Hi Multis

Karan here.

Confession time: I’ve been working on this article for 3 weeks. Why did it take so long?

The first version was a comprehensive review of the company’s earnings and how well they did, considering their challenging environment. I probably would have published it, but when I fall asleep proofreading my own article, it’s probably not fun for the rest of you to read it.

The second version was focused on the state of the insurance industry, I found great company with the analysts on the earnings call - but it turned out that the company was navigating most of those pressures just fine. Also, it was still pretty boring.

To a certain extent, this is the nature of the company’s business – insurance is hard to understand and boring most of the time – but writing about it for a generalist audience can be even worse. Where do we draw the line between detail and noise?

So, this is the third attempt, written more directly and simply, and I hope, gets the job done. It’s also the shortest, because I’m trying not to bore our loyal readers.

A quick recap, Kinsale Capital Group (KNSL), Inc. operates as a specialty insurance company focusing on the excess and surplus lines ('E&S') market in the United States. E&S is a catchall term for “hard-to-price risks”.

And so, in other words, the company provides customized insurance solutions for complex and hard-to-place risks. This includes stuff like property, casualty, and specialty risk insurance products, but targeted mostly at small to mid-sized businesses (which they defined as having gross revenues between $1 million to $50 million annually).

These businesses are generally high-risk commercial enterprises and emerging market segments, including transportation, construction, environmental services, and hospitality.

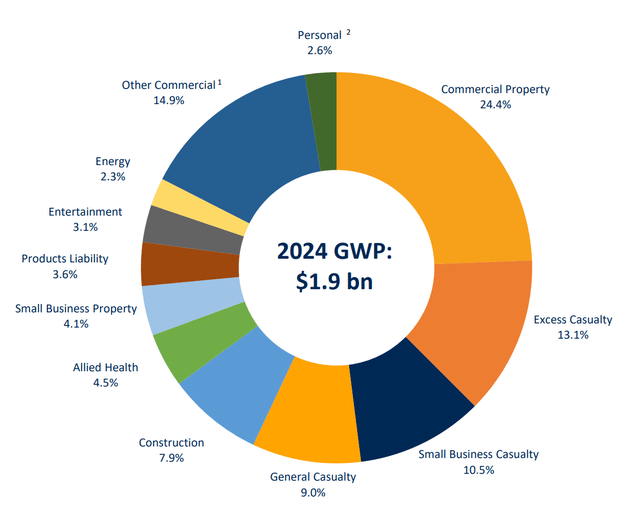

This is how the customers are split up between different industries.

Source: Kinsale's Q4 2024 Earnings Call Slides

This works out to about 15,000 commercial insurance clients, sold mainly through a network of independent brokers.

You and I likely can’t walk up to Kinsale to buy life insurance (yet, see further), which is why most never have, and never will, hear about the company. That's also why it is niche and kind of boring to read about. It’s still barely followed despite crushing the market since its IPO.

Now what makes Kinsale special? After all, there are thousands of insurance companies in the world. To recap the thesis, Kinsale is good at 4 things:

Underwriting Expertise: They are willing to take risks that are complex and too difficult for most.

Technological Innovation: The company invests in machine learning risk assessment, real-time risk monitoring, and cybersecurity risk evaluation to enhance its risk management capabilities. (Obligatory AI reference of course). Other insurance companies don't have 27% of their employees in the tech department, as Kinsale has.

Efficient Claims Processing: Average processing time of 7.2 business days and a 94.6% claims resolution rate. These are some of the best in the insurance industry.

Customer Relationships: The company maintains a retention-focused approach, resulting in an 85% customer retention rate and an average client relationship duration of 7.2 years.

These are all pretty good benchmarks for the US insurance industry, which is widely hated for its byzantine rules and slow claims processing. But Kinsale stands apart, as do its results.

Financial Performance

EPS: Q4 2024 EPS of $4.62 vs the analyst forecast of $4.30. (Beat)

Revenue: Reached $412.12 million, $45 million better than the expectations, a 29.7% year-over-year increase. (Beat)

Net Income: $109.1 million, up from $103.4 million in Q4 2023, while full-year net income surged 34.5% to $414.8 million

Gross Written Premiums: Grew by 12.2% to $443.3 million compared to Q4 2023. Underwriting income was $97.9 million for Q4 2024. For the full year this figure was $1.9 Billion, a 19.2% increase YoY. Net Earned Premiums also grew 21.2% to $359.74 million. They also got a boost of $9.6 million due to releasing reserves from prior years that weren’t realized, showing their risk management.

Net Investment Income: Increased by 37.8% to $41.9 million compared to the same quarter last year.

Combined Ratio: Maintained a strong combined ratio of 73.4% for Q4 2024. (Analysts had estimated 76.3% so this was much better) with a loss ratio of 52.3% and an expense ratio of 21.1%. For the full year, combined ratio was 76.2%, which was steady, but remarkably, this means they performed better in Q4, which bore the brunt of the wildfires, than they did in the year as a whole. Return on Equity clocked in an excellent 29%.

A quick recap of what some of these mean for newer readers or people looking into Kinsale for the first time.

Gross Written Premiums: Total amount of premiums collected from policies issued by Kinsale in the period.

Net Earned Premiums: Portion of premiums actually earned by the insurer after deducting reinsurance and other adjustments.

Expense Ratio: Percentage of the premiums earned goes towards operating costs, such as salaries, marketing, and administrative expenses

Loss Ratio: What percentage of the premiums earned is paid out in claims. If the loss ratio is 52%, it means that for every dollar earned in premiums, 52 cents is paid out in claims.

Add these 2 and we get the Combined Ratio: To over-simplify, it’s a measure of profitability, where a ratio below 100% indicates profit, and above 100% indicates loss. And Kinsale is the best of its peers in E&S.

Source: Kinsale's Q4 2024 Earnings Call Slides

In other words, in Q4 2024, Kinsale collected a $100 from selling policies, at a cost of $21 and ended up paying out $52 in claims on those policies, thereby leaving $27 for the company as profit. Simple right? That’s pretty much the business model – keep most of what you make.

Now, of course, every company says it has competitive advantages over its peers. Fortunately, we can check using standard metrics to see how meaningful those claims are.

For context, there is only one company with a market cap larger than Kinsale and a return on equity higher than Kinsale – Progressive, which dominates auto insurance all across America. PGR’s combined ratio? 89%.

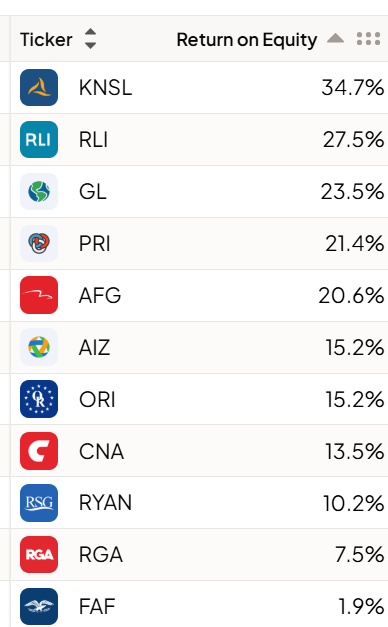

If we use Finchat’s industry filter, specifically for E&S insurers, we see Kinsale is top of the pile when it comes to profitability:

I did a quick scan of these names and not a single one has a combined ratio less than 85%. I believe the technical term for Kinsale is “best of breed”.

Hence, understanding how such a company grows is also a simple matter, broadly it can be done through the following ways:

Raise premium prices – This provides natural inflation protection but can’t be done too aggressively lest they get undercut

Sell more policies to more people – But this must be done at the right price with the right benefits to entice people to take them up

Increase efficiency by reducing expenses and keep more of the premiums (Kinsale is world class at this as we’ve seen)

Invest the float earned wisely and prudently, managing both return and liquidity (Perfected by the GOAT Buffet himself). CFO Bryan Petrucelli expects continued benefits from higher new money yields, averaging in the low 5% range, which should further enhance net investment income moving forward.

Expand into other verticals.

On that note, the company specifically announced expansion plans:

Kinsale plans to expand into personal insurance and adjacent markets, including high-value homeowners' insurance in catastrophe-prone areas.

New Business Unit: Introduced a new agribusiness underwriting unit, focusing on farm, ranch, and related spaces

We see CEO Michael Kehoe’s philosophy in full play here – which is to expand deliberately both vertically (through market share gains) and horizontally (into newer insurance lines)

Now, some may question the wisdom of going into catastrophe-prone areas given how many established insurers are retreating and the frequency of extreme weather events keeps increasing.

Kinsale itself got burned (pun intended) from the Southern California wildfires with $6.2 million in after-tax catastrophe losses for Q4, primarily from the Southern California wildfires. In January 2025, preliminary estimates pegged additional wildfire-related losses at $ 25 million pre-tax.

While this doesn’t sound great, it’s the point of insurance – you pay out when bad things happen, but collect a fortune to protect against them at all other times. Ironically, with more established insurers retreating, it would likely make it more lucrative for those willing to step into the void and offer hard-to-price insurance in disaster zones, as long as they can make the math work. For example, the initial loss estimates were actually $45 million, but KNSL had re-insured about half that amount and hence ended up with only $25 million in losses. That’s excellent risk management, without a doubt.

The other risk to worry about is as Kisnale moves away from niche areas into more “mainstream” categories like personal insurance, the field gets quite crowded quite quickly. Expenses go up because you have to market aggressively, pricing goes down because there are plenty of cheaper alternatives and hence margins get hit. So, it will be interesting to see how the company can navigate these challenges.

Despite strong results, the stock sold off 6% on the day. My best guess here is because Gross written premium growth decelerated to 12.2% in Q4 from 19% in Q3, this is clearly a result of increased competition, particularly in larger property accounts, which impacts premiums, and was clarified by the company in the call.

Will this continue? We will have to see, that said, the company maintained its outlook of 10-20% growth in gross written premiums over the long term. Until this is disproven, we have no reason to believe otherwise.

As CEO Kehoe asserted: “Our model is built for cycles, not quarters”— that’s a great line and one that I hope will bear out for years to come.

Conclusion

Not every business is like the Trade Desk, where the CEO gives masters level theses on the earnings call or innovates at the cutting edge of ad tech. And because so many people follow it, we see the stock routinely having a 50% move at least once a year. In contrast, Kinsale is a very simple, but equally well-run business. A boring one, and that’s a good thing in this case.

Most of the earnings call (and I encourage everyone to listen) consisted of analysts worried about, if not outright sceptical of competition and pricing pressures. I totally understand where they’re coming from, but this line of questioning suffers from the same problem as my first 2 attempts at this article – the tendency to overcomplicate something simple but complex drivers. It’s really exciting to model in a wildfire or hurricane impact or re-insurance rates or distribution of small casualty accounts. I’m kidding, but professionals get paid to do this for a living and so have no choice but to ask questions about them.

Fortunately, we have a founder CEO that has spent a long time making things simple and continues to show results through consistent execution. Kinsale remains confident in their growth projections and their expense outlook, and if those 2 hold up, the rest is just simple math.

That’s what we should all be focused on and hopefully this is a lesson I will remember next time.