Hi Multis

The poll I launched on Slack showed that you were looking most forward to the Tempus and SEA earnings analysis and you got those two first. The number three was Hims & Hers. So, here’s that one.

I wrote in my previous earnings analysis that this is by far the most volatile stock I’ve ever covered, and nothing has changed. Right now, the stock is down 55% over the last year.

If you want a Fiscal subscription, you get 15% off with this link.

So, is this a moment to buy or should we be cautious? Let’s find out.

The Numbers

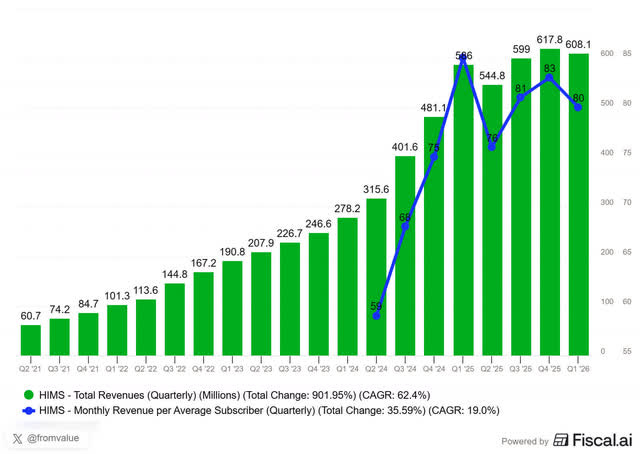

Revenue: $608M, up 4% YoY.

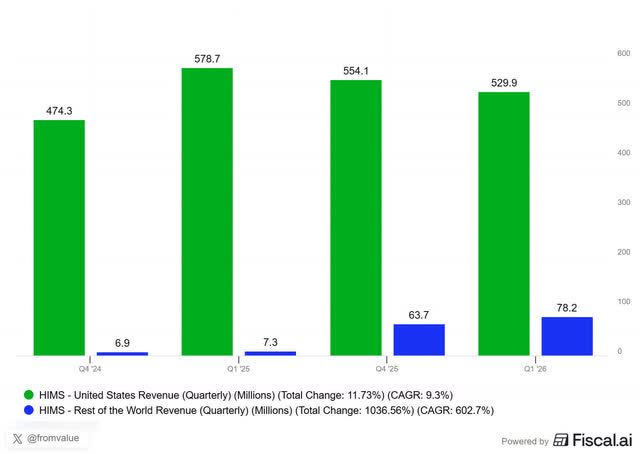

US revenue: $530M, down 8% YoY.

International: $78M, up 969% YoY.

Subscribers: 2.58M, +9% YoY. Personalized: ~1.7M, +20% YoY.

Monthly ARPU: $80, down from $85 a year ago.

Gross margin: 65%, down from 73%.

Adjusted EBITDA: $44M, a 7% margin, down from $91M and 16% in Q1 2025.

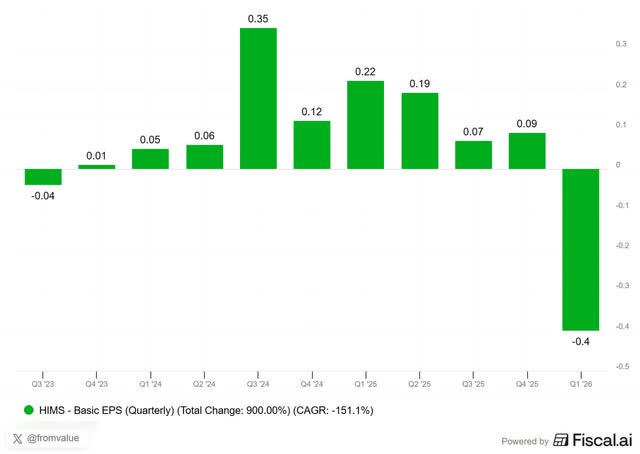

GAAP net income: −$92M, versus +$49M last year.

Free cash flow: $53M.

Guidance Q2: revenue $680–700M (+25 to 28% YoY), adjusted EBITDA $35–55M.

Guidance FY2026: revenue raised to $2.8 to 3.0B, above the consensus of $2.71B.

2030 target: reaffirmed $6.5B+ revenue and $1.3B+ adjusted EBITDA.

Those numbers don’t look great, do they? So, I understand the questions and FUD (fear, uncertainty and doubt) around HIMS.

Until Q1 2025, everything seemed to go well. Revenue was up a lot every quarter and ARPU (average revenue per user) peaked in Q1 2025.

Right now, in Q1 2026, revenue was down QoQ and up only 4% YoY, margins were down, and it posted the first GAAP loss since Q4 2023. Add a miss of $8.75M for revenue and a miss of $0.03 for EPS and it’s not too crazy to think the company is falling apart before your eyes.

I’m going over a few things, though, that could put things in a different light.

The Revenue & EPS Miss

Let’s take the revenue first.

In March, the company stopped advertising compounded GLP-1s and shift to branded weight-loss products, mainly Novo Nordisk’s (NVO) Wegovy pen and Wegovy pill, although Eli Lilly’s Mounjaro is also possible.

I wrote about the mess that came before that decision: the $49 compounded pill that lasted just 48 hours before the FDA, the DOJ and the SEC came knocking and it was withdrawn. The branded pivot is the cleanup of that mess. It took the GLP-1 risk off the table.

But it changes how the money comes in. The compounded business sent out medication in longer cycles, while branded GLP-1s go out monthly. That means there is less upfront recognition. It’s a bit similar to a software company switching from upfront software sales to a SaaS model. So, it’s often the same dollar amount (or even more), but recognized over more periods instead of all at once. In accounting, that looks like a revenue decline.

CFO Yemi Okupe was very clear about this:

These dynamics affect only the timing of revenue recognition and not customer demand or engagement.

That timing change removed about $65 million from Q1 revenue. If you add it back, the quarter would have come in at $673 million, quite a bit higher than the $652 million consensus. So the revenue “miss” wasn’t really a miss. Of course, if revenue is lower, EPS will be lower as well. So, that “miss” had the same cause.

And don’t forget the comparison. Q1 of last year was the best quarter in the company’s history, as I already showed on the chart. GLP-1s had just started on the platform and sold like crazy. So, while the 4% YoY growth looks very weak, it’s not really how you should look at this quarter. On a comparable basis, revenue would have been up about 15%. That may not be a number that excites you, but it’s not as depressing as that 4% revenue growth, right?

US revenue fell about 8% to roughly $530 million, but it would have been up 4% YoY on a comparable basis. Again, not something that will make you jump around in joy, but still a lot better than what you think on first sight.

International revenue jumped almost 10x to $78 million. Of course, this is on a small basis, but still, it’s important. You can see the opposite movements in this chart.

The $92 Million GAAP Loss

Now the GAAP net income loss. I saw this scared quite some investors. After all, the company had been GAAP profitable in every quarter since Q4 2023.

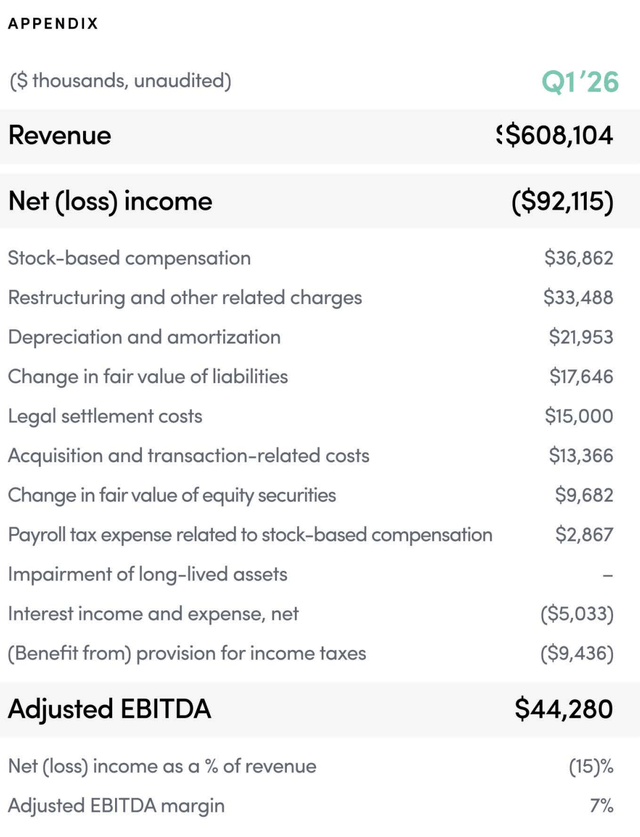

The company gave us the full breakdown, so let’s use it. It’s in the appendix of the earnings call slides. Most will probably never look at that, but we do. I see many takes against adjusted numbers vs. GAAP and to a certain level, I understand that. But adjusted numbers can sometimes give you insights that GAAP earnings can’t. That was definitely the case this time.

After stock-based compensation, which is a quarterly item and hasn’t moved much, the biggest piece is restructuring: about $33 million, of which $28 million is in write-downs related to the compounded GLP-1 supply chain. If you build infrastructure for a business and then you decide to leave it, you write it off. That’s a one-off cost. Take it out, and the gross margin was about 70%, right in line with where Hims & Hers has always been.

And there are other one-offs and non-cash items. There’s a ‘loss’ of $17.6M that’s a provision because Hims & Hers expects that the acquisitions will have higher earn-outs. That’s exactly what you want. Maybe you know this from the contingent payments Topicus and Constellation have. There are certain milestones. You take a base case for your accounting, but if the companies do better than expected, the same percentage of earnings is a higher number. Or because you cross certain expectations, that percentage can even be higher. In other words, that’s something to celebrate, even if this is seen as a “loss” in accounting.

There was also $13.4 million in M&A costs. Hims & Hers has bought quite a few companies: Eucalyptus, YourBio, ZAVA and Livewell. The acquisition process produces costs (think of legal, for example) and the integration process as well.

Then there’s something we saw earlier this quarter from Shopify and Tempus, for example. There’s $9.7 million in losses because some of the investments Hims holds have dropped in value on paper, even though the company hasn’t realized them.

If you look for other numbers, you can look at $89.5 million operating cash flow and $59.5 million in free cash flow this quarter. I think that shows better how Hims & Hers did this quarter. Even if you want to deduct stock-based compensation, you get $22.7M in FCF-SBC. That shows that the GAAP loss is mostly accounting.

Novo Nordisk GLP-1

So why did Hims & Hers do this? The change to branded GLP-1 provides the company (and its investors!) with much greater regulatory certainty. There’s no more Novo Nordisk litigation, and the company goes out of the way of the FDA and the SEC.

And it’s working. Within six weeks of putting Novo’s products on the platform, Hims & Hers fulfilled more than 125,000 Wegovy shipments. Founder and CEO Andrew Dudum on the conference call:

We see it in the scale of new customers coming in the door today, which is larger than as Yemi said, any spikes we saw even during the most important seasonal campaigns such as New Year’s and Super Bowl campaigns.

The New Year and the Super Bowl campaigns are the two most important campaigns for the company. Now, the new ‘normal’ pace after the Novo Nordisk deal is bigger than those peaks. That’s not in the numbers yet, but it’s an important data point. Management says it’s on track to add more than 100,000 weight-loss subscribers per month.

If the company can keep up that pace, subscriber growth would probably land somewhere in the low 30s a year from now.

Subscriber growth looks slow right now, but that is mostly because these new subscribers are just starting to come in. We should see acceleration in the next quarters. The early engagement numbers look good as well. Nearly 90% of these new subscribers download the app, and, on average, they speak with a doctor or nurse from the Hims & Hers care team three times in the first month. That tells me these subscribers are engaged and that makes them more likely to stay.

On the economics, CFO Yemi Okupe said branded and compounded are “roughly comparable” on a dollar basis. The branded GLP-1 has a higher price but a lower margin, and the compounded was the other way around, so they more or less even out. So the company gave up a high-margin product that carried a lot of legal risk and replaced it with a fully legal one at a lower margin that brings in more people. I think that makes sense. It takes away a major risk while still driving growth.

I find it ironic. In the US, Hims & Hers and Novo Nordisk now sell Wegovy through a partnership. That is the company that tore up the first deal and accused them of “illegal sham compounding” last year. Providers on the platform can also send prescriptions to Eli Lilly’s LillyDirect. And then last week, Hims launched generic semaglutide in Canada at C$149 a month, undercutting everyone, on the same molecule Novo uses. It’s important to know that Novo Nordisk’s patent in Canada has expired.

There’s a second irony. While Hims & Hers reduced a major legal risk by partnering with Novo Nordisk, it also introduced a new risk. The partnership already broke before. But right now, Novo Nordisk’s Wegovy is a big revenue growth driver. If the relation gets troubled again, this might have serious consequences for Hims & Hers. But that risk is worth taking more than the legal troubles that the company might have faced otherwise.

Not A GLP-1 Company

I didn’t buy this stock for the GLP-1s. I’ve written that many times before. If this were a GLP-1 company, I would never have been interested. The GLP-1s may be 30% of revenue or less this quarter, given the accounting change we saw earlier. But people keep staring at that one part of the business and completely ignore the rest of the platform, which accounts for 70% or more of the revenue.

That platform is an attempt to bring personalized, proactive, data-driven healthcare. Peter Attia writes about this in his book Outlive, and calls it medicine 3.0. Hims & Hers not only wants personalized healthcare but is also on a mission to make it affordable for everyone. Right now, that kind of care costs the wealthy tens of thousands of dollars a year. Founder and CEO Andrew Dudum put it like this on the call:

Netflix and Spotify reshaped how people could access not only a broader range of content, but also the best the industry has to offer. Health care must evolve towards that same consumer-oriented distribution model.

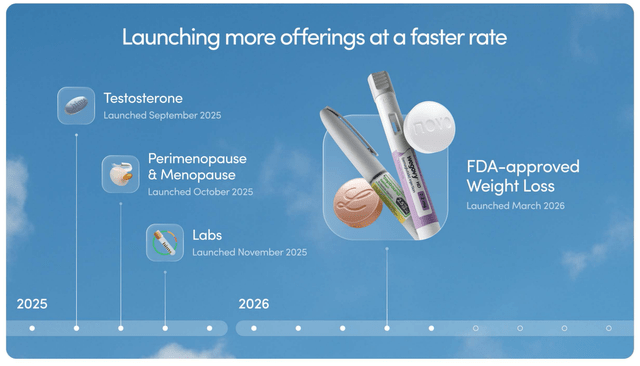

This quarter, some things pointed to this again. Take testosterone, for example. Tens of thousands of men now already take it, and the early results are strong. Andrew Dudum:

More than 95% of individuals utilizing a testosterone support offering experienced an increase in testosterone levels within the first 2 months of treatment, with an average increase of over 80%.

Most men never even know they have low testosterone levels. They just feel tired and blame it on their age, stress or something else. With Hims, they can take an at-home blood test, get treated, and then retest to see if it worked. That is a Medicine 3.0 example, because you find the problem before the patient even knows to look for it.

Then there is Labs. You take a blood test at home, and the app reads out more than 130 biomarkers for you, with AI helping to explain them. Andrew Dudum on the call:

On the Labs side, also, it’s just providing people data that, frankly, used to cost somewhere between $5,000 or $10,000... And then from there, 70% of those people are identifying an area of concern and an area of clinical risk that the platform can actually help treat.

So seven out of ten people who run Labs tests find something they should treat and they can find the treatment on the same platform that just identified the problem. That is great for cross-selling, of course. It’s the kind of preventative care I want to see. And it makes Labs a great entry point to everything Hims & Hers does and sells.

Sexual health and hair loss each took three to four years to cross $100 million in annual revenue. Weight loss did it in seven months.

Andrew Dudum thinks testosterone, menopause and Labs can each get there soon as well.

The GLP-1 noise is the easy part. The hard question is whether there's a real moat underneath, and that's exactly what comes next, along with my verdict on the stock.

If you are a paid subscriber already, you can just scroll past this. If you are not, please read this.

When you join Potential Multibaggers now, you get my entire investment system:

✅ Best Buys Now: every month, the 5 best stocks to buy

✅ My Proprietary Quality Score: rating companies on 17 quality metrics nobody else uses

✅ Deep Earnings Analysis: thorough breakdowns that reveal what really matters

✅ Valuations & Buy/Hold/Sell scales: cut through the noise and know exactly when to act

✅ 15,000+ Word Deep Dives: each pick gets 4-5 extensive articles so you understand exactly what you own.

✅ Private Community: direct access to me and 800+ serious long-term investors.