Hi Multis

Wow, what a trip this has been so far.

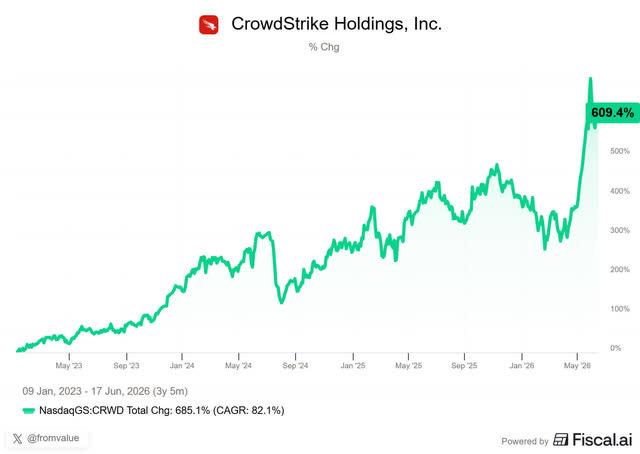

I picked CrowdStrike (CRWD) as a Potential Multibagger on June 29, 2020, almost six years ago exactly, at $98.10. That means it is almost a 7-bagger. But in typical Potential Multibaggers style, it has been very volatile and, I’m sure, will remain so.

This is how multibaggers go. Everyone wants to celebrate a multibagger, but very few have the stomach to hold on to stocks through the ups and downs.

Don’t be mistaken in thinking that CrowdStrike was an easy hold. It first became a threebagger in a relatively short time and then went back to square 1 in January 2023.

That means the stock was down 65% from the top. Of course, as always, the cynics were ready to chime in: to get back to even, the stock has to almost triple.

There are two problems with that.

The first false assumption is that everyone picked the absolute top. If you picked the absolute bottom, everyone would accuse you of cherry-picking, and they would be right. But if someone cherry-picks negatively, it just passes as if that’s normal. My irritation about this is one of my pet peeves.

Secondly, the percentages make it seem impossible. To be exact, the stock would have to win 186% to get back to the top. Including the stock price, that’s almost a triple. Sounds hard, right? But the stock just has to regain the lost dollar amount. Math is somewhat misleading here. Not factual, of course, but psychological. It makes it sound almost impossible or very hard. But if you look at the bottom, this often happens and usually very quickly.

Just look at what CrowdStrike did from January 2023.

As you can see, the stock is more than a 7-bagger from that point. I looked at when it exceeded its previous top. The poetic beauty of the facts is that it was exactly a year after that bottom.

As long as a company keeps performing fundamentally, the stock return will come. Sometimes it goes swiftly, sometimes you have to exercise years of patience. That’s the entrance ticket for outsized returns.

This is what Charlie Munger said about this.

But enough musings. It’s time for action. And Zack will help me. He will analyze the earnings, although I also contributed a few elements. Even when someone else writes, I still analyze, so I don’t lose touch with the stock.

After the analysis, I take over again for the Selling Rules, the PM Quality Score update and the Valuation to see if CrowdStrike is still attractive at this price, or if it would be wise to sell or trim. Take it away, Zack.

Hi Multis

Leading up to earnings, CrowdStrike went on a generational run, more than doubling from the AI-fear lows set earlier in the year.

The sentiment on X went from “CrowdStrike is going to be replaced by Claude!” to “CrowdStrike is overvalued!” in a matter of months.

CrowdStrike stock run(Fiscal.ai)

So what happened in the past 4 months? Did something fundamental change? Read on to find out.

Headline Numbers

Let’s first dive into the numbers.

Revenue grew to $1.39B, 26% increase year-over-year, exceeding estimates by 1.7%.

Annual Recurring Revenue (’ARR’) grew to $5.51B, growing 24% year-over-year.

As a reminder, for SaaS companies, ARR is often a better indicator than revenue because it more accurately reflects current and future obligations due to the nature of GAAP revenue recognition.

Net New ARR which came in at $256M, up 32% year-over-year indicating continual expansion of contracted revenue with existing and new business. A related note: both SGNL and Seraphic closed in Q1, contributing $7.8M of acquired net new ARR to this quarter.

Charting ARR over the past few quarters, we see the reacceleration of revenue continue after an initial slowdown in the quarters prior:

The growing ARR is also reflected in the increased module adoption that continues to march up and to the right:

ARR and adoption charts(Fiscal.ai)

There’s one more forward-looking number worth paying attention to: RPO or Remaining Performance Obligations. That’s revenue that is already under contract but that can’t be booked as revenue yet because CrowdStrike still has to deliver the services. RPO came in at $8.8B, up 29% year-over-year. That’s growing even faster than ARR and revenue. Probably, that’s a result of the bigger and longer contracts that CrowdStrike can sign.

Subscription Gross Margin came in at 78%, or 81% on a non-GAAP basis. Both were up by 1% compared to their respective quarterly numbers from last year.

Operating Income (Loss) was ($30.6M) compared to ($118.7M) in FY 2026. Non-GAAP income was $325M compared to $201M in FY2026. The biggest contributors to the swing in income were a reduction in expenses related to the July 19th incident (damages from the big outage), which dropped over 50% compared with last year, and reduced SBC (stock-based compensation) as a percentage of revenue.

While operating income is still in the negative on a GAAP basis (mostly due to SBC), we see that Operating Cash Flow continues to grow every quarter, reaching a record high of $591M, growing 54% year-over-year.

Net Income (Loss) was $27.8M compared to ($104.3M) in Q1 FY2026. Non-GAAP net income was $283.4M compared to $184.7M in Q1 FY2026. GAAP net income got an $18M boost from gains on strategic investments. CrowdStrike has a venture fund, the Falcon Fund, and probably one or a few of those investments did very well.

Earnings Per Share (diluted) on a GAAP basis was $0.11 compared to a loss of $0.42 in Q1 FY2026. Non-GAAP Earnings Per Share (diluted) was $1.10 compared to $0.73 in Q1 FY2026.

Free Cash Flow was $468.5M compared to $279.4M in FY2026 while maintaining a stellar 34% free cash flow margin.

Cash and cash equivalents stood at $4.55B. This rock-solid balance sheet continues to provide security and massive optionality via future acquisitions or buybacks.

In Q1, CrowdStrike repurchased $176 million in shares at an average price of $365.63, leaving approximately $1.3 billion remaining under their current authorization. Management noted they will remain opportunistic in returning capital while staying focused on capturing the significant growth opportunities ahead.

CrowdStrike also announced a 4-for-1 stock split, the company’s first as a public company. While stock splits are purely cosmetic, they can increase liquidity for both shares and options. Shares will begin trading on a split-adjusted basis on July 2, 2026.

Guidance

For Q2 FY2027, management guided:

ARR: $5.793B – $5.795B (24% YoY growth),

Net new ARR: $284M – $286M (28 – 29% YoY growth)

Revenue: $1.436B – $1.442B (23% YoY growth)

For the full year FY2027:

ARR: $6.531B – $6.556B (25% YoY growth); a slight raise.

Net New ARR growth: raised to 27.7% at the midpoint which is a 520 basis point increase from prior guidance, implying $1.279B – $1.303B of net new ARR. This is a meaningful revision and signals that management sees future business expansion in the pipeline.

Revenue: $5.915B – $5.959B (23 – 24% YoY growth); a slight raise.

Free cash flow margin: At least 30% for the full year

Overall, these were incredibly solid numbers across the board, showing clear signs of top-line reacceleration and improving operational leverage as they shake off the final impacts of the July 2024 incident.

Now let’s move on to what CEO George Kurtz referred to as the “Mythos inflection moment”.

The Mythos Moment

First, a quick recap of what transpired over the past few months:

A shift began at the RSA Conference in late March 2026, slightly before Mythos was even announced. Founder and CEO George Kurtz mentions that every meeting he had that week boiled down to the same thing:

Every meeting was literally the same meeting all over. Help us protect these AI workloads that are running on the endpoints. All the developers are running it, marketing is running it, accounting is running it. We heard just crazy stories about AI run amok.

Organizations want to move faster in adopting AI without compromising security.

Then, in April 2026, more fuel was added to the fire with Anthropic releasing a new frontier model referred to as “Mythos,” which demonstrated an ability to identify software vulnerabilities and construct sophisticated cyberattacks at an unprecedented speed and scale.

Claude Mythos(Anthropic)

Source: Anthropic

Now, any reasonably technical person or AI agent can potentially conduct serious cyberattacks against enterprise infrastructure, and cybersecurity’s role in the enterprise has evolved overnight. Founder and CEO George Kurtz:

For the first time in my career, the market’s view of cybersecurity’s role has shifted from being viewed primarily through the lens of risk management, compliance, and protection to being recognized as a strategic accelerator and a critical enabler of AI adoption.

The funny thing is that if you have been following CrowdStrike for a few years, George Kurtz has said this forever. So, it was with pride that he said this. Cybersecurity is now a necessity for enterprises that want to leverage and accelerate AI quickly, as deploying AI across an organization without proper security controls is too risky. Secondly, on the defensive end, frontier AI models (e.g. Mythos) have increased the attack surface and lowered the barrier for adversaries, increasing the security gap enterprises were already facing.

In response to this potential threat, new programs were created: Anthropic’s Project Glasswing and OpenAI’s Trusted Access for Cyber (’TAC’).

CrowdStrike was the only cybersecurity company selected for both, underscoring its leadership in this space. These programs gave enterprise companies early access to frontier models to ensure that necessary cybersecurity guardrails were in place before the models were released to the public.

This quarter, CrowdStrike also took the initiative in launching Project QuiltWorks.

Source: CrowdStrike

This is an industry-wide coalition of the world’s top AI companies, consulting firms, and cyber insurance companies, all under one roof, with the goal of providing auditing services with the CrowdStrike platform to identify vulnerabilities within companies.

As you can imagine, all of this serves as a new marketing and sales pipeline for the business, positioning CrowdStrike as the thought leader and best-of-breed in this space.

It’s ironic how what initially started as a threat to the CrowdStrike business is now a sales generator. I mentioned that in last quarter’s analysis of the “AI Threat” and it looks like it’s playing out exactly as I saw it then:

To flip the script, rather than a threat, AI and the “agentic workforce” represent a massive new market for CrowdStrike. AI adoption means a new attack surface that must be secured. As it grows, CrowdStrike becomes an even more necessary layer of protection for the AI stack. We are already seeing this reflected in the growth of the modules (Identity, Endpoint, AI-DR, etc.) mentioned earlier in this article. CrowdStrike is set to benefit from this AI revolution, not be replaced by it.

This entire pivot was further proof to me of just how much the market is driven entirely by narratives. Especially in an environment with volatile price action, you can clearly see how negative narratives drive down prices, which then fuels an even more negative narrative. The cycle repeats endlessly until the story finally turns. Keep in mind, this whole roller coaster happened despite zero evidence of fundamental weakness.

So the narrative flipped, the fundamentals are stronger than ever, and the stock just doubled in four months. I bought back then, based on the valuation, which is in the paid part below.

Below: the customer behavior that proves how sticky this platform is, the AI giants that are now building on top of CrowdStrike, the exact price I’d buy more of this stock at, and what I’m doing with my position after a 7-bagger.

Don’t want to miss opportunities like this one again?