Hi Multis

Cloudflare (NET) reported its Q1 2026 results on May 7. I didn’t find the time to cover them right away and then I saw that it had its annual Investor Day on June 9. I waited a bit so I could cover both in one article. And here it is.

We’ve owned Cloudflare since I picked it at $39 in 2020, and that definitely helped me to unpack everything and put certain things in perspective.

Let’s walk through the numbers first.

The Numbers

Revenue: $639.8M, +34% YoY. That’s the same growth as Q4. It beat the consensus of around $622M by about $17M or 2.7%.

Non-GAAP EPS: $0.25

Non-GAAP operating income: $73.1M, or 11.4% of revenue, up from $56.0M a year ago.

Free cash flow: $84.1M, up from $52.9M in Q1 last year.

Free cash flow margin: 13%

RPO: $2.543B, +36% YoY. RPO is the remaining performance obligation. That’s revenue already under contract but not yet booked because the service still has to be delivered.

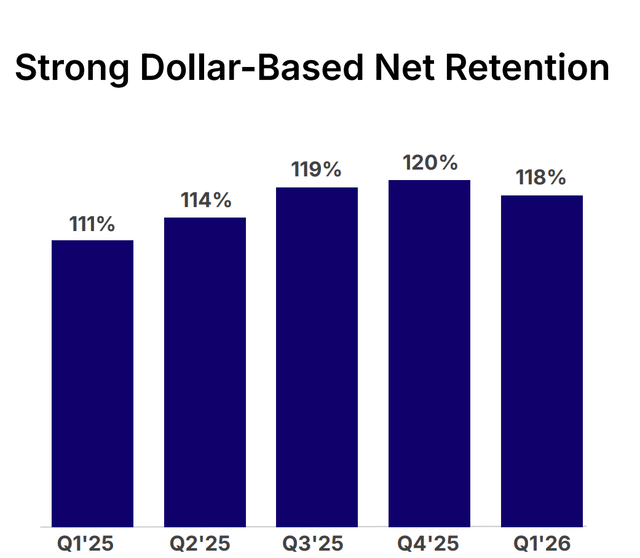

DBNRR: 1118%. (dollar-based net retention, how much customers Cloudflare had a year ago are spending now, including the churn of customers that stopped).

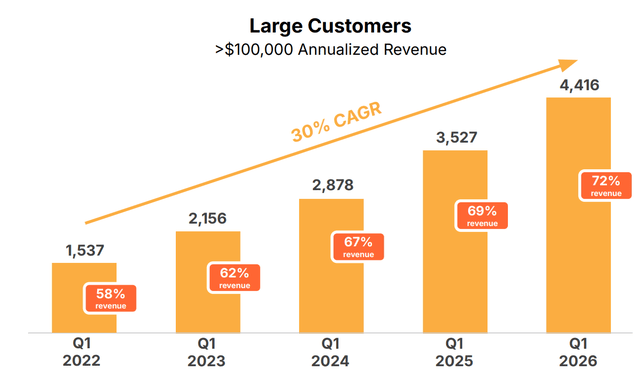

Large customers (over $100K a year): 4,416, +25% YoY. This is now 72% of revenue, up from 69% last year, and grew by 38%.

Very large customers: deals over $1M grew 73% YoY. Cloudflare added as many $5M+ customers in this quarter as it did in all of last year.

Cloudflare has said on multiple occasions that investors should not focus on the DBNRR, but I still read a lot of takes saying it was bearish that DBNRR dropped from 120% in Q4 to 118%.

Cloudflare said that its sales teams focused on new businesses, and not as much on the expansion of existing customers. But still, retention was great.

Founder and CEO Matthew Prince on the call:

Our quarterly gross retention reached its highest level in four years, reinforcing that customers understand Cloudflare is a must-have rather than a nice-to-have.

Gross retention is different from dollar-based net retention. It looks at what you had in revenue from your customers last year and you withdraw all the churn of customers who left, but you don’t count what they spent more. So, the maximum is 100%. The highest gross retention in four years means very few customers are leaving.

The focus on new customers paid off. New business grew at its fastest rate since 2023.

Guidance went up as well. Management raised the full-year guidance to $2.805 billion to $2.813 billion, about 30% growth at the midpoint. For Q2, Cloudflare guided to $664 million to $665 million, also around 30%. I’m pretty confident the real result will be higher.

Also important: network capex is expected to be 14% to 15% of revenue for the year, which is still almost nothing compared to the tens of billions the hyperscalers are investing into data centers. And knowing this team, they’ll probably beat all of it.

The 20% Layoff

On the same day it reported this quarter, Cloudflare also announced it was letting go of about 1,100 people, about 20% of the company. That’s the news that made all the headlines, and I understand why it shocked people.

A company growing 34% laying off a fifth of its employees sounds bad. But when you look at what Cloudflare said about this, and at what it has been doing internally, it’s a very different story.

The cuts hit every function and every part of the world, with one exception: the salespeople who carry a quota and sit in front of customers. Those were barely touched, and management still expects its sales capacity to grow this year. The whole reorganization will cost $140 million to $150 million (about $40 million of that non-cash), mostly in the second quarter, and it should be done by the end of the third. The free cash flow targets for the year didn’t change.

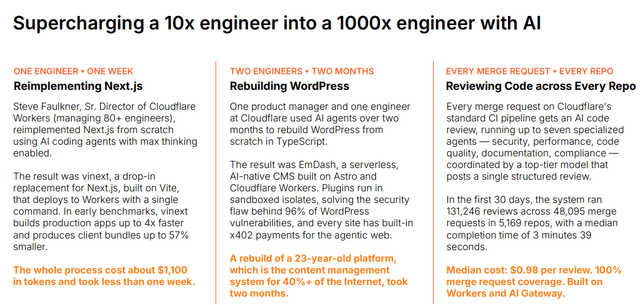

So why do this now, when things seem to be going well? Because Cloudflare has ramped up the use of its own AI tools internally for the last six months. The results convinced management to act.

Cloudflare has been pretty cautious with AI internally, but that changed in November. Since then, people suddenly got much more productive, in some cases two times, ten times, even a hundred times as productive. Matthew Prince described it in his typical colorful language:

It was like going from a manual to an electric screwdriver.

The numbers the company shared were impressive. Cloudflare’s use of AI is up more than 600% in three months. In engineering, 97% of the team now uses AI coding tools, all of them running on Cloudflare’s Workers platform. People in finance, HR, and marketing all use AI intensely. That’s on an internal system the company built and calls Cloudflare OS. On the Investor Day, a few interesting examples were given.

The layoff is the consequence of that. Prince was clear about what it was and wasn’t:

This isn’t a cost-cutting exercise or an assessment of individuals’ performance.

To me, this is a clear signal that the second AI wave has begun. The first wave of the AI boom rewarded the companies that built the data centers, the chipmakers and memory suppliers. A lot of that (but maybe not everything) is now priced in. The next wave will reward the companies that take all that AI and turn it into real earnings by changing how they operate. Cloudflare is one of the first to do that systematically.

It also helps to compare this to the other layoffs we’ve seen this year. Plenty of big technology companies have cut staff, but most did so because they had to. Often, that was to compensate for their enormous data center investments. Cloudflare cut while growing 34% and raising its guidance. That’s a very different situation. And it’s actually a very good thing to do.

The other thing I appreciated was the honesty. Cloudflare paired the layoff with what it called industry-leading severance, and instead of hiding behind the usual corporate language, Prince called it a hard day and said the people leaving will go on to build great things. He also made clear this isn’t a company shrinking. He expects to have more employees in 2027 than at any point in 2026. When an analyst asked why he would do this right after such a strong quarter, he put it like this:

We’re the fittest we’ve ever been, but we’re gonna get even fitter to win the next chapter.

I respect this move a lot. I’m sure Cloudflare will take on many more employees once the new system is in place. Right now, there’s overcapacity. But the companies that will win over the long term are those that can leverage the efficiency gains at a larger scale and I think Matthew Prince knows this better than anyone else.

Sales productivity went up year-over-year for the ninth quarter in a row. Hiring of new salespeople grew at its fastest pace since 2023. We already saw that customer bookings grew the fastest since 2023. They also filled the pipeline at the fastest pace in five years and beat their internal plan for the quarter by more than they have in any first quarter since 2021, during that crazy COVID peak.

The customers keep getting bigger, too. Large customers now make up 72% of revenue, up from the high 50s a few years ago.

The Agentic Internet, Cloudflare’s Biggest Tailwind

Below: Cloudflare’s premium role in the agent traffic, why OpenAI and Anthropic both build on Cloudflare, the "Google Zero" problem of the internet and how Cloudflare seems to be the only one working on a solution, why the dropping gross margin is actually good news. And of course much more, like the valuation.

The value you get for your subscription is priceless!