HIMS: The Numbers Looked Bad. The Business Got Better

It looked like a mess (until I dug deeper)

Hi Multis

On Monday, Hims & Hers (HIMS) reported its Q2 2025 earnings.

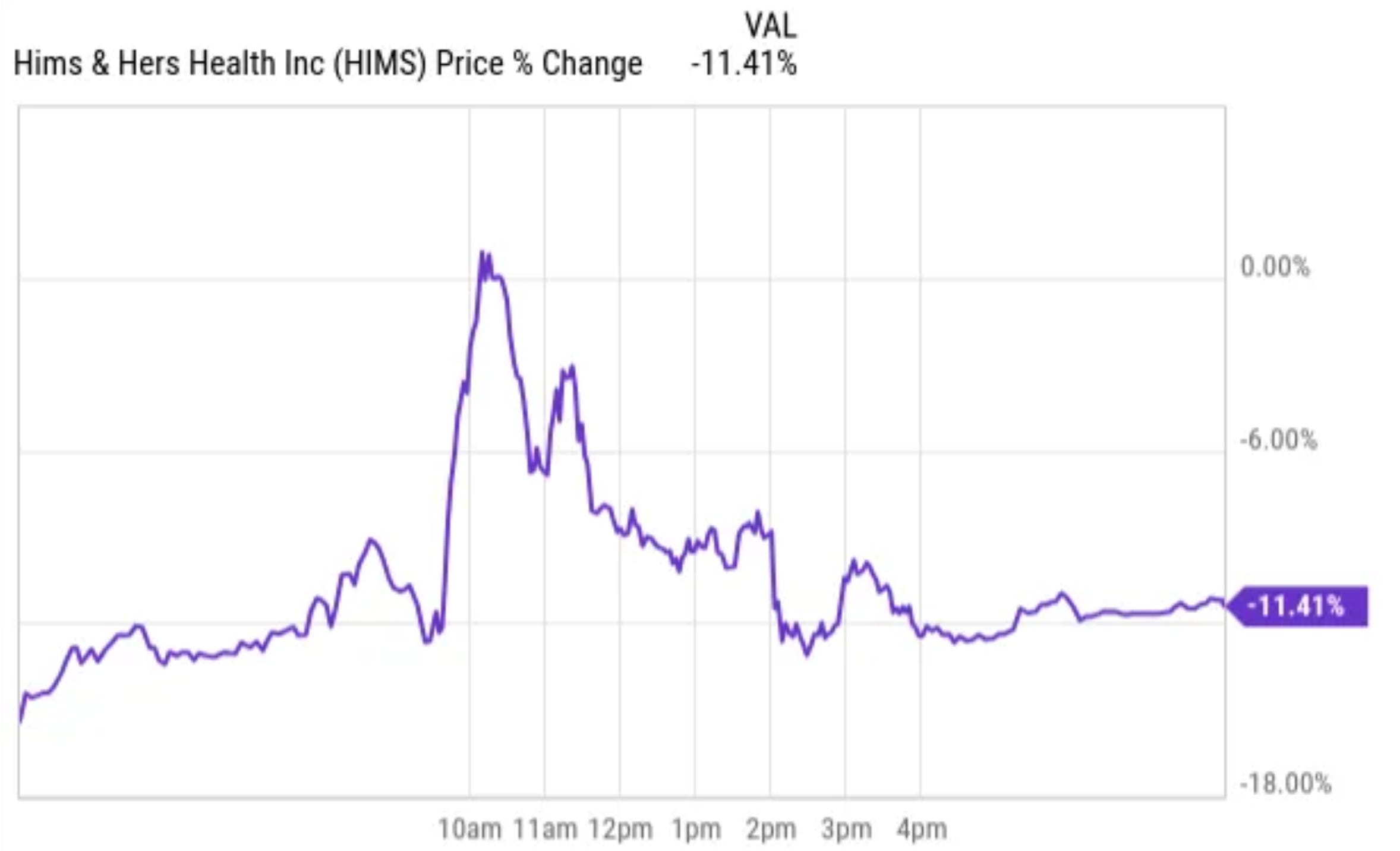

The market didn't know what to think of the results, it seems. First, the stock dropped 16% after-hours, then it opened in the green and then it fell again by double digits.

Everyone sees the headline numbers. Few look deeper, yet most still have an opinion. Let’s actually analyze the report before forming an informed opinion. I see too many following the herd of online commenters who had ready an opinion even before the conference call started. That may be OK to get a first idea, but don’t stick to that initial idea as the absolute truth, as I see so many people do.

So, what is this article about? A summary.

Hims & Hers' stock first crashed, then was in green and crashed again after the earnings.

I was quite negative when I read the headlines and looked at the numbers, but after digging deeper, my perspective shifted.

There's definitely more downside possible and there's legal risk, but the Quality Score actually went UP, to my surprise.

This article will show you what most missed.

The Numbers

Revenue: +73% YoY to $545M, missed the consensus by $7M or 1.3% but on the high end of its own guidance.

Operating Margin: 5%, vs 4% last year in Q2.

EPS: +183% YoY to $0.17, beat by $0.01

GLP-1 Revenue: $190M, down from $230M in Q1.

Core Revenue, ex-GLP-1: $355M, essentially flat vs. $356M in Q1

Subscribers: 2.44M, +31% YoY, +73K QoQ.

Monthly ARPU: $74, down from $84 in Q1 due to GLP-1 churn.

Adjusted EBITDA: $82M vs. $72M expected, 15% margin

Free Cash Flow: -$69M (more about this later, of course)

Guidance: Q3 $570-590M revenue, $60-70M EBITDA; FY25 unchanged at $2.3-2.4B revenue

For the first time since Hims & Hers became a public company, it missed the Wall Street revenue estimates. Not by a lot, but still. Now, you always have to wonder who's wrong there. The company had guided to $530 million to $550 million in revenue and with $545M, it is at the high end of that range. Wall Street just had higher expectations.

Revenue also dropped slightly QoQ, but you should put this in the correct context. In Q1, there was still a GLP-1 shortage, so Hims & Hers could easily sell compounded weight drugs. That fell away in Q2. Of course, the company still sells compounded GLP-1, but only for reasons of personalization. The QoQ decline was completely from GLP-1, which fell from $230 million to $190 million as the company offboarded customers on commercial dosages when the FDA lifted the shortage status of GLP-1.

But that also has a flipside. If you leave out GLP-1 completely, revenue was flat from Q1 to Q2. For a company that previously delivered 5-10% quarterly growth like clockwork, this core business stagnation is a much bigger issue for me than the GLP-1 category. But there, too, it’s not what it seems.

The rest of the article shows you that the GLP-1 cliff is a distraction. The real story is buried inside the call and it made my Quality Score go UP (not down). Members get the full breakdown.