these come with a positive return on investment for the ecosystem.

As mentioned in the Overview Of The Week, Sea also announced a partnership with Google, which is still in development. There are no details yet, but it builds on what they’ve been doing together for years on Google Shopping and Google Ads. On top of that, Google’s AI would also help with game development for Garena.

Forrest Li framed the company’s AI philosophy pragmatically:

We try to focus on the applications and how to connect that fantastic technology to people’s daily life from every corner of the world... We’re not going to try to make some fundamental large language model breakthrough. We’re not going to build data centers.

In other words, Sea will be an AI applier, not an AI builder. That’s a good strategy, I think.

Taiwan and competition

One more highlight: Taiwan. GMV growth accelerated to double digits in 2025. Shopee’s automated locker network grew to over 2,800 locations, making it the only e-commerce player at that scale in Taiwan. These lockers run at 30% lower per-order costs while also functioning as last-mile hubs. This kind of infrastructure moat is an extra defense against competitors.

When you look at the competitive landscape, CFO Tony Hou noted it remains “relatively stable across most of our markets.” No dramatic shifts is good news.

The US recently scrapped the de minimis rule, which allowed packages under $800 to enter the country tax-free. That was the backbone of how companies like Temu and Shein shipped cheap goods directly to American consumers. Now that this loophole is closing, those players need to find growth elsewhere and Sea’s markets in Southeast Asia and Brazil are the obvious targets.

That’s what the market was afraid of and yes, competition got tougher. But SEA doesn’t seem to suffer. Shopee’s take rate keeps rising, order growth accelerated to 30% in Q4, and the active buyer base keeps expanding. Companies that are losing a competitive fight don’t show numbers like that.

One more thing on the guidance. Sea has a long history of guiding conservatively and then beating. At the start of 2025, they guided for around 20% GMV growth. The end result was 27%. For 2026, the 25% GMV target will probably be a floor, not a ceiling.

Monee

Monee, Sea’s crown jewel, as I like to call it, keeps delivering. This segment generated $3.8 billion in revenue for the full year, up 60% YoY. Adjusted EBITDA crossed $1 billion, up 43% YoY. The fintech arm alone generated over a billion in adjusted EBITDA.

The loan book reached $9.2 billion at year-end, up 80% YoY. An 80% loan book expansion sounds risky, right? I heard this as an explanation for the big stock price drop.

But there’s a very important number to look at here, the 90-day NPL ratio. NPL stands for non-performing loans or, in other words, loans that can’t be paid back.

The 90-day NPL ratio held steady at 1.1% at the end of Q4. That’s very strong and even an improvement from a year ago. For context, this is far more conservative than comparable operations like Mercado Pago, where similar delinquency metrics can run much higher. For comparison, the average NPL ratio across Asia was about 2.7% in 2024.

On top of that, remember that Sea is lending to consumers and small businesses in emerging markets, the riskiest segments. Traditional banks in those same markets, with their decades of experience and conservative underwriting, are running NPL ratios 2-3x higher.

But, also very important to acknowledge, a loan book growing so fast will automatically lower the 90-day NPL ratio. Loans need time to go bad and if you grow your loan book fast, this will naturally bring down the 90-day NPL ratio. Nevertheless, the numbers look very conservative.

The growth came from three drivers.

Do you want to see if Sea is a BUY here? Become a paying member of Potential Multibaggers!

(If you already are, just scroll past this)

What do you get as a member?

✍️ Multiple high-quality articles per week

📚 Full access to our entire library of deep-insight articles

🔎 Full investment cases

📊 Access to the Private Community

🎥 Regular Webinars

📈 The Best Buys Now every month

✍️ The Overview Of The Week each Sunday

🔎 Deep earnings analysis

Many Multis say that the community alone is already worth the price, but you get so much more.

Go to this page.

Subscribe to the annual plan.