Hi Multis

At Potential Multibaggers, I'm always looking for the best quality.

For a company like Nu Holdings (NU), I'm always honored that Karan covers the earnings. Karan is a banking expert who works for one of the Big Four US banks.

Unless you are new (hi, there!👋), you probably know the drill by now. First, Karan will analyze the earnings and then I will take over to update the Quality Score and Valuation score to see if the stock is attractive right now.

Hi Multis

Karan here with the update on NU. After the earnings, I saw quite a bit of negativity. We will address that in this article.

I think of NU in the same way as I think of a sailboat in a competition.

(Image generated by Grok, prompted by Kris)

Meticulous preparation of the boat, combined with skillful navigation, but the final outcome also depends on the wind and overall weather, forces beyond their control.

Sometimes, a favorable breeze carries them to record-breaking results; other times, an unexpected storm makes it much harder to reach their destiny, regardless of their efforts.

And this is why, of all the companies I cover, I am most tempted to automate NU’s earnings reports. I imagine a template that says:

NU did well in a challenging macro environment.

Then I should just ask Perplexity to update the earnings numbers and publish.

This way, you only have to read if NU either did poorly or we somehow had a supportive macro environment (which happens once every five years in Brazil, apparently).

I haven’t done it yet, though, so while I will share the numbers later on, I will structure this report a little differently and try to debunk some of the negative points that have been raised since the earnings came out by various people/analysts.

I’ve spoken at length multiple times before about NU’s structurally advantaged business model and amazing execution. All that still holds, so let’s examine the “negatives” first.

Brazil has matured; it’s “game over.”

Funny, I think that NU’s Investor Relations Team heard this and went:

So, for the first time, they produced this chart (it's small, I know, but try to zoom in; it's interesting):

The runway for onboarding more customers might be shrinking in Brazil, but NU's market share is still not high when it comes to revenue; they fully intend to capture and deepen their ARPAC numbers. (Average Revenue Per Customer)

2. After the call, an analyst wrote:

Q1 earnings included a net income benefit of $42M from the usage of deferred tax assets, a non-recurring item. Excluding the gain, Q1 net earnings would have missed consensus by 10%, instead of the 3% miss reported. Adjusting for the impact, earnings would have been $515M for a 7.7% Q/Q decrease.

The implication here is that NU’s earnings are obscured by accounting because they booked a gain on deferred taxes, which is a one-time thing and won’t benefit them again. Ok? The fact is, NU will pay less in taxes and keep more of its cash. It’s not like they swung from a loss to a profit, just that the profit was slightly lower. The reason? A ridiculous headwind from FX moves. Think about our sailboat and headwinds. (More about this later.)

3. He also noted that the company received an initial license for banking in Mexico, but it could take three to five quarters before Nubank can operate fully as a bank.

Lol, “3 to 5 quarters”. So basically Mid-2026? Oh, how would any poor equity holder survive that long?

Of course, if you only look at the next 4 quarters, as most analysts do with their target prices, this is a pain in the behind. Poor analyst, you must be waking up in the middle of the night, screaming and sweating from this nightmare. 😱

The important piece, as highlighted by NU, is the size of the prize waiting in Mexico:

This is not a pipe dream, NU knows how to run a bank, and they have formal approval to do it. Yes, it takes a while to hire staff, train them, get office space and develop processes; that’s just business. The fact is, Mexico will become a meaningful driver of growth moving forward.

4. BofA Securities analyst Mario Pierry pointed to slower revenue growth, higher cost of risk and lower return on equity. He wrote in a note to clients:

The miss reflected a sharper compression in risk-adjusted net interest margin (-120bp Q/Q to 7.0%), mainly reflecting higher cost of risk (17.1% of avg loans up from 15.5% in 4Q), and lower credit spreads (on higher funding costs, weaker loan mix, geographic expansion)," .

The analyst was worried about this chart from NU:

If this is the only thing we saw, we would be worried, their NIMs keep going lower while their Credit Loss Allowances keep going higher. This echoes another point that an online commentator made about how this is bad news from NU, highlighted by Multi Magnus in our Slack community. Quoting from the article he linked to: (NIM = net interest margin)

Gross margins slid from 46% to 41% -- that’s not a rounding error. It’s the lowest in two years.

Net interest margin compressed 20bps to 17.5%, and risk-adjusted NIM fell even further to 8%, its third straight quarterly decline. And this isn’t a one-off anomaly caused by seasonality or credit cycle noise. This is a structural shift.

Nu is pivoting into secured lending and international markets. FGTS loans, public payroll loans, and now private payroll products are the future of its credit book.

(Note: An FGTS loan in Brazil is a home mortgage that uses your government-mandated FGTS ( Fundo de Garantia do Tempo de Serviço) savings as collateral to secure lower interest rates.)

In Mexico and Colombia, deposit franchises are being aggressively built out to fund local growth. But these are lower-margin plays by design. You don’t yield 22% NIMs on government-backed payroll loans. You don’t expand credit safely in underbanked economies without subsidizing your funding base. And you certainly don’t expand cross-border without taking on duration mismatches that pressure spreads.

The problem isn’t that Nu is making these moves -- they’re necessary. The problem is that the market is still pricing this story as if Brazil’s mature unit economics are portable. They’re not. Even management admits that margins in Mexico and Colombia are meaningfully tighter, and profitability there is still “a longer-term story.”

But the longer the company leans into lower-yielding growth to hit customer milestones, the more that long-term story dilutes short-term margin reality.

And yet, the narrative persists. That this is a compounding flywheel. That ARPAC will trend toward $40 like incumbents. That scale will keep outrunning cost. But when gross margins are shrinking, NIM is falling, and CLA (credit loss allowance) is rising -- not stabilizing -- you’re not in a compounding story. You’re in a transition phase. One that demands new pricing models, stricter capital discipline, and recalibrated expectations.

Because here’s the truth: operating leverage doesn’t save you if your revenue per dollar of credit deployed keeps falling. You can have the best CAC in the world. You can serve 60% of a country. But if your incremental dollar of income comes with tighter spread and heavier provision, the ROE math breaks. And with $4B+ in excess capital sitting idle, the optics start to shift from optionality to inefficiency.

That sounds so scary. We should all be rushing to short NU. Like NOW!

But before you do, let's first look at this. Because it's a piece of art, an outstanding specimen of a word soup, spiced with some jargon and selectively (!) using some data to create a story that's the investors' equivalent of A Nightmare On Elm Street.

The only problem with this word soup is that it falls apart after just 30 seconds of research. By the way, I added the white lines. It was one block of text, and it was already bad enough to feed you.

But back to the 30 seconds of research. I present to you Exhibit A:

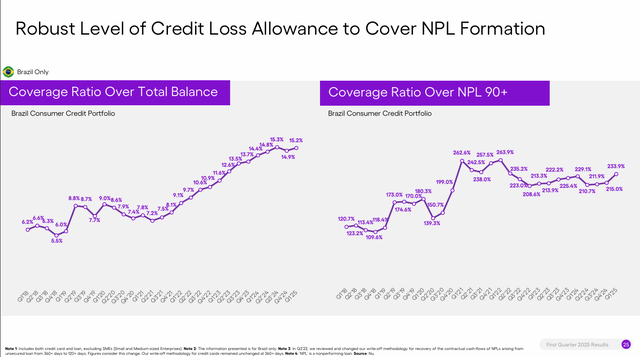

NPL 90+ (basically, people who are 90+ Days past due are lower than in Q1’24, despite originations being 70% higher. And those loans have a return of 15%, would you not take this bet as a business owner?

And with that, here’s Exhibit B:

Funny, 15-90 NPLs (non-performing loans) are at levels last seen in 2021, while NPLs divided by the total balance are also down to 2022 levels, basically telling you the portfolio is growing faster than NPLs, which is excellent news for profitability. Of course, this could also change in 3 months if they all go bad at the same time, but looking at this trend line doesn’t indicate that, does it?

So why are loss allowances going up and scaring poor online commentators? Simple, they’re supposed to, those are the rules of GAAP accounting – Provisions for losses are a dollar figure, calculated by assuming a total portfolio ENR (aka all outstanding balances) multiplied by a loss rate.

So, here’s an oversimplified math example,

A portfolio of 10 billion loses 4% a year; this means you have a credit allowance of $400M.

A portfolio of 17 billion also loses 4% a year, but your credit allowance is now $680M.

Should you panic like this online expert? Or should you refresh your math. It's so simple: NU’s allowances will increase the more they lend, even if they lose less per loan. Let’s move on to Exhibit C:

Surprise, surprise, they had to increase provisions because the portfolio grew so much. But the ratio of losses has gone nowhere, as we see in Exhibit D.

So, the next time you see someone having a panic attack about the increase in credit losses, tell them to keep calm and send them a copy of GAAP accounting.

The other points they raised about NU getting into government payroll loans and secured lending, which offer lower yields, that's true, but they are secured, which means write-offs are also lower and need lower credit provisions. They are also larger in size, so NU can deploy more capital more efficiently as it gets bigger. This is… normal. (Think shrugging emoji here)

As for profitability and NIM declining, he wasn’t the only one complaining.

5.

Also, net interest income decelerated for the seventh straight quarter to 34% Y/Y, he added.

Pierry has a Neutral rating on Nu Holdings.

Yes, the NIM is lower and NU has an explanation for why:

Slightly different picture, isn’t it? NIMs actually INCREASED in Brazil, which is supposed to be the mature market, while they contributed negatively in Mexico and Colombia, where NU is offering enticing rates to sign up new customers.

It’s called Investing for Growth. It's what you want your growth companies to do. And it's exactly what compounders do. If anyone thinks it’s a permanent problem, I point you to Brazil, which has expanded after 12 years of operations because NU has captured most of the adult population and is super-efficient.

6. J.P. Morgan analyst Yuri R Fernandes, wrote:

Our initial assessment is mixed as adjusted figures are 9% below company-provided $561M consensus, but not as negative as initial after market performance indicates." Net interest margin compressed to 17.5% from 17.7% in Q4 2024 and 19.5% in Q1 2024, but stabilization "appears near," he said. J.P. Morgan has an Overweight rating on NU.

Least offensive in my view. All I have to say to all these people is look at the magnificence of this chart:

Repeat after me. “I will not panic about a few quarters of NIM compression.”

I was taught that when a business keeps increasing the money it makes from each customer, growing its customers at a high rate, all while continuously lowering the price of serving those customers, it creates a flywheel of operating leverage that cannot be beaten. We have no signs that there is anything wrong with NU’s business model. To the contrary. Don't let the short-term-minded analysts distract you.

That’s enough bear dunking for one day. If you’re still here, read on for the victory lap.

Q1 2025 Key Highlights

If you are not a paid subscriber, it stops here for you. I hope the debunking of the negative comments was useful for you.

Want to continue to read the analysis and know if Nu’s stock is attractive now?

It’s your lucky day!

It’s 20% off now.