Karan here with the earnings analysis of Sea (SE). I hope you enjoyed my article where I shared my user experience on Shopee and with Sea Money/Monee (Maribank).

In this article, I will analyze the quarter. Kris will then update the quality score and the valuation to decide if the stock is interesting at this point.

Sea Limited's first quarter 2025 performance represents a defining moment in the company's evolution, a real moment of triumph for Forrest Li and the management team, who said they would achieve sustainability and profitability and proved that they could.

To recap, as far back as 2024, SE saw a 90% drawdown from its all-time high. I believe we have seen evidence that SEA will return to all-time highs sooner than most growth stocks. It was the kind of Goldilocks quarter we’re used to seeing from the likes of Crowdstrike and Mercado Libre, where every single vertical grew, alongside profitability. Let’s dig into the highlights.

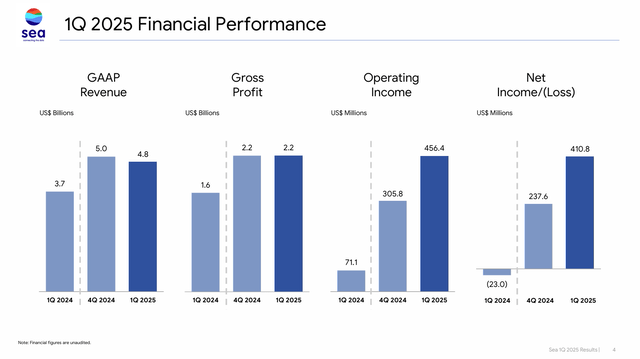

SEA reported total GAAP revenue of $4.8 billion, representing a 29.6% year-over-year increase, alongside a remarkable turnaround to net income of $410.8 million compared to a net loss of $23 million in the prior year period. This was only possible because every single division pulled its weight this quarter, as we will see.

Consensus was that this was a “miss” of $50 million, to which I will just paste this chart of the YTD trading range between the USD and some of the currencies SEA earns in

At a 4.8 billion run rate, a $50 million “miss” is a variance of 1%, more than likely given the absurd volatility we’ve seen in FX markets so far this year.

Q1 GAAP EPS of $0.65 beat by $0.04. The most striking aspect of Sea's Q1 performance was the dramatic improvement in profitability metrics. Adjusted EBITDA more than doubled to $946.5 million from $401.1 million, a 136% year-over-year increase, significantly outpacing revenue growth and a pure display of operating leverage at its finest. Gross profit jumped 43.9% year-over-year to $2.2 billion. The company's transformation from a net loss of $23 million in Q1 2024 to a net profit of $410.8 million in Q1 2025 represents one of the most impressive turnarounds we’ve seen from any Potential Multibaggers, vindicating management’s claim that they can grow profits alongside growth.

They also ended the quarter with $10 billion in cash in the bank, which is enough to buy ROKU or Celsius. I’ll pause there for a second to let you wrap your head around that. This company is a giant and deserves respect.

I mentioned before that every single business pulled its weight and SEA has the numbers to show it.

We no longer have a situation where Shopee or Sea Money are burning cash to fuel growth and so Garena’s bookings make or break the company. The simple fact is that Garena is now the SMALLEST division of the company, with Shopee’s operating income almost on par with it. Yes of course, gaming is still the most profitable due to the nature of the business, but it’s no longer the driver of SEA’s business. That said, we can still celebrate the record number of bookings and the role it played in the record profit

E-commerce Excellence: Shopee Is Going to Make a Lot Of Money Now

Simply put, this was an exceptional quarter for Shopee in terms of profitability.

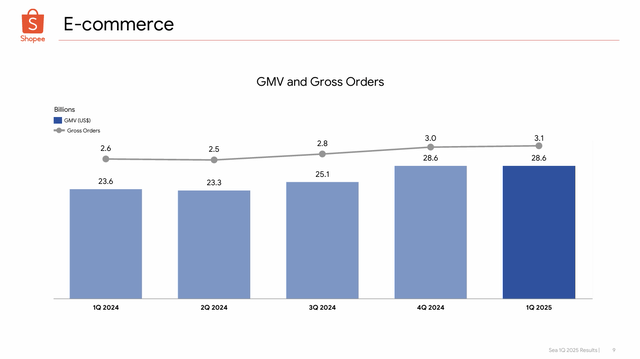

The e-commerce segment generated $3.5 billion in GAAP revenue, representing a 28.3% year-over-year increase, while achieving a record-high gross merchandise value ('GMV') of $28.6 billion, up 21.5% from the previous year. The fact that there was no seasonal slowdown in Q4 is extremely impressive and it means the company is well-positioned to exceed the full-year target of 20% growth that management guided to.

Gross orders increased 20.5% year-over-year to 3.1 billion and, most impressively, the e-commerce division achieved adjusted EBITDA of $264.4 million, a remarkable turnaround from a loss of $21.7 million in the prior year period. This represents an EBITDA margin of approximately 0.9% relative to GMV, showcasing Shopee's path toward sustainable profitability.

To sum up:

Some key call-outs here:

CEO Forrest Li emphasized the platform's continued market leadership, stating that "Shopee sustained market leadership with improved profitability across both Asia and Brazil" through focused execution on "enhancing price competitiveness, improving service quality, and strengthening our content ecosystem.”

It’s great news that Brazil is no longer considered a money sink and has started meaningfully driving profitability as well with positive adjusted EBITDA Average monthly active buyers (>15%), ad revenue (>50%), sellers who spend on ads (22%), spend per ad (28%) all went up double digits Conversely, the logistics efficiency improved significantly, with 6% decrease in Asia and a staggering 21% decrease in Brazil, showing us just how meaningful a fully fleshed out logistics arm can be, as a driver of profitability.

Digital Financial Services: The New Favorite Child

At the outset, let me say that the strangest part of the ER was reporting out that “Sea Money” is now called “Monee”. I hope the consultant who came up with that is enjoying their well-earned jet ski (I’m kidding). That said, the division has shown no impairment in performance due to embarrassment or other factors and continues to kill it.

Monee delivered the most impressive growth metrics across the entire company portfolio. The segment generated $787.1 million in revenue, representing a 57.6% year-over-year increase, while adjusted EBITDA grew 62.4% to $241.4 million. This growth trajectory positions Monee as a significant value driver within Sea's ecosystem, contributing meaningfully to both top and bottom-line growth

Of course, many of us may wonder why this rebranding was necessary and to be fair, Forrest Li did address it:

We chose the name Monee because it is simple, cute, and, just like our company's name Sea, easy to write and pronounce. Monee also resonates well with the name of its sister brand, Shopee, reflecting the seamless, synergetic connection between the two ecosystems. This rebranding supports the integration strategy between e-commerce and financial services, potentially driving higher customer lifetime value across the platform.

Ok fine, it’s a nod to “Shopee” which also sounded ridiculous when it first launched but is now a verb in Southeast Asia, and as I will cover in a separate piece, they are serious about cross-selling both platforms to generate higher customer value. So, I will give them a pass on that name, because look at those revenue and profit numbers; does the name really matter?

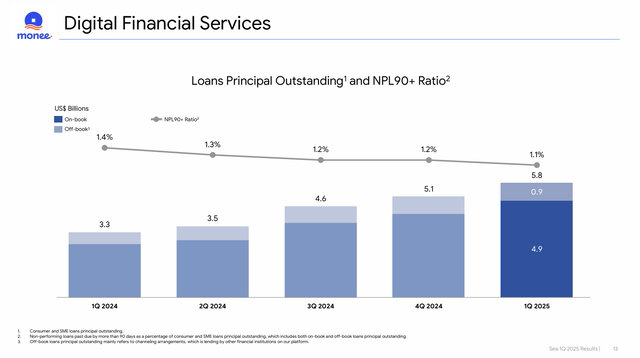

Of course, as we have seen with NU, growth in loans gets people scared about delinquency and here we have a hilarious chart of 90+ NPLs at an all-time of 1.1% despite the book increasing by >75% in the past 1 year. (including both consumer and SME). This is also 13% higher than Q4 2024, so economic uncertainty wasn’t a big factor in Q1.

The ability to grow the credit business at such aggressive rates while maintaining stable asset quality metrics suggests sophisticated underwriting capabilities and robust risk management frameworks that should support continued expansion.

Again, let’s look at the major call-outs here:

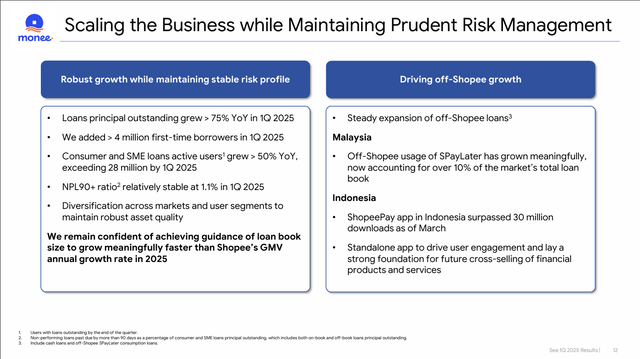

More than 4 million first-time borrowers in Q1, which means people have a higher degree of trust in Monee, especially since active users grew more than 50% to a total of 28 million.

The loan book is forecast to grow faster than Shopee’s GMV, hence underscoring how this has become the most important component of SEA’s business

The growth is coming both on platform and off, for Malaysia, almost 10% of the total market is now with Shopee. Indonesia also saw strong user growth which sets the stage for future expansion.

And with that, we move on to Ye Ol' Faithful, Garena.

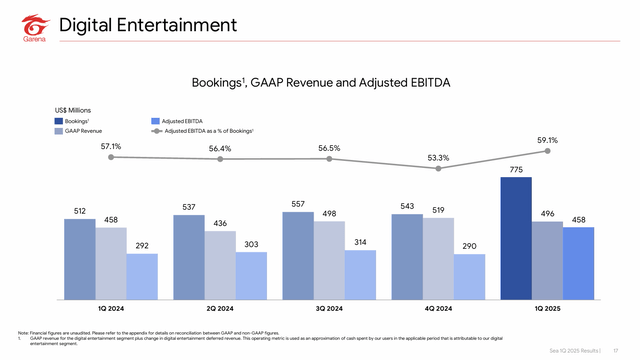

Digital Entertainment: Garena's Spectacular Recovery

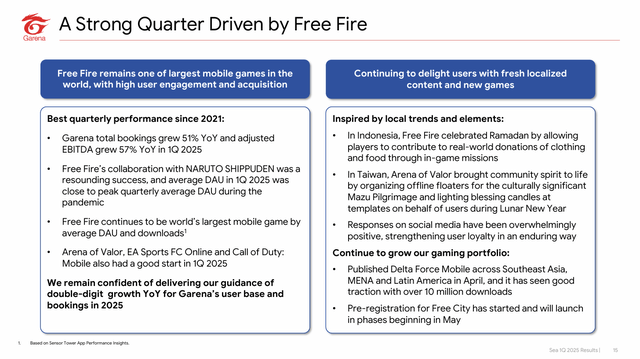

Garena's Q1 2025 performance represented the gaming division's best quarter since 2021, driven primarily by the phenomenal success of the Free Fire and NARUTO collaboration launched in January ’25. NARUTO is a popular Japanese manga and anime series.

- IMDb")

Total bookings surged 51.4% year-over-year to $775.4 million, while quarter-over-quarter growth of 42.8% demonstrated the immediate impact of successful content partnerships and user engagement initiatives.

GAAP revenue for the digital entertainment segment reached $495.6 million, compared to $458.1 million in the prior year, while adjusted EBITDA increased 56.8% to $458.2 million. This margin expansion reflects the high-margin nature of gaming revenue and the operational leverage inherent in Garena's business model when user engagement and monetization align effectively.

The Free Fire and NARUTO collaboration's impact wasn’t just about users. While average daily active users ('DAUs') for Free Fire approached peak quarterly levels achieved during the pandemic, they also meaningfully drove revenues and in-game purchases.

This actually addresses one of the frequently cited criticisms of Garena being reliant on a single game. The fact is that if something like an IP collaboration can generate such enormous growth, it opens up the platform to similar such tie-ups with other major combat-oriented IPs.

That said, Garena did say that Arena of Valor, EA Sports FC Online (formerly FIFA online), and COD Mobile had strong metrics in Q1 as well, so there is some potential for other games picking up the next trough in Freefire.

The gaming division's recovery vindicates management's long-held belief that Garena is an evergreen franchise for mobile. I think we’ve all been burned by 2022-23 which proved how cyclical gaming can be, but for now we can enjoy the successful execution in Q1’25 and thank Garena for all it’s cash flow over the years, that powered the growth of Shopee and Monee.

Conclusion

Sea Limited's Q1 2025 results represent a watershed moment in the company's history. In the deep, dark days of 2022/23, when SEA was down 70% from all-time highs, the market scoffed when management said they would first pivot to profitability and then re-accelerate growth.

Well, they did what they said they would. I mentioned at the top of the note that SE experienced a 90% drawdown from its all-time highs. As of May 2025, this has improved to a 55% drawdown, meaning if you bought SEA at its peak and held, you’ve recovered substantially from a price perspective, although it still needs to double again from here.

The key, however, is that the SEA of 2025 is a significantly stronger, bigger, and more profitable franchise that is back to double-digit growth rates, kind of the ideal growth stock we’ve become accustomed to with the likes of MELI, whose own growth continues unimpeded alongside SEA. They’ve shown that sustainable profitability and robust growth can coexist.

Shopee had record gross orders, Monee had record revenues and Garena had the best quarter in 4 years. The market has just seen what can happen when all of SEA’s engines fire on all cylinders. I imagine Forrest Li kicking back after this ER, turning on the TV and nodding his head along to this piece of cultural history:

Quality Score

Personal conviction: 9/10 (unchanged)

Profitability: 9/10 (unchanged)

Sales efficiency: 10/10 (unchanged)

The sales efficiency was up, but above 10/10, so you don't see it. But margins were higher (46.5% from 44%), marketing spending as a percentage of revenue lower (19.2% from 21.2%). What's not to like?

Innovation: 4.5/5 (unchanged)

Must-have?: 4.5/5 (unchanged)

If there are 3 billion orders in a quarter... you know that the company is seen as a must-have. Half a point off from a perfect score because of Garena, which is less of a must-have.

Revenue growth: 5/5 (unchanged)

29.6% revenue growth? No doubt, 5/5.

Durability of growth: 9/10 (unchanged)

Sea has now proven that it can push the buttons it wants: profitability or growth and now both together. That bodes well for the future.

Management quality: 10/10 (unchanged)

There was a ton of negativity about Sea, but I always said that management was impressive. And great management makes the company.

Insiders' ownership: 5/5 (unchanged)

Multibagger potential now: 4/5 (unchanged)

TAM & SAM: 5/5 (unchanged)

Financial Strength: 8/10 (unchanged)

Risk (negative): 2/5 (unchanged)

Competition (negative): 3/5 (unchanged)

Dilution (negative): 3/5 (from 4/5)

4/5 was probably a bit too harsh. But 3% dilution is still a bit high for my taste.

Scale advantages shared (-5/+5): 5 (up from 4/5)

The reason I raised this score to the maximum is because of the cross-selling of the different platforms that kicked into a higher gear.

Conclusion Quality Score

Sea's Quality Score jumps from 79 to 79.5. That too shows an impressive turnaround. At the lowpoint, the Quality Score was just 61. Still not awful, but 79.5 is much better, of course.

So, for reasons of quality, you shouldn't refrain from buying Sea's stock. How about the valuation? Let's check that.

If you want to read the rest, you can upgrade your subscription from free to paid).