Hi Multis

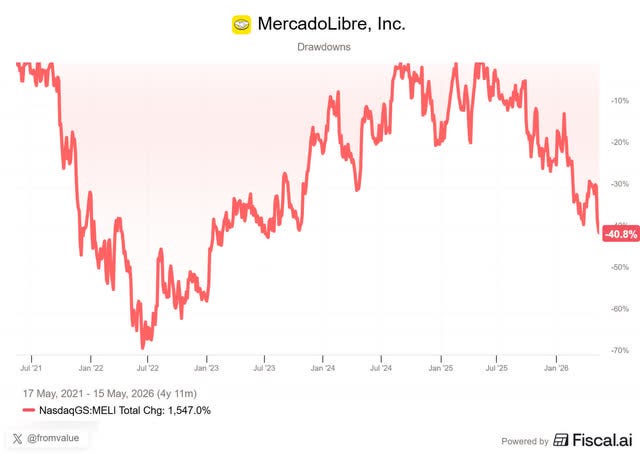

Last Thursday, Mercado Libre (MELI) reported its Q1 2026 earnings. On Friday, the stock dropped close to 13%. Right now, MELI is down more than 40% from its 2025 high.

So, the market hated the earnings. Let me tell you up front: I loved them. And I love the market’s hate.

I’m going to explain why in this article. If you are a long-term investor and I do my job well, you will probably love it as well.

Let’s go through the numbers first.

par Mercado Libre - Télécharger sur PHONEKY")

The Numbers

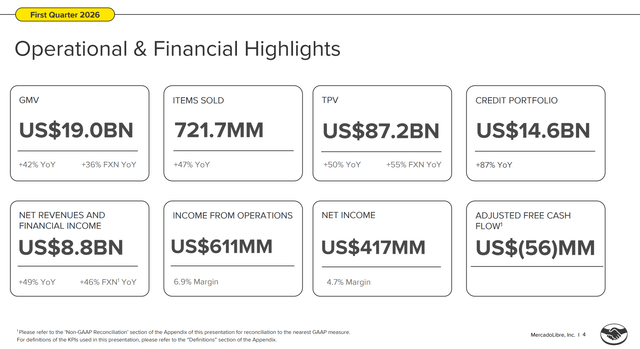

Revenue: $8.85B, +49% YoY in USD, +46% FX-neutral, beating estimates by $530M

EPS: $8.23, missing estimates by $0.24

Net income: $417M (-16% YoY)

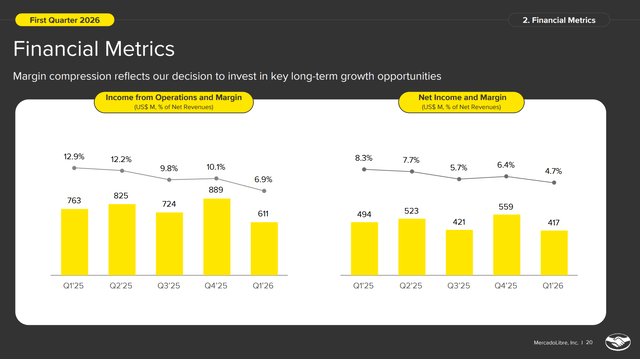

Operating margin: 6.9%, down 600 bps YoY

Adjusted free cash flow: -$56M

I’m sure you are not impressed with some things here, like the FCF, for example, or net income down 16% YoY, margins down from 12.9% to 6.9%. And that’s already an important part of what the market hated about this quarter. Much more about this later and why I love it. Let’s first look at the different segments.

Marketplace:

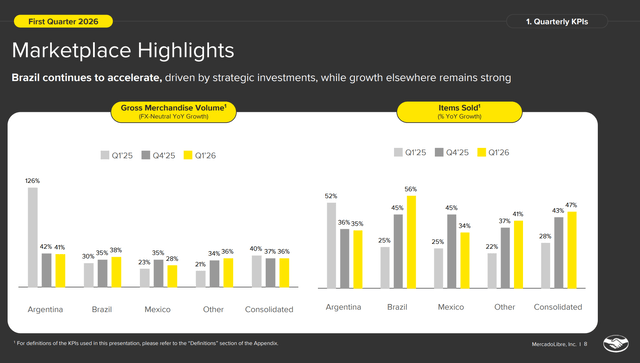

GMV: $19.0B, +42% YoY, +36% FX-neutral

Items sold: 722M, +47% YoY

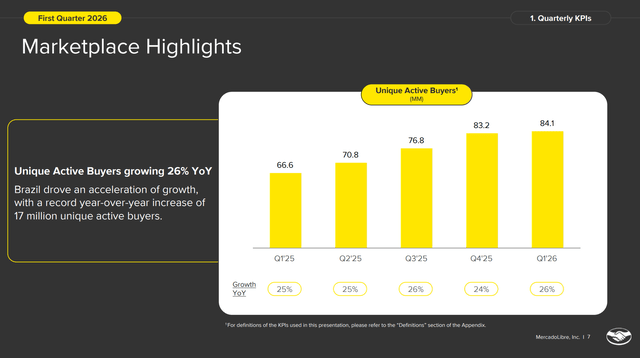

Unique active buyers: 84.1M, +26% YoY, a record addition of 17 million in a single year

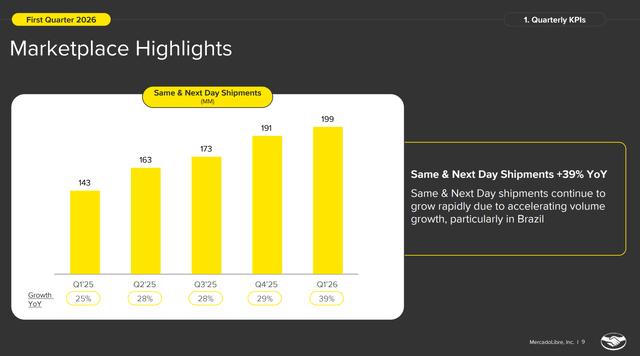

Same- and next-day shipments: +39% YoY, accelerating from +29% in Q4

Mercado Pago:

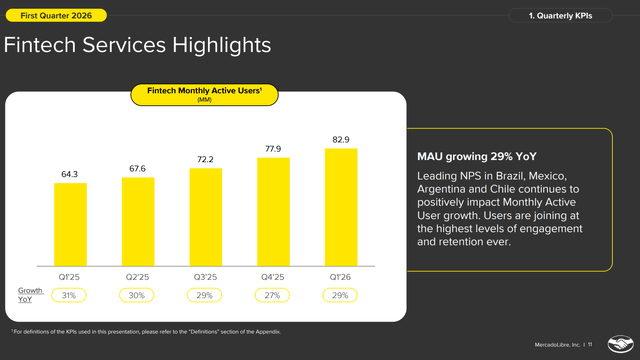

Monthly active users: 82.9M, +29% YoY

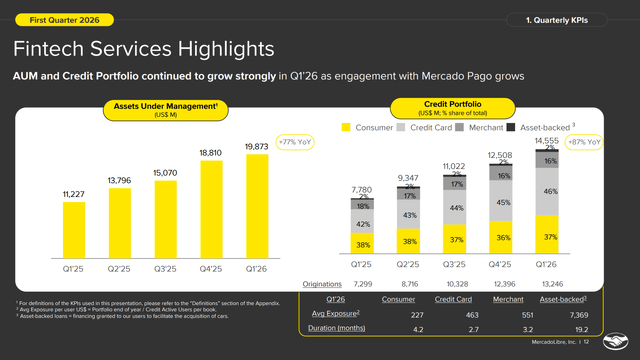

Assets under management: $19.9B, +77% YoY

Credit portfolio: $14.6B (+87% YoY, the largest nominal quarterly increase ever)

Credit cards issued in Q1: 2.7 million

Credit card portfolio: $6.6B, +104% YoY

Advertising: +73% YoY in USD, +63% FX-neutral

To summarize the numbers, this is the overview from the earnings call slide deck.

What The Market Didn’t Like

The market doesn’t like that the operating margin dropped from 12.9% a year ago to 6.9% in Q1. I already pointed that out shortly.

The market doesn’t like that EPS was down for the fourth quarter in a row.

And the market really doesn’t like that NIMAL (net interest margin after losses) compressed from 22.7% to 17.8%, which makes the bearish “the credit book is getting riskier” crowd start typing furiously. And it sounds informed, of course, as most people already have no idea what NIMAL is exactly, let alone what a good or bad NIMAL is. We'll come back to this.

Here is the evolution of margins and net income.

That already looks bad, right? But the margin compression is not a weakness. Management had announced it properly and they broke it down in detail. That breakdown shows the entire compression is the direct, predictable result of investment decisions that are working. In other words, this is not weakness, it’s deliberate investing.

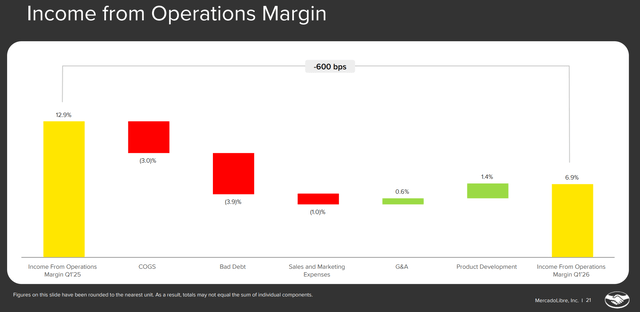

Look at the operating margin waterfall:

The two big red candles are COGS (cost of goods sold) and bad debt.

The two big hits are COGS (cost of goods sold) and bad debt. The COGS went up because of more free shipping in Brazil and the rapid growth of the 1P business (first-party, meaning the products Mercado Libre buys and sells itself, as opposed to the 3P marketplace business where merchants sell on the platform). Both are very deliberate investments.

The bad debt was up because the credit portfolio grew 87% YoY, and management explained in detail how this works. When Mercado Libre writes a new loan, accounting rules require it to immediately provision for the full expected lifetime loss on that loan, before it has collected a single dollar in interest.

Two thirds of the 3.9 percentage points of bad-debt compression comes from this requirement. If your credit book is growing so fast, that accounting rule alone will compress margins, and it tells you absolutely nothing about whether credit quality is deteriorating or not.

The other third of the margin compression has a different explanation. Management extended the duration of personal loans in Brazil from 5 months to 8 months. They also broadened the reach of consumer credit.

Again, both decisions require taking higher provisions upfront. But this is not management being reckless. As Fintech President Osvaldo Giménez explained on the call, the goal is to reach customers who were offered a credit line in the past and didn’t take it. By lowering the spread and extending the duration, MELI can activate this group. The early signs are encouraging.

Two parts of the income statement improved this quarter. Product Development expenses dropped from 9.3% of revenue to 7.9%, mostly thanks to AI productivity gains. G&A (general and administrative expenses) also came down as a percentage of revenue, for the same reason.

In other words, there is no “weakness” here. Every single basis point of margin compression came from deliberate investment decisions, not from anything that’s getting worse in the underlying business. To the contrary.

I can’t stress enough how important that is. Margin erosion is a problem if it’s not announced or not deliberate. Mercado Libre has gone through multiple investment cycles before. Don’t forget that it didn’t have a distribution arm first, but over the last decade, it built by far the best delivery network in LatAm, beating Amazon at its own game. If you were already following the company a decade ago, the negative comments you hear now must sound very familiar.

Brazil Is On Fire

Last quarter, I wrote about how the lowering of the free shipping threshold in Brazil from R$79 to R$19 was working. This quarter, it’s working even better than last quarter.

Let’s look at the last four quarters of the growth of items sold in Brazil:

Q2 2025: 26%

Q3 2025: 42%

Q4 2025: 45%

Q1 2026: 56%

Four quarters of incredible acceleration. The growth rate has more than doubled from the level before the shipping fee change.

Total GMV in Brazil grew 38% FX-neutral, also accelerating. Unique buyer growth accelerated to 32% YoY, the fastest pace since the pandemic.

On top of that, the economics keep getting better, not worse. Unit shipping costs in Brazil dropped 17%, accelerating from the 11% decline we already saw in Q4.

Even better, roughly half of the profitability hit MELI took when it lowered the free shipping threshold has already been recovered. How? Through scale, productivity gains, efficiency improvements, and some smart pricing adjustments. Several categories below R$79 are now breaking even on a unit basis, less than a year after the change. That’s much faster than expected and once more a testament to the relentless execution of this company.

I want to show you a quote from CEO Ariel Szarfsztejn that I think captures what’s really happening here. I love that first sentence.

Free shipping has always been a long-term investment in user behavior, not a short-term promotional tool.

When we launched it in 2016, it took time for unit economics to improve enough to offset the investment but the compounding impact on engagement and scale validated the decision.

Today, like in 2016, the signals we see give us confidence: user behavior is responding as we expected, and unit shipping costs are falling faster than we had anticipated.

Mercado Libre has done this before. They have the experience and they know what metrics to look at. Does that sound like a company crushed by competition that has to give up margins? Not to me. You can’t have it more deliberate than this.

The buyers who have joined since the shipping fee threshold change are buying more items across more categories with higher retention than the cohorts that came before. Daily active users are growing faster than monthly active users, which means users use Mercado Libre much more often.

Conversion, frequency, retention, and NPS (net promoter score, how satisfied customers are) are all at record highs. Tell me: does this sound like a victim or a winner?

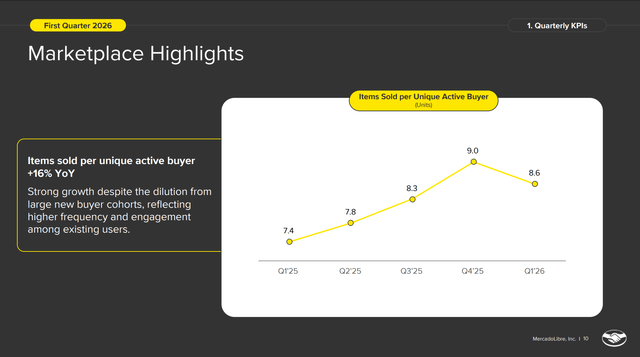

If you see the small slide in the items sold per unique users QoQ, that’s seasonality from Q4 to Q1. It’s really impressive that items sold per unique active buyer don’t slide more and are up YoY, as the company added a record number of new customers, and usually, new customers have fewer orders. Another sign of strenght.

By the way, this is happening in a market where Sea’s Shopee is also accelerating. Some bears love to say that Shopee is going to eat MELI’s lunch in Brazil. As you know, I’m a long-term shareholder of both companies and I think both can do very well.

Latin America is still in the very early days of e-commerce adoption, and as the market continues to grow, there is more than enough room for multiple strong players.

Just look at this chart that MELI has on its website. LatAm is literally at half the e-commerce penetration of the US and at 38.5% of that of China.

Also important: MELI’s conversion rate in Brazil is up 1 percentage point YoY. Conversion rate is the percentage of visitors who actually end up buying something on the platform. A 1% improvement may sound small until you consider the size of the platform. If MELI has, say, 100 million visitors a month, that 1 % extra conversion improvement means 1 million additional buyers per month.

The Logistics Moat Keeps Deepening

I want to underline two numbers that I think don’t get enough attention.

The first is 95.5%. That’s the share of all Mercado Libre’s deliveries that now go through its own logistics network. In other words, when you order something on MELI, there’s a 95% chance the package is moving through MELI’s own infrastructure at some point on the way to your door. The other 4.5% goes through external delivery services.

The second number is 55%. That’s the share of shipments that come from Mercado Libre’s own fulfillment centers, meaning warehouses where MELI is storing the seller’s inventory, similar to Amazon’s FBA. The remaining 45% ships from the seller’s own (ware)house, but still moves through MELI’s logistics network from there.

Think about what these two facts combined mean. When you control 95% of your own delivery infrastructure and your unit shipping cost drops 17% in a single year while your shipment volume shoots up like a rocket, that is devastating for competitors that are paying third-party logistics rates.

Each additional package Mercado Libre handles makes its network cheaper to operate. Each additional package a smaller competitor ships through a third-party logistics network costs them about the same as the previous one. And, as Mercado Libre is the biggest by far, all competitors are smaller.

Same- and next-day shipments accelerated to +39% YoY, after running in the high 20s for four straight quarters. The customer experience is getting visibly faster at the same time that volume is exploding.

The company is also building a new 100,000 m² (more than 1 million sq ft) fulfillment center in Argentina, the largest in its network. It will open in late 2026. You see that management is still investing in its infrastructure investments as well.

Mercado Pago: The Real Story Of The Quarter

If you want to understand why this quarter matters, you have to understand Mercado Pago. The fintech segment grew 54% FX-neutral. AUM hit $19.9 billion. Monthly active users came in at almost 83 million, with MELI adding nearly 20 million users in a year. That’s about the population of Chile and more than that of many countries.

I want to expand a bit on the credit portfolio because that triggered a lot of headlines. The portfolio grew 87% YoY to $14.6 billion, and management noted this was the largest nominal quarterly increase ever. Of that $14.6 billion, $6.6 billion comes from the credit card book, now up 104% YoY. It now accounts for 46% of the total portfolio, up from 42% a year ago. The company issued 2.7 million new credit cards in Q1 alone. Pretty impressive numbers.

Here’s how CEO Ariel Szarfsztejn framed it in the shareholder letter:

Investing in our credit card is as pivotal for Mercado Pago as the launch of our managed logistics network was for our marketplace ten years ago. Just as fulfillment was a critical element of achieving market leadership in Commerce, the credit card is central to our ambition of being the region’s largest digital bank.

That’s a big claim but I take it seriously.

Older credit card cohorts in Brazil have been profitable on a NIMAL basis for some time, and they’re now generating enough profits to offset the dilution from the massive new cohorts being added.

In Mexico, where the credit card was launched about two years ago, the cohorts are performing even better than in Brazil at the same time. In Argentina, where MELI launched cards in mid-2025, the early data looks very promising as well, in line with the data in Brazil at the same time after launch.

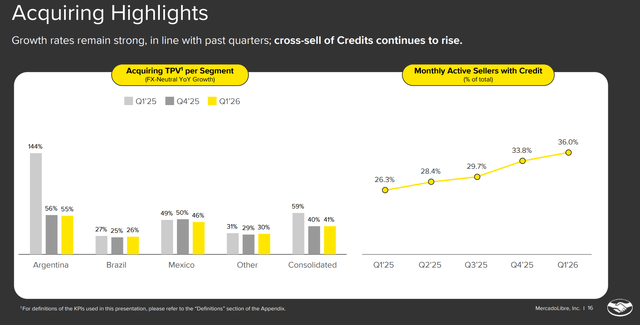

This is the cross-sell working very well. If someone has a Mercado Pago credit card, it increases the marketplace conversion, the GMV per user, and the number of transactions in MELI’s ecosystem.

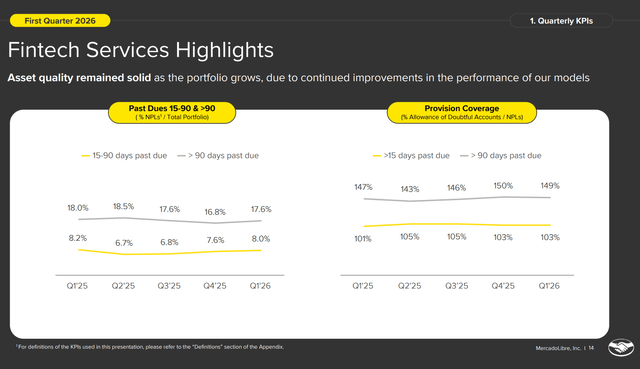

Even better, the 15-90 day NPL ratio (non-performing loans) for the credit card book actually fell 80 basis points YoY. So while the book more than doubled in size, the asset quality got better, not worse. That’s impressive!

The credit card also has the shortest duration of any product in the portfolio at just 2.7 months on average, which means MELI can adjust quickly if the macro conditions change. That’s important. If conditions deteriorate, MELI can stop issuing new cards, and within just a few months, the existing loan book will be largely paid off. With long-duration loans, you’re stuck with the credit risk on your balance sheet for years. The short duration of credit cards is a built-in safety mechanism that many bears don’t seem to understand.

Now about that NIMAL compression. Quick reminder: NIMAL stands for Net Interest Margin After Losses, which is essentially the profitability of the lending business after accounting for credit losses.

For comparison, Itaú, the largest traditional bank in Brazil, has an NIMAL of 6%. So even after this quarter’s compression, MELI’s 17.8% NIMAL is roughly three times that of a traditional bank. Boom! As it’s AL (after losses) that means the risk is already taken out.

The drop from 22.7% to 17.8% YoY looks scary at first glance, and many have pointed to it as a major issue. It’s not, as we already saw. Two thirds comes from the regulatory provisions, a third from the extension of loans from 5 to 8 months and lower spreads for better-quality customers.

Fintech President Osvaldo Giménez on the call:

We’re not trying to seek out riskier folks. We’re reaching out to customers who had a line of credit in the past and they were not taking it. So we are lowering the spread to see if we entice them to start trying our personal loan products.

And the asset quality data backs this up. The 15-90-day NPL remained at 8.0%, broadly stable YoY. Provision coverage stands at 103% for 15+ days past due and 149% for 90+ days past due.

In Argentina, where the broader financial system is seeing rising delinquency, MELI’s 15-90 day NPL actually fell QoQ while spreads increased. That’s not how a credit book under stress looks like, to the contrary.

Do you remember that I mentioned last quarter that MELI was sitting on close to $19 billion in AUM but wasn’t yet using those deposits to fund its lending? Well, AUM is now $19.9 billion and growing 77% YoY, faster than MAU growth (29%). That means existing users are keeping more money with MELI, not just that new users are signing up. This remains a competitive advantage Mercado Libre chooses not to use yet, but I’m sure they will do it one day.

Mexico, Argentina, And The 1P Milestone

Mexico’s items sold grew 34% and FX-neutral GMV grew 28%, still ahead of the market but slowing QoQ because of a tax reform for small and medium sellers. Argentina delivered 41% FX-neutral GMV growth on top of a very tough comp, with items sold up 35%. Chile delivered 40% FX-neutral GMV growth.

TPV (total payment volume) grew 41% FX-neutral in total, with Brazil at +26%, Mexico at +46%, Argentina at +55%, and Chile at +69%. Mercado Pago is taking market share in every market and growing like weeds. Tap to Phone, which is growing by triple digits in Brazil, just launched in Mexico.

There’s another milestone worth highlighting: the 1P business. Quick reminder: 1P is when Mercado Libre buys inventory itself and sells it directly to customers (as opposed to 3P, where merchants sell on the platform). It’s how Amazon started and still accounts for a big part of its revenue. Mercado Libre does this in categories where there’s not enough competition to drive prices down.

Last quarter, I mentioned that 1P had reached positive direct contribution in 2024. That means that for every product MELI buys and sells through 1P, the revenue from that sale covers all the direct costs tied to it (the cost of the product itself, shipping, handling, payment processing, and so on). In other words, each individual 1P sale was finally making money on its own, before any allocation of broader company overhead.

This quarter, management said that some of the categories MELI entered first with 1P are already fully profitable after less than two years. It means 1P is no longer just a margin drag, but is becoming a contributor to profits in mature categories. The rest of the categories should follow as they scale up too.

The numbers are getting really impressive. 1P grew 69% FX-neutral and now generates almost $5 billion in GMV (gross merchandise volume, the total value of goods sold on the platform). An example. Three years ago, MELI had just a 12% share of the cellphone market in Brazil. Today, MELI is the market leader with roughly three times that share. In three years, MELI tripled its share in a category it was barely competing in. That is the power of 1P used well.

The Ads Engine

Advertising grew 73% YoY in USD and 63% FX-neutral. MELI doesn’t break out advertising as a standalone revenue contributor, but TTM ad revenue is now estimated to be about $1.7 billion, up from around $1.55 billion at the end of 2025. This is the highest-margin business in the entire company, and it grew four times faster than the LatAm ad market in 2025.

There’s a structural story behind this that’s worth understanding. Traditional offline channels still account for roughly half of the Latin American ad market, versus about a quarter in the US. As those budgets shift to digital, Mercado Libre is capturing a huge share of the growth, because nobody else in the region has its combination of huge audience, deep first-party data and strong performance attribution.

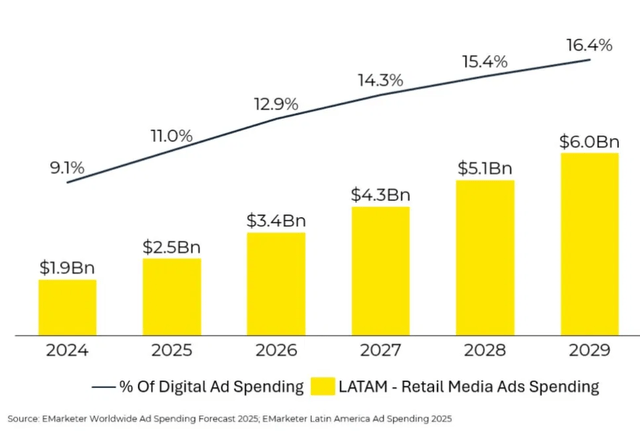

eMarketer projects LatAm retail media spending to more than double from $2.5B in 2025 to $6.0B by 2029, and even at that level, retail media’s penetration of digital advertising in LatAm will be just 16.4%, versus a 22% global average today.

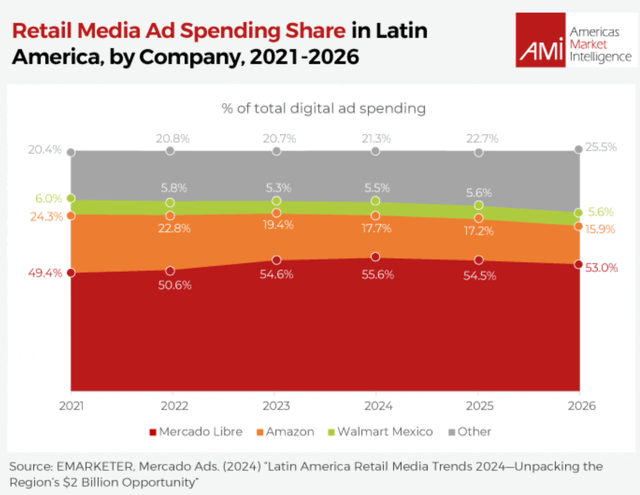

But it goes much faster than eMarketer thought just two years ago. Then it saw a $2 billion market in 2026. And guess who’s got the biggest market share by far, with over 50%? You guessed it.

As you can see, Mercado Libre has actively taken market share from Amazon in something seen as one of Amazon’s core competencies: advertising. Impressive.

The new AI-powered search that MELI launched in Q1 will play an important role for advertising. MELI already saw the shift from keyword to LLM search improve both organic conversion and the click-through rate for sponsored listings. The ad engine got more fuel, as it were.

On Agentic Commerce And AI

Speaking of AI, there is a question that keeps coming up: won’t AI agents disintermediate marketplaces?

I’d suggest reading the piece that MELI’s CMO, Sean Summers, published in March in the IR newsletter. His view, which I agree with, is that agentic commerce as currently pitched won’t scale. AI will compress and accelerate the shopping funnel, but consumers want to keep agency over their purchases.

The Amazon Rufus data illustrates this: 40% of holiday sessions used Rufus, and it drove 66% of sales, but Rufus is acting as a really good co-pilot, not an autonomous agent. The conclusion is simple: AI commerce will happen inside existing platforms with the deepest catalogs, richest data, the best AI recommendations, the best fulfillment, and the most trust. That’s exactly what MELI is in LatAm.

If you are still skeptical, talk with someone who uses AI every day, as I did in Omaha. They will tell you how much of the internet is closing down for bots. Scraping has become much harder and that means that internal agents will be much more valuable.

Internally, the AI productivity gains are showing up in MELI’s numbers as well. Tech headcount grew 8% YoY, but productivity KPIs are growing 7 to 10 times faster. Senior engineers who used to spend most of their time reviewing code are now building again, because the AI tools have made review materially less expensive. Code rollbacks are materially lower YoY. Mercado Libre has rolled out Claude Cowork to 31,000 employees, making it one of the earliest large-scale enterprise adopters globally.

And we’re already seeing the impact in the numbers. Remember when I said earlier that Product Development expenses dropped from 9.3% of revenue to 7.9%? That 140 basis points of leverage is MELI doing more with the same engineers, thanks to AI. It’s already a real, measurable contributor to the operating margin.

The AI Assistant in Brazil is also worth a mention. It now identifies funds held at other banks (via Open Finance) that could earn a higher yield with Mercado Pago and can act on those opportunities within seconds, moving balances between accounts. The Seller Assistant’s daily active users grew more than 40% month-over-month in March.

Below the paywall: my updated PMQS score, my valuation work, the updated Selling Rules, my Buy-Hold-Sell call. If you want this premium content, feel free to subscribe!